The Vietnamese economy is facing a pivotal moment, opening a new chapter in the socio-economic development history of the nation. The period 2021-2025 has played a role as a period of overcoming difficulties and consolidating internal strength after unprecedented shocks from the global pandemic and complex geopolitical fluctuations.

In that context, the 14th National Party Congress was identified as an important milestone, shaping a new development space with the aspiration to break through to realize the vision of 2045: To become a developed, high-income country. General Secretary To Lam's message on the goal of double-digit growth is not simply a quantitative indicator but also a supreme political order to bring the country through the middle-income trap and strongly move into a new era.

To achieve this breakthrough growth goal, the macroeconomic management system, especially the coordination between fiscal policy and monetary policy, needs a fundamental shift in thinking. If in the period 2021-2024, these two policies mainly played a role in stabilizing the economy and supporting businesses to recover from the epidemic, then in the era of rise, they must become strong policy levers to unlock and ensure resources for development. Fiscal policy is expected to play a leading role through public investment and strategic infrastructure, while monetary policy plays a stepping stone, ensuring liquidity and regulating capital flows into new economic sectors with higher productivity and quality.

The global context for the period 2025-2030 is forecast to continue to operate in a state of high uncertainty. The rise of protectionist trade policies, tariff-to-technology conflicts and the fragmentation of supply chains are creating significant risks for an open economy like Vietnam. However, opportunities always exist in challenges. The shift of high-quality FDI flows towards core technology industries such as semiconductor, artificial intelligence and green economy is opening the door for Vietnam to reposition its position better in the global value chain. The transformation of the growth model from "wide" to "deep", taking science - technology and innovation as the central driving force, is the key to realizing the strategic goals of the 14th Party Congress.

Looking back at the period 2021-2024, Vietnam's economy has shown incredible resilience. After only achieving a growth rate of 2.56% in 2021 due to the heavy impact of the pandemic, GDP recovered dramatically to 8.02% in 2022. However, this recovery momentum did not maintain stability when growth slowed down to 5.05% in 2023, reflecting difficulties from weakening world demand and internal barriers to the economy. Stepping into 2024, positive recovery signals have returned with an estimated growth rate of 7.09%, bringing the scale of the economy to 476.3 billion USD.

Although there is a recovery in terms of quantity, the quality of growth still has many problems to be solved. The ICOR (capital efficiency) in the state sector is still maintained at a worryingly high level, reaching about 17.8, showing that the cost to create a growth unit is too expensive. This proves that the growth model based excessively on investment capital and cheap labor has reached the limit. In addition, domestic consumption, although growing, has not had a real breakthrough, with the consumption growth index in the first quarter of 2025 reaching 7.45%, still lower than the target set for the whole year.

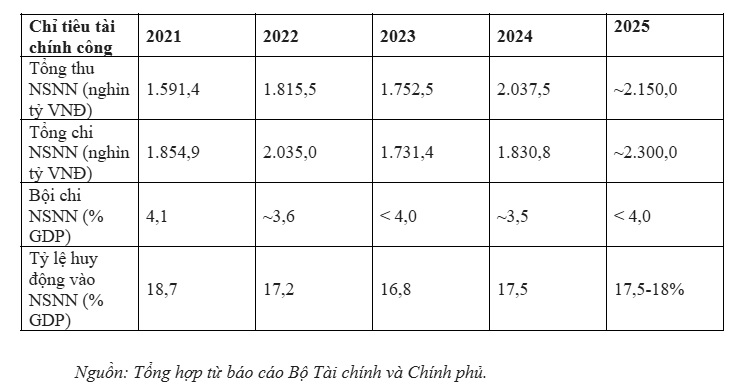

In the period 2021-2025, fiscal policy has excellently performed the role of "supporting" the economy. Total state budget revenue (NSNN) for the whole period is estimated at about 9.5 million billion VND, far exceeding the target of 8.3 million billion VND and 1.36 times higher than the period 2016-2020. This result was achieved thanks to proactiveness in tax management reform, expansion of revenue base and promotion of digitalization in budget revenue work. In terms of spending, fiscal policy has been managed in the direction of saving recurrent expenditures to allocate resources for development investment and social security. Budget deficit is strictly controlled at 3.1-3.2% of GDP, lower than the threshold approved by the National Assembly. However, a major bottleneck in spending management is the slow disbursement of public investment capital.

Vietnam's public debt in the period 2021-2025 has had strategic changes, creating an important comparative advantage compared to many countries in the region. From 42.7% of GDP in 2021, public debt has continuously decreased to about 34% in 2024 and fluctuated around 36-37% by the end of 2025. This figure is much lower than the 60% ceiling and the 55% warning threshold stipulated in Resolution 23/2021/QH15.

A highlight in public debt management is the improvement in the balance structure towards sustainability. The proportion of domestic debt compared to the total government balance has increased from 60.1% in 2016 to 71.9% in 2023. Domestic borrowing mainly through the issuance of long-term government bonds (average nearly 10 years) and low interest rates (average 3.01%/year) has helped minimize exchange rate risks and reduce debt repayment pressure in the short term. This is the abundant "fiscal space", allowing the Government to boldly mobilize capital to invest in super infrastructure projects such as the North-South High-Speed Railway without causing risks to national financial security.

While fiscal policy has great room, monetary policy is facing challenges in terms of easing limits and systemic risks. Credit is still the main capital supply channel for the economy. The large dependence on banking leverage has made the financial system sensitive to interest rate shocks and asset market fluctuations.

The bad debt ratio tends to increase. The expiration of Circular 02 on debt extension and postponement has forced banks to recognize substantive risks, increasing the pressure to make provisions and eroding profits. In particular, capital flows are excessively concentrated in real estate (accounting for about 21% of total outstanding debt) while house and land prices have increased to an unreasonable level (60 times higher than workers' income) creating risks of asset bubbles and potential cross-debt.

In the new era, fiscal policy must carry out a revolution in management thinking, shifting from passive support to maintain stability to a leading role, unlocking resources for rapid growth. This requires courage in exploiting existing room and innovating the method of allocating budget capital. Maintaining public debt at a low level while the need for strategic infrastructure investment is still very large is assessed by experts as a waste of opportunity costs.

To achieve the double-digit growth target, the Government needs to boldly relax the actual public debt ceiling to mobilize capital for basic infrastructure projects including transportation, energy and digitization. These mega-public investment projects are not just simple public investments but also driving forces to create a new economic space, improving long-term national competitiveness.

The debt management strategy to 2030 has affirmed that mobilizing domestic capital through the Government bond market is the main thing and with the fact that domestic debt accounts for more than 70% of the Government's outstanding debt, it will be a solid foundation for the Government to implement large investment stimulus packages while maintaining financial security. However, all fiscal capital sources will become meaningless if they cannot be disbursed into reality.

The bottleneck in disbursing public investment needs to be removed by more synchronous and drastic measures, in which it is necessary to focus on reforming and removing institutional bottlenecks, policy change risks and responsibilities in the implementation stage. Eliminating the "ask - give" mindset, applying a set of monthly cadre evaluation criteria associated with project progress and strongly shifting to a "post-inspection" mechanism based on digital platforms are urgent requirements.

Public investment must truly play the role of "bait capital", activating capital flows from the private and foreign sectors. Public-private partnership (PPP) models need to be redesigned to be more transparent, protecting the legitimate rights of investors, especially in the fields of green infrastructure and high technology. Reducing 30% of legal compliance costs for businesses through institutional reform will help the private sector have the ability to absorb capital more effectively, creating a real spillover effect from government spending.

To ensure sustainable resources for rapid growth, fiscal policy needs to aim to expand the tax base and restructure revenue sources. However, in the short term, tax exemption and reduction policies still need to be maintained in a focused manner to support businesses to overcome the model transformation phase. In particular, fiscal policy needs to be used as a sharp tool to promote R&D and technology application.

Breakthrough fiscal solutions in Resolution 68 such as allowing businesses to deduct up to 20% of pre-tax profit to establish a Technology Innovation Fund and applying a "double tax deduction" mechanism for R&D costs are important solutions to encourage private sector investment in core technology. This is the shortest path to shift from a processing economy to a creative economy, creating higher added value for the country.

The reality of monetary policy management in recent years shows that pressure from changes in trade policy and monetary management of major countries is creating "reverse winds" for the exchange rate and foreign exchange reserves of Vietnam. In that context, exchange rate management needs flexibility to absorb external shocks, contributing to controlling inflation, while stabilizing market sentiment and strengthening investors and people's confidence in the Vietnamese currency.

In that context, to make the banking system a solid backing for rapid growth, Firstly, the SBV and commercial banks need to drastically implement system restructuring associated with bad debt handling. The key task is to focus on definitively handling weak banks, and promote the increase of charter capital for state-owned commercial banks to raise the capital adequacy ratio (CAR) to over 12% by 2026.

The termination of temporary easing policies (such as Circular 02) will help bad debts become clearer to have substantive handling measures through the debt trading market. At the same time, it is necessary to strengthen supervision to detect and handle cross-ownership relationships between banks and business groups, preventing risks of cross-spreading in the financial system.

Secondly, the policy of expanding credit during the high growth period poses many risks if capital flows into asset speculation sectors. The SBV needs to strictly control capital flows into real estate or other speculative bubbles. Credit policies need to be prioritized and oriented towards key industries such as semiconductor, AI, green economy and circular economy in accordance with the guidelines and policies on economic restructuring of the Party and the State. For example, the implementation of Resolution 57 with special credit packages with preferential interest rates lower than the market by 2-3% for businesses in the key industrial ecosystem such as the semiconductor and AI industries is a focus that needs to be accelerated.

To achieve breakthrough growth while maintaining macroeconomic stability, the coordination between fiscal and monetary policies needs to be elevated to a state of "dynamic balance".

First, it is necessary to strengthen coordination that needs to be designed according to the principle: Fiscal policy needs to be done by stimulating both total supply and demand, while monetary policy focuses on ensuring liquidity and price stability. If the fiscal year expands excessively without monetary regulation, it will lead to inflation risks, conversely, if the monetary policy is too tight while the fiscal year needs infrastructure investment resources, it will lead to high interest rates, overwhelming private investment. Credit growth needs to be maintained at 15-16% by 2026 to meet capital needs, but must be accompanied by strict control of the speed of monetary circulation to avoid putting pressure on inflation.

Second, it is necessary to strongly develop the bond and stock markets to create long-term capital channels. Fiscal policy can support through tax exemptions for listed companies applying international financial reporting standards (IFRS), while monetary policy supports through stabilizing interest rates and creating liquidity for the debt market. Building a strong domestic debt market not only helps the Government mobilize capital for strategic projects but also creates a diverse capital ecosystem for the private sector.

Third, institutional breakthroughs in the new era must be built on the foundation of protecting innovative businesses and applying the principle: businesses are allowed to do everything that is not prohibited by law. The abolition of the "ask-give" mechanism, strongly shifting from "pre-inspection" to "post-inspection" based on digital governance will help reduce at least 30% of legal compliance costs, freezing capital flows that are frozen in thousands of projects that are backlogged in many sectors of the economy.

Fourth, fiscal and monetary policies need to coordinate to create an "innovation ecosystem" in accordance with the spirit of Resolution 57 and recent Central Resolutions. Accordingly, source capital from the state budget should focus on basic research and national data infrastructure, while bank credit and venture capital funds provide capital for technology commercialization projects. The goal is to increase the contribution of total factor productivity (TFP) to economic growth by at least 60% by 2030.

To achieve this figure, the rate of increase in social labor productivity needs to reach about 8.5%/year, 1.5 times higher than the previous period. This is a huge challenge, requiring synchronous investment in high-quality education, human resource retraining and strong application of AI and automation in production. Therefore, innovating the public finance model and mobilizing private resources for education will also be a key task in the coming time.

The period 2021-2025 has proven the bravery and resilience of the Vietnamese economy through the harsh challenges of both external and internal factors. However, to realize the aspirations of the XIV Congress and strongly move into the stage of accelerating sustainable development, we cannot be satisfied with old ways of doing things and policies.

The shift in fiscal and monetary policy from supporting macroeconomic recovery and stability to ensuring resources for rapid and sustainable growth is an urgent requirement. Under all conditions, institutional reform must be implemented with a determination to implement it to unlock all social resources, all potentials of economic sectors in the era of national rise.