Supply and demand both increase

According to data recently released by the OneHousing Center for Market Research and Customer Insights, the entire Hanoi market had about 83,000 residential real estate transactions in the first 9 months of 2024. Primary transactions, including high-rise and low-rise, accounted for 27%, while the remaining 73% were secondary transactions, including residential land, apartment transfers and low-rise houses.

At the end of the third quarter of 2024, the newly opened apartment market in Hanoi recorded an average price of nearly VND 80.5 million/m2 (including VAT and maintenance fees), an increase of 7.6% over the previous quarter.

The average price of transferred apartments in Hanoi reached nearly 55 million VND/m2 (including all service fees and rental fees according to the Law), an increase of 4% compared to the previous quarter, especially at the two projects Vinhomes Ocean Park and Vinhomes Smart City, an increase of up to 10%.

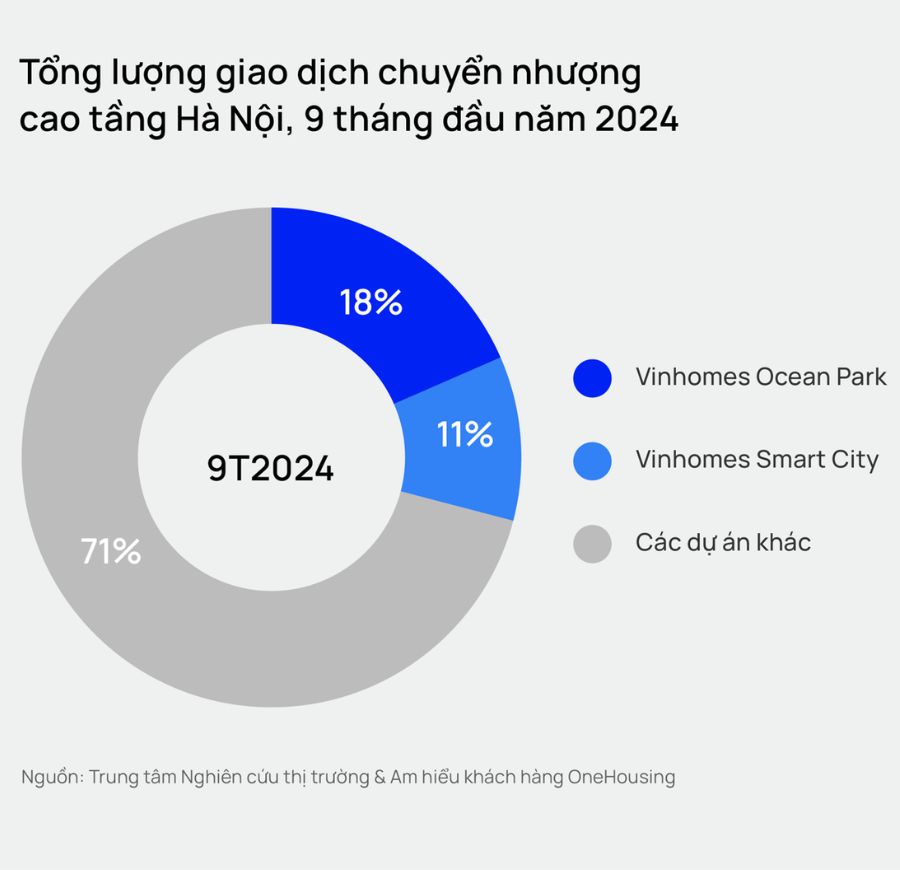

Despite high prices, apartment transactions still increased sharply in both the primary and secondary markets. Primary apartment transactions in the first 9 months of 2024 reached 21,100 units, an increase of 205% over the same period in 2023. Meanwhile, high-rise transfer transactions were about 25,200 units and 30% of transactions were mainly concentrated in two major urban areas: Vinhomes Ocean Park and Vinhomes Smart City.

Mr. Tran Minh Tien - Director of OneHousing Market Research and Customer Insight Center - acknowledged that with high demand and rapid price increase, apartment real estate is being chosen by many investors as a safe haven for accumulated cash flow.

Investors continuously release products

In Hanoi, the supply for the whole year of 2024 is expected to reach nearly 30,000 units, almost equivalent to 2019 - the pre-COVID-19 period and higher than the period 2020 - 2023; especially higher than the previous forecast (22,000 - 24,000 units). According to the OneHousing Center for Market Research and Customer Insights, high-end and luxury apartments will continue to account for the majority of supply in late 2024 and 2025.

Explaining the increase in supply compared to the forecast, Mr. Tran Minh Tien said: “In the second half of 2024, the apartment market is better than previously forecast, the absorption rate of primary supply is up to 80 - 90%. Many new projects are launched and sold out in a short time, in particular, there are projects that match all newly launched apartments in 48 hours or sell out the list of products in just 2-3 weeks.

Seeing the good signals of the market, investors with financial potential and having projects with full legal documents have launched their products earlier than expected in 2025 - 2026, providing the market with a relatively abundant supply of apartments.

In 2025, the total new supply in the market is expected to be equivalent to or higher than in 2024, mainly in the high-end and luxury segments. Meanwhile, secondary high-rise transactions are still popular - forecasted at about 36,100 units in 2025 (up 3% compared to 2024).

"Secondary sales are still mainly concentrated in Vinhomes Ocean Park and Vinhomes Smart City, and sales in these two urban areas are even higher than the average of the whole market because many subdivisions are expected to be handed over next year," said Mr. Tien.