The Government has just issued Decree 253/2026/ND-CP detailing a number of articles and measures to organize and guide the implementation of the 2025 Personal Income Tax Law, replacing Decree 65/2013/ND-CP.

One of the notable new points of the decree is that taxpayers who are resident individuals are entitled to deductions from taxable income before tax calculation for expenses for health, education - training of themselves and dependents when determining income from salaries and wages.

Taxpayers are entitled to deductions for medical examination and treatment expenses at domestic medical facilities within the scope of the list paid by health insurance, with a total deduction of a maximum of 23 million VND/year.

For education and training, the maximum deduction is 24 million VND/year for tuition fees at domestic education and training institutions, including tuition fees for preschool education, general education, vocational education, higher education according to the provisions of education law and other professional skills training courses.

To be deducted, these expenses must have invoices and documents according to the provisions of law. Medical expenses must be accompanied by a list of medical examination and treatment costs used at medical examination and treatment facilities according to the regulations of the Minister of Health.

According to the 2025 Personal Income Tax Law, from 2026, the family deduction for taxpayers will be increased to 15.5 million VND/month, equivalent to 186 million VND/year. The deduction for each dependent person will be increased to 6.2 million VND/month.

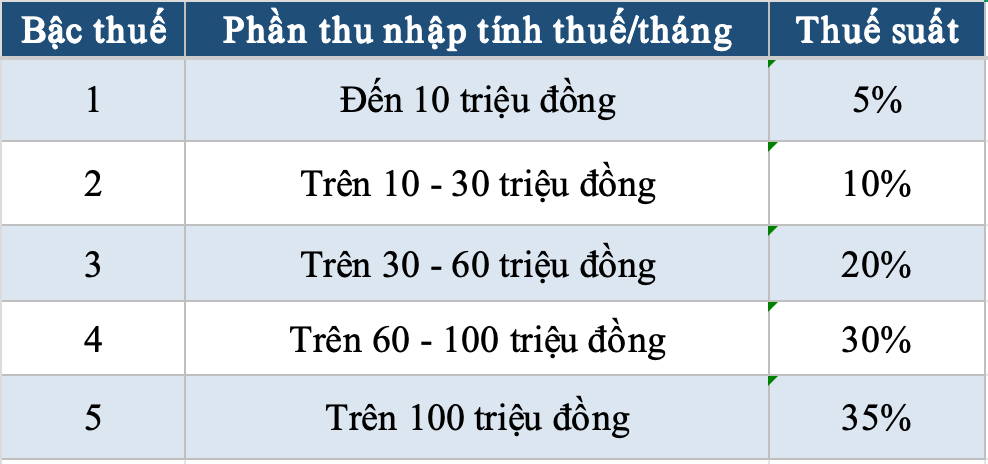

The law also amends the tax schedule applied to income from salaries and wages in the direction of reducing from 7 levels to 5 levels and widening the income gap between tax levels.

Thus, not including the deductions for social insurance, health insurance and unemployment insurance, in case the taxpayer has 1 dependent and fully incurs the health, education - training expenses that are maximally reduced, the total amount of deductions in the year may be up to 307.4 million VND.

This deduction level is determined based on deductions for taxpayers themselves of 186 million VND/year, deductions for 1 dependent of 74.4 million VND/year, deductions for medical expenses up to 23 million VND/year and deductions for education and training expenses up to 24 million VND/year.

According to calculations by the Ministry of Finance, in case a taxpayer has 1 dependent and has an income of 28 million VND/month, after deducting insurance premiums, personal deductions, deductions for dependents and health, education - training deductions at the maximum level, personal income tax is still not yet payable.

In the specific case as above, taxpayers with income over 28.63 million VND/month are required to pay tax with a starting tax rate of 5%," Mr. Luu Duc Huy, Deputy Director of the Department of Tax, Fee and Charge Policy Management and Supervision (Ministry of Finance) informed.

The 2025 Personal Income Tax Law and Decree 253/2026/ND-CP take effect from July 1. However, regulations related to business income, salaries, and wages of resident individuals are applied from the tax period of 2026.

For cases that have declared and paid tax on income from salaries and wages of the 2026 tax period from January 1 to before July 1 according to old regulations, Decree 253/2026/ND-CP stipulates that tax declaration dossiers are not required to be re-submitted monthly or quarterly but are adjusted when preparing tax finalization dossiers for 2026.