In many previous cycles, gold prices were mainly viewed through the lens of interest rates, the USD and inflation. When bond yields increase, the opportunity cost of holding non-genuine assets such as gold also increases.

As the USD strengthens, gold becomes more expensive for buyers outside the US. These factors are still present and continue to put pressure on the market in the short term.

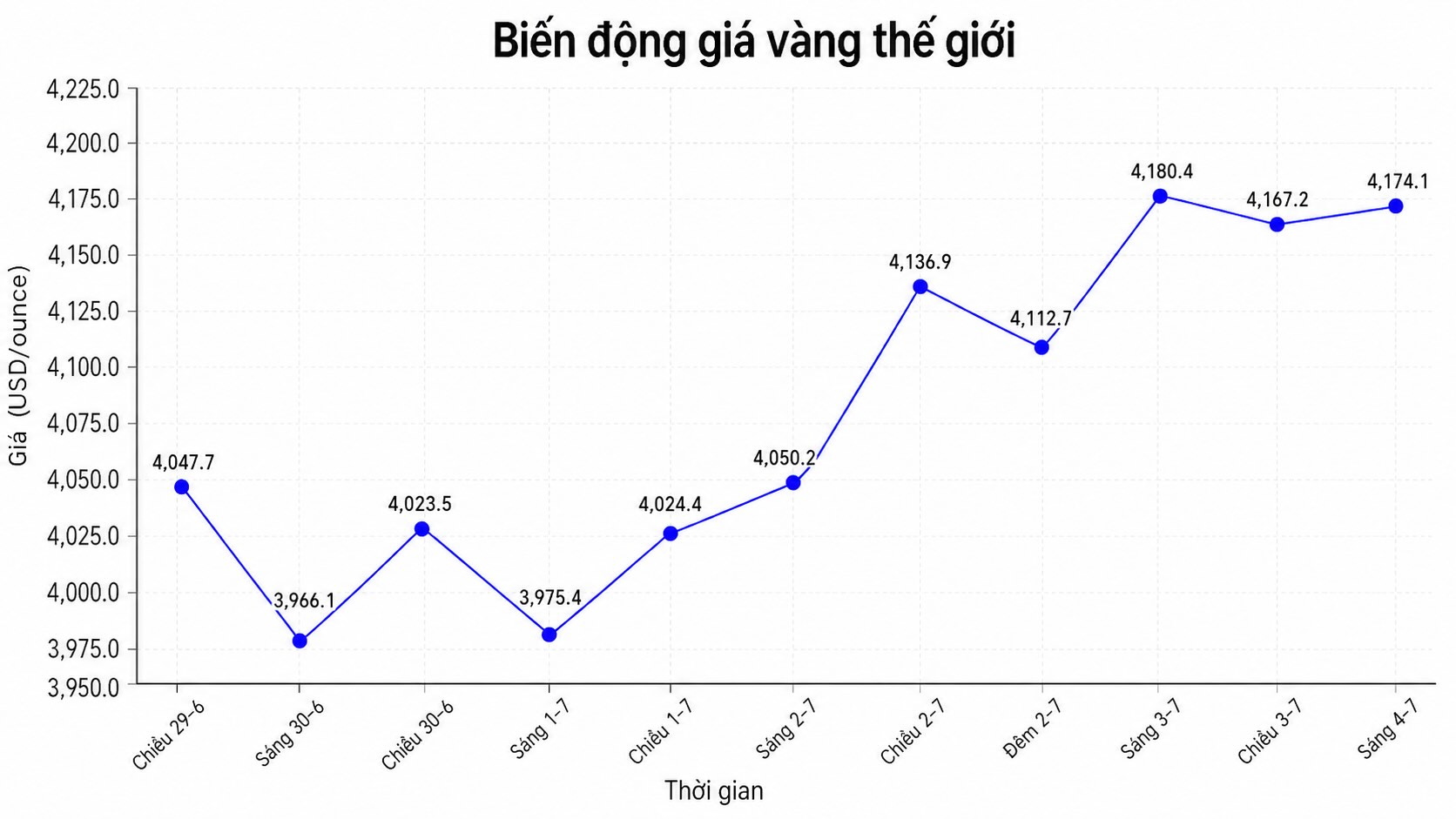

In fact, the recent adjustment of gold prices took place in the context of real yields in the US remaining at a high level, the USD being supported and expectations for the Fed's monetary policy fluctuating strongly.

HSBC (one of the largest financial - banking corporations in the world) believes that US Treasury bond yields are currently one of the main factors dominating gold price movements. When the market assesses the possibility of the US Federal Reserve (Fed) maintaining a tougher stance, the precious metal is unlikely to increase sharply like in the previous period.

However, if only looking at short-term resistance, investors may overlook more important changes taking place in the gold market structure. Unlike speculative cash flows or ETF investors who can buy and sell quickly according to price fluctuations, central banks buy gold with a much longer-term vision. These are decisions associated with reserve safety, asset diversification and reducing dependence on a single currency.

Data from the World Gold Council shows that central banks net bought 41 tons of gold in May, the second highest level since the beginning of the year. Poland, China, Uzbekistan, Kazakhstan and Singapore are in the noteworthy buying group. Poland alone has accumulated 64 tons of gold since the beginning of the year, while China continues to extend its net buying streak for many consecutive months.

The noteworthy point is that this buying activity did not take place in a pleasant cheap environment. This shows that gold is not only bought for short-term price increase expectations, but also for its strategic role in the national reserve system.

Recent surveys also reinforce this view. The World Gold Council said a record 45% rate of central banks expecting to increase gold holdings in the next 12 months, while nearly 90% believe that global official gold reserves will continue to rise.

A survey by OMFIF (an independent research organization specializing in central banking and national reserve management) also shows that many reserve managers expect gold prices to trade in the 5,000-6,000 USD/ounce range in the coming year.

This change reflects a broader reality: gold is playing its role as a neutral reserve asset.

Meanwhile, State Street (a large US financial group) believes that although the gold's upward journey may be more bumpy than the 2024-2025 period, the upward cycle has not ended. This organization forecasts that gold prices may rise to the 4,750-5,500 USD/ounce range in the next 6-9 months, thanks to demand from Asia, central bank buying power and portfolio diversification.

When stocks and bonds tend to fluctuate more in the same direction than before, investors need assets that can reduce portfolio risk. According to HSBC experts, gold still plays an important role in diversification in the face of major market shocks.

This also explains why gold may not increase sharply even when geopolitical tensions escalate. When oil increases, fears of inflation return, yields and the USD rise together, gold may be sold to meet cash demand. But that does not mean gold loses its shelter role.

Overall, the gold market seems to be entering a different cycle than before. Interest rates, USD and inflation still determine short-term fluctuations, but strategic buying power from the central bank is creating a long-term foundation. When the main buying group is organizations making decisions in decades instead of quarters, the trend of gold prices also needs to be assessed by a longer timeframe.

Therefore, the recent adjustment may make the market more cautious, but not enough to conclude that the upward cycle of gold prices has ended. On the contrary, if official buying power continues to be maintained at a high level, the demand for diversification of reserves expands and investment capital returns, gold still has a basis to maintain its central role in a new upward cycle.