Gold prices have just undergone a significant correction after a historic hot period, causing the market to question whether the long-term price increase cycle of this precious metal is weakening?

Short-term pressure comes from expectations that the US Federal Reserve (Fed) will maintain high interest rates, bond yields will rise and the USD will strengthen. However, many major financial institutions believe that behind short-term fluctuations, a more important driving force has not changed: the gold buying demand of central banks.

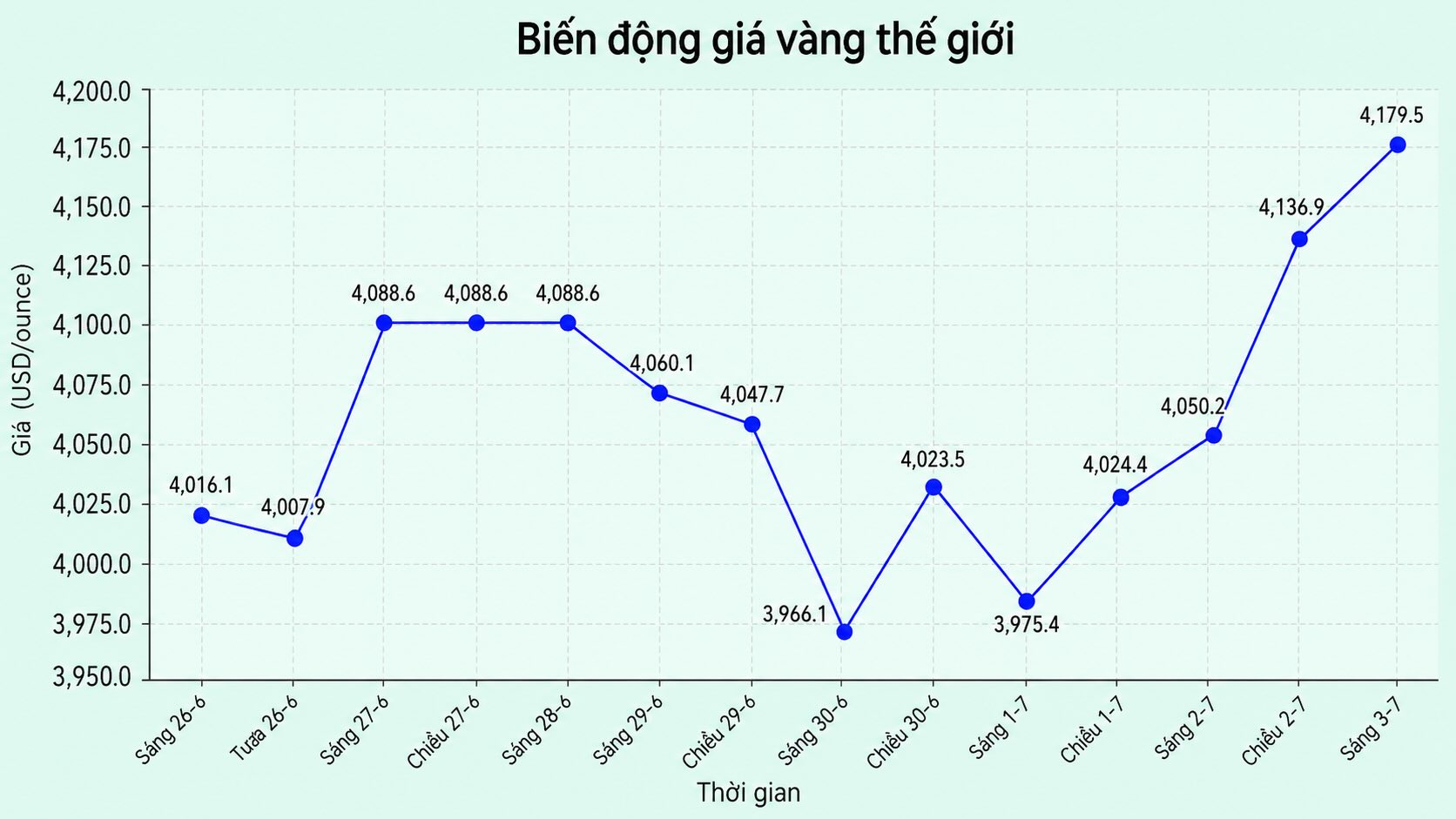

Latest update, international gold prices are fluctuating above the 4-150 USD/ounce range after a slight recovery last week. However, this precious metal is still significantly lower than the peak set at the beginning of the year, in the context of investors reducing expectations that the Fed will soon ease monetary policy.

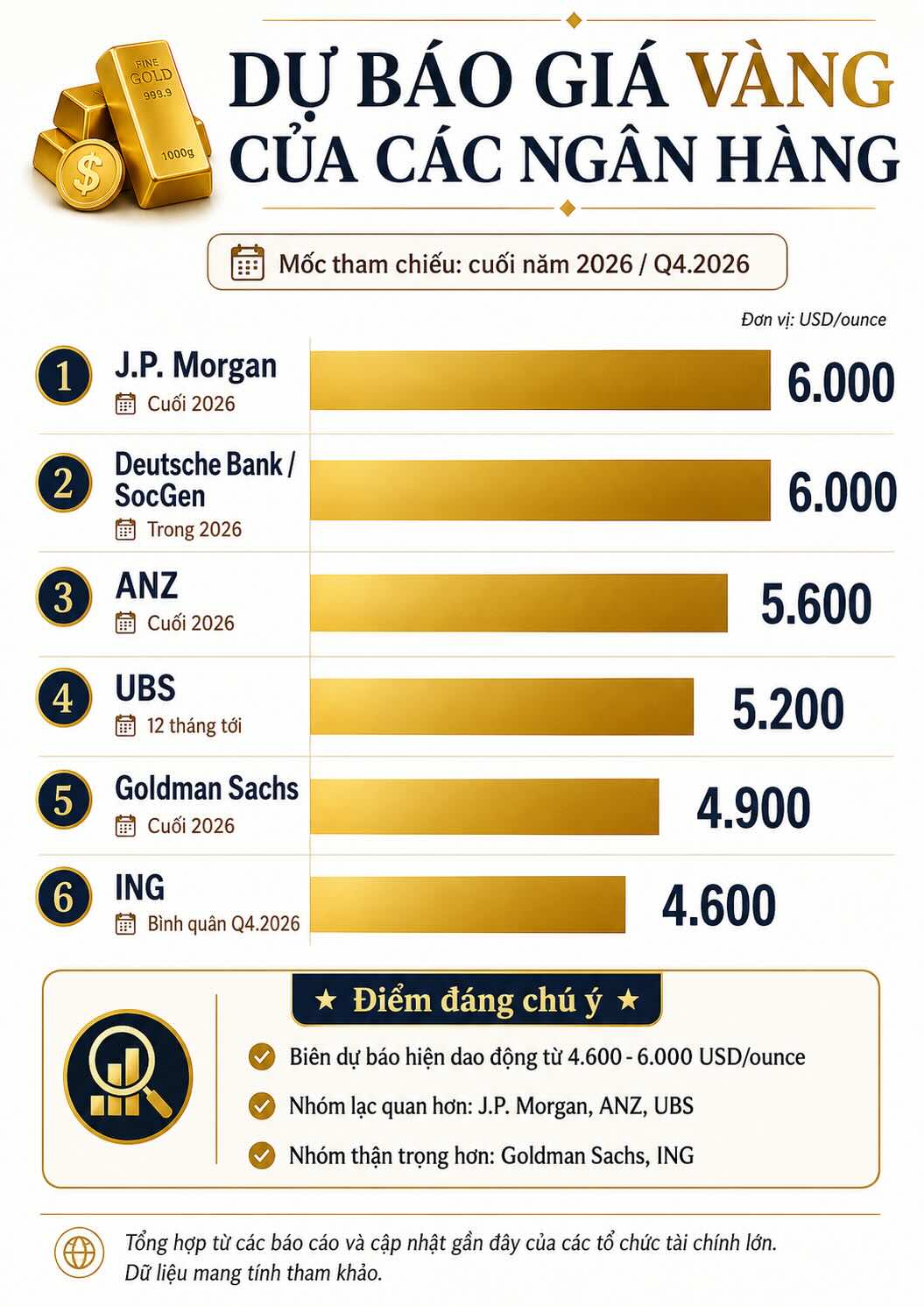

This adjustment has caused many major banks to reduce previous optimistic forecasts. ING currently forecasts the average gold price in Q3. 2026 at 4,300 USD/ounce and Q4. 2026 at 4,600 USD/ounce, lower than previous forecasts of 4,850 USD and 5,000 USD/ounce respectively.

Deutsche Bank also lowered its Q4 forecast to about 4,800 USD/ounce, while Goldman Sachs lowered its target for the end of 2026 to 4,900 USD/ounce. Bank of America acknowledged that the 6,000 USD/ounce mark, once considered a 12-month target, is now "hard to achieve in the short term".

However, the forecast picture is not entirely negative. J.P. Morgan still maintains a more positive view, saying that gold prices could rise to around 6,000 USD/ounce by the end of 2026, although the bank has lowered its annual average price forecast to 5,243 USD/ounce.

ANZ also cut its year-end target but still kept its forecast at a high level, around 5,600 USD/ounce. UBS even believes that gold prices may recover to around 5,200 USD/ounce in the next 12 months, thanks to the possibility of a weakening USD, expectations that the Fed will eventually have to cut interest rates and stable gold buying demand from central banks.

The common point in most reports is: interest rates, USD and ETF capital flows may dominate gold prices in the short term, but central bank buying power is the structural factor.

According to the latest survey by OMFIF, 82% of central banks surveyed currently hold physical gold, up from 71% last year.

Also according to this survey, 30% of participating units said they plan to increase allocation to gold in the next 1-2 years. Notably, 61% of respondents expect gold prices to trade in the 5,000-6,000 USD/ounce range in June 2027.

A World Gold Council survey also reinforces this trend. The 2026 report shows that 89% of central banks believe that total global official gold reserves will increase in the next 12 months.

In particular, 45% of central banks said they expect to increase their own gold holdings - a record high since the survey was conducted. The main reasons include diversification of reserve portfolios, inflation hedging, protection from geopolitical risks and reducing dependence on the USD.

This change reflects a larger trend in the global monetary system. Reuters quoted the OMFIF survey as saying that many central banks for the first time tend to want to reduce their USD holdings in the next decade rather than increase them further.

About 79% of central banks surveyed believe that the global monetary system is shifting in a multipolar direction. In that context, gold is considered a politically neutral asset, highly liquid and independent of any country's debt obligations.

In the short term, gold may still continue to fluctuate strongly. If the Fed maintains a tough stance, real yields increase and the USD maintains strength, gold prices may be under pressure and find it difficult to quickly return to the old peak. This is why cautious forecasts such as ING, Deutsche Bank or Goldman Sachs are leaning towards the 4,600-4,900 USD/ounce range for the end of 2026.

However, from a longer-term perspective, the central bank's continued increase in gold reserves is creating a sustainable support for the market. New mining supply is only gradually increasing over time, while formal demand from reserve managers remains at a historically high level. If the trend of dedollarization and geopolitical instability continues, gold may still maintain its role as one of the most important strategic reserve assets.