Clause 1, Article 2 of the draft Law on Special Consumption Tax stipulates the subjects subject to tax on goods as follows:

Cigarettes according to the provisions of the Law on Prevention and Control of Tobacco Harm; Alcohol according to the provisions of the Law on Prevention and Control of Alcohol and Beer Harm; Beer according to the provisions of the Law on Prevention and Control of Alcohol and Beer Harm;

Vehicles with engines under 24 seats, including: passenger cars; four-wheeled motorized passenger vehicles; passenger pick-up cars; double-cabin cargo pick-up cars; VAN trucks with two or more rows of seats, with a fixed divider design between the passenger compartment and the cargo compartment;

Two-wheeled motorbikes, three-wheeled motorbikes with a cylinder capacity of over 125cm3; Airplanes, helicopters, tourists and yachts; Gasoline of all kinds;

Coordinate the temperature with a capacity of over 18,000 BTU to 90,000 BTU except for the type according to the manufacturer's design only for installation on means of transport including cars, trains, ships, boats, and airplanes. In case the organization or individual producing and selling or the organization or individual importing separately each part is a hot or cold unit, the goods sold or imported (hot or cold unit) are still subject to special consumption tax as for the finished product (complete air conditioner); Leaf balls;

Gold codes, codes, excluding codes for children's toys, teaching aids;

Vietnam standard soft drinks (TCVN) have a sugar content of over 5g/100ml;

This goods is a complete product, excluding components for assembling goods;

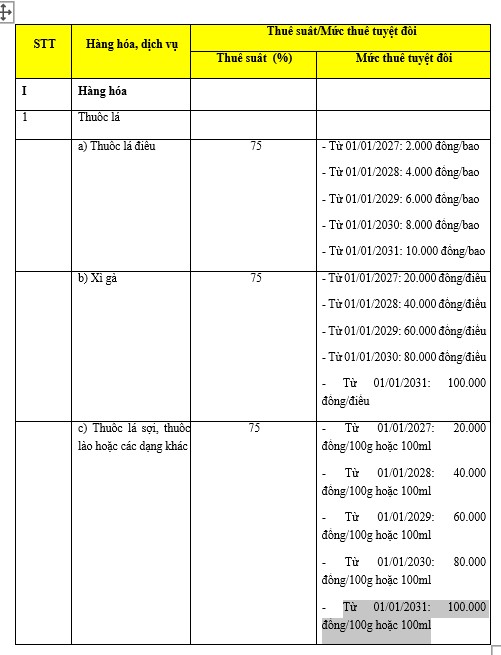

Article 8 of the draft stipulates the tax rate and absolute tax rate of special consumption tax on goods and services. In which the special consumption tax rate on tobacco is calculated according to the roadmap, in which the absolute tax rate on tobacco from January 1, 2021 will be 100,000 VND/tael.

Special consumption tax rates for cigarettes are as follows: