Continuing the 9th Session, on May 9, the National Assembly listened to Member of the National Assembly Standing Committee (NASC) Phan Van Mai present the Report on explanation, acceptance, and revision of the draft Law on Special Consumption Tax (SCT).

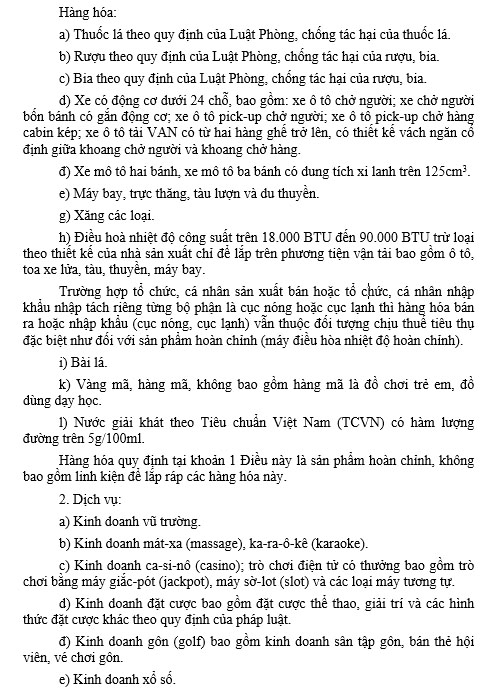

Regarding subjects not subject to tax, Article 3 of the Law on Special Consumption Tax (amended) clearly stipulates that goods specified in Clause 1, Article 2 of this Law are not subject to Special Consumption Tax in the following cases:

Goods are manufactured, processed, hired by organizations and individuals for direct export to foreign countries or sold or entrusted to other business organizations and individuals for export to foreign countries.

For imported goods, including:

Firstly, humanitarian aid and non-refundable aid, including imported goods using non-refundable aid funds approved by competent authorities, humanitarian aid and emergency relief goods to overcome the consequences of war, natural disasters and epidemics.

Gifts from organizations and individuals abroad to state agencies, political organizations, socio-political organizations, socio-political organizations - occupations, social organizations, socio-professional organizations, people's armed forces units, public service units within the quota are exempted from import tax according to the provisions of the law on export tax and import tax.

Gifts and gifts for individuals in Vietnam are exempt from import tax according to the provisions of the law on export tax and import tax.

Third, transit goods according to the provisions of commercial law, foreign trade management; imported and transit goods; goods from abroad imported to foreign warehouses and then exported to other countries according to the provisions of customs law.

Regarding this case, the Standing Committee of the National Assembly stated that even goods imported into the customs warehouse only for the purpose of sending, transit and then export to other countries will also have to be subject to special consumption tax. This is not in accordance with the principle of special consumption tax only applicable to goods consumed in Vietnam.

Next are temporary imported, re-exported and temporarily exported, re- Imported goods that do not have to pay import tax, export tax within the prescribed time limit of the law on export tax, import tax.

In case the re-export, re- import or sale period expires/use purpose changes during the temporary import or temporary export period, business organizations and individuals must pay special consumption tax.

Fifth, foreign organizations and individuals' items according to diplomatic exemption standards; goods carried in the luggage standard are exempted from import tax according to the provisions of the law on export tax and import tax; imported goods for sale at tax-free stores according to the provisions of law.

Sixth, goods exported abroad that have paid special consumption tax will be returned by foreign countries when imported.

Regarding this case, according to the Standing Committee of the National Assembly, in principle, goods exported abroad are not subject to special consumption tax, therefore, when imported back into Vietnam, special consumption tax must be applied similarly to other imported goods.

However, in the case of goods sold through commercial enterprises for export, the seller (producing enterprises or importing enterprises) must pay special consumption tax, Thus, if they continue to be taxed when imported due to being returned by customers, this amount of goods will be taxed twice.

The next case is airplanes, helicopters, hanging ships, yachts used for business purposes of transporting goods, passengers, tourists and airplanes, helicopters, hanging ships used for security and defense purposes, training pilots, spraying pesticides, fire fighting, filming, taking photos, measuring maps.

An ambulance; car carrying prisoners; funeral car; car designed with seating and standing seats for 24 or more people; passenger car, four-wheeled passenger car with engines that are not registered for circulation, do not participate in traffic and only run within the area of entertainment, entertainment, sports, historical sites, hospitals, schools and other specialized cars.

The draft Law on Special Consumption Tax (amended) is continuing to be discussed by the National Assembly. If approved by the National Assembly, this Law will take effect from January 1, 2026.