On March 5, 2026, Circular No. 18/2026/TT-BTC was issued, regulating tax management dossiers and procedures for business households and individual businesses.

Table of tax rates for households and individual businesses in 2026

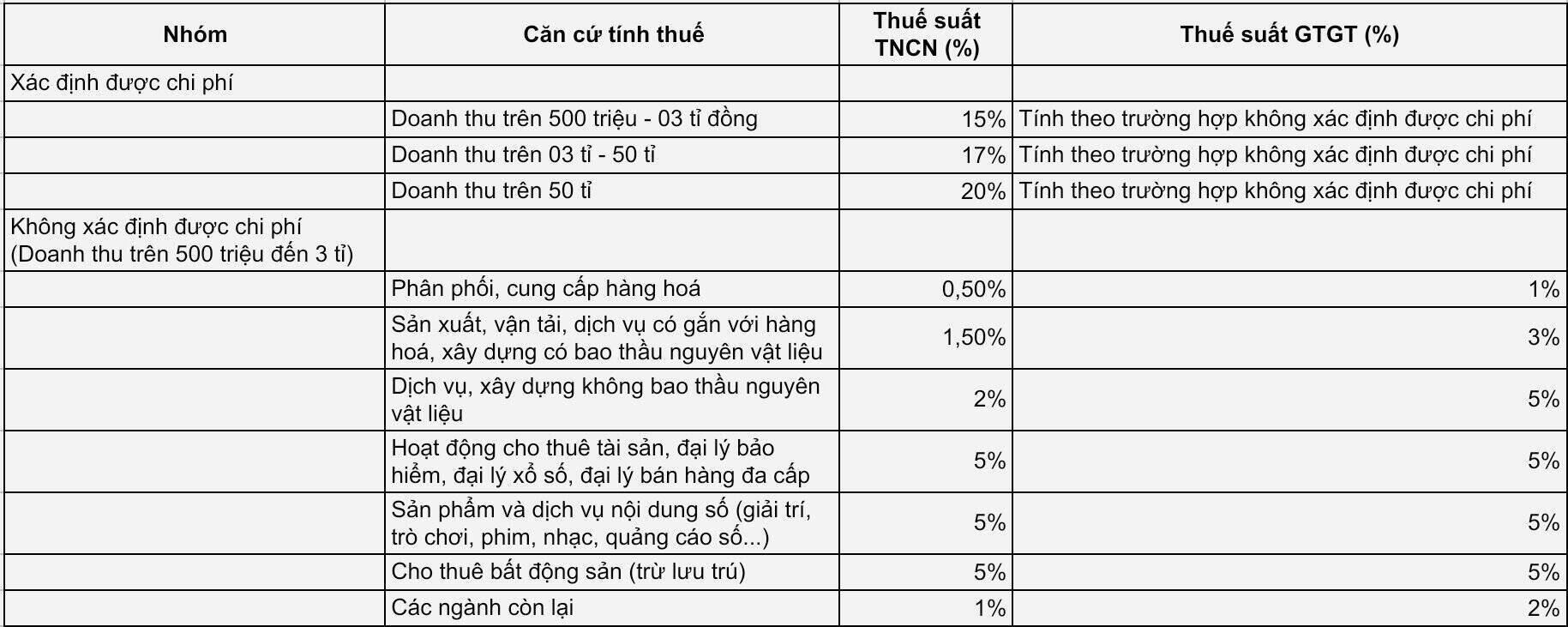

Below is a summary of the industry lookup table for value-added tax (VAT) and personal income tax (PIT) according to the latest regulations applied from 2026:

1. For business households that can determine costs

In this case, the PIT rate is calculated based on actual income (revenue minus reasonable expenses), specifically:

Revenue over 500 million to 03 billion VND: PIT rate 15%

Revenue over 03 billion VND to 50 billion VND: PIT rate 17%

Revenue over 50 billion VND: PIT rate of 20%

VAT rate: Calculated according to cases where costs cannot be determined.

2. For business households that cannot determine costs (Revenue over 500 million to 3 billion VND)

Taxpayers will apply a direct percentage of revenue depending on the sector:

Distribution, supply of goods: PIT rate 0.5% | VAT 1%

Manufacturing, transportation, services associated with goods, construction with raw material bidding: PIT rate 1.5% | VAT 3%

Services, construction without raw material bidding: PIT rate 2% | VAT 5%

Asset leasing, insurance agents, lottery, multi-level marketing: PIT rate 5% | VAT 5%

Providing digital content (entertainment, games, movies, music, digital ads): TNCN 5% | GTGT 5%

Real estate lease (excluding accommodation): Personal income tax 5% | VAT 5%

Remaining occupations: Personal income 1% | VAT 2%

Details of the quick lookup table of business household tax rates according to Circular 18/2026/TT-BTC:

Meaning of adjusting the new tariff

The introduction of specific tax rates for each group of subjects helps business households to be more proactive in accounting. In particular, the PIT rate from 15% to 20% for large-scale households (determining costs) helps ensure fairness between business households and businesses.

For medium-sized business households (from 500 million to 3 billion VND), if the management of input invoices is not strict, choosing to pay taxes at a direct percentage rate on revenue is still the simplest and easiest option to implement. Experts recommend that business households should rely on their actual operation to choose the most beneficial tax declaration method under the support of the automated declaration system of the tax authority.

KEY UPDATE: NATIONAL ASSEMBLY FINALIZES 500 MILLION VND TAX THRESHOLD

On the morning of April 24, 2026, the National Assembly officially passed the Law amending the Laws on Taxation with the following important changes:

Removing the fixed threshold of 500 million VND: The National Assembly agreed not to rigidly stipulate the figure of 500 million VND in the Law. Instead, the Government will flexibly stipulate the tax-free revenue threshold to suit the economic context of each period.

Expected to raise the tax exemption threshold to 1 billion VND: According to a report by the Ministry of Finance, the Government is expected to raise the non-taxable revenue level to 1 billion VND/year (instead of 500 million VND as previously regulated).

Beneficiaries: About 2.5 million households and individuals doing business with revenue below 1 billion VND are expected not to have to pay taxes under this new policy.

Corporate income tax exemption: Enterprises with total annual revenue not exceeding 1 billion VND are also expected to be exempt from corporate income tax.

The law takes effect from April 24, 2026.

(Source: According to the report on receiving and explaining of the Ministry of Finance at the National Assembly session on the morning of April 24, 2026)