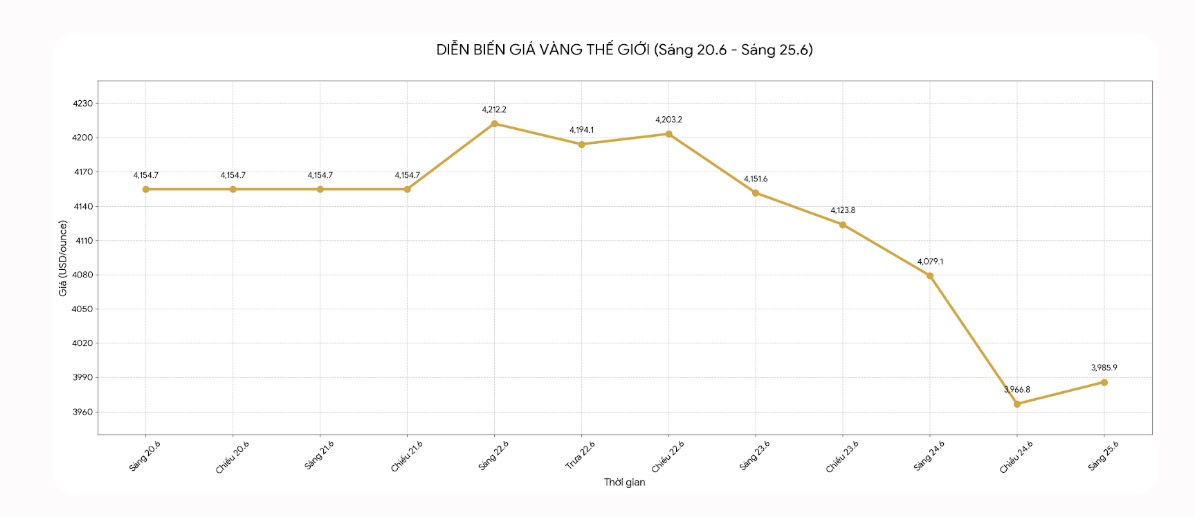

Faced with a series of pressures, gold prices fell below the 4,000 USD/ounce mark and touched a new low of the year. Meanwhile, silver prices have fallen below the 60 USD/ounce mark.

Although the downward correction of gold and silver from the historical peak set in January surprised many traders and experts, Ms. Ewa Manthey - commodity analyst at ING (a multinational financial and banking group) said that this sell-off reflects that the market is focusing more on high interest rate prospects and tighter financial conditions.

The market continues to react to the recent monetary policy meeting of the US Federal Reserve (Fed). Although the Fed kept interest rates unchanged, the agency signaled support for an interest rate hike this year.

Fed Chairman Kevin Warsh also emphasized that price stability is still the top priority. The market is currently assessing the possibility of the Fed raising interest rates right in September, and expects another wave of increases in December.

Strong monetary policy tightening expectations have pushed the USD Index back to the 100-point mark. Currently, this index is trading at 101.69 points - the highest since May 2025.

Faced with increasingly unfavorable factors for gold, Ms. Manthey said that ING has adjusted down its gold price forecast for the second half of the year.

Although still optimistic about the medium-term outlook for gold, the short-term environment has now become more difficult," she said.

ING currently forecasts that the average gold price will reach 4,300 USD/ounce in Q3/2026 and 4,600 USD/ounce in Q4/2026, lower than previous forecasts of 4,850 USD and 5,000 USD/ounce respectively.

Although ING does not expect the Fed to raise interest rates this year, Ms. Manthey believes that investors should not go against market trends.

High yields and a strong USD may continue to be factors putting pressure on gold in the short term," she said. "Geopolitical tensions have not created strong safe-haven cash flow as in previous periods of instability. Instead, the market focuses on the inflation impact of geopolitical developments and possible consequences for monetary policy.

ING also lowered its silver price forecast. The organization currently expects the average silver price to reach 68 USD/ounce in the third quarter and 74 USD/ounce in the fourth quarter, down from previous forecasts of 79 USD and 84 USD/ounce respectively.

Although the silver market is forecast to continue to lack supply, some of the strongest demand growth drivers are gradually weakening. Demand from the solar energy industry is slowing down, while measures to reduce and replace silver in photovoltaic panel production continue to reduce the amount of silver used on each panel," Ms. Manthey said.

Although gold and silver are forecast to face a difficult environment in the second half of the year, Ms. Manthey believes that the fundamental structural factors of the market have not changed.

The demand for buying gold from central banks is still very strong, the trend of diversifying foreign exchange reserves continues and geopolitical risks remain high.

However, rising yields and weakening investment demand are creating greater pressure than our previous forecasts. The gold correction has forced ING to re-adjust forecasts, but does not change the overall view of the market," she said.

We still believe that long-term drivers supporting gold prices remain intact, although the price increase process may be slower and more volatile than previously expected. Despite lowering forecasts, we still believe that silver will have slightly higher growth than gold, thanks to prolonged supply shortages and the trend of electrification of the economy.