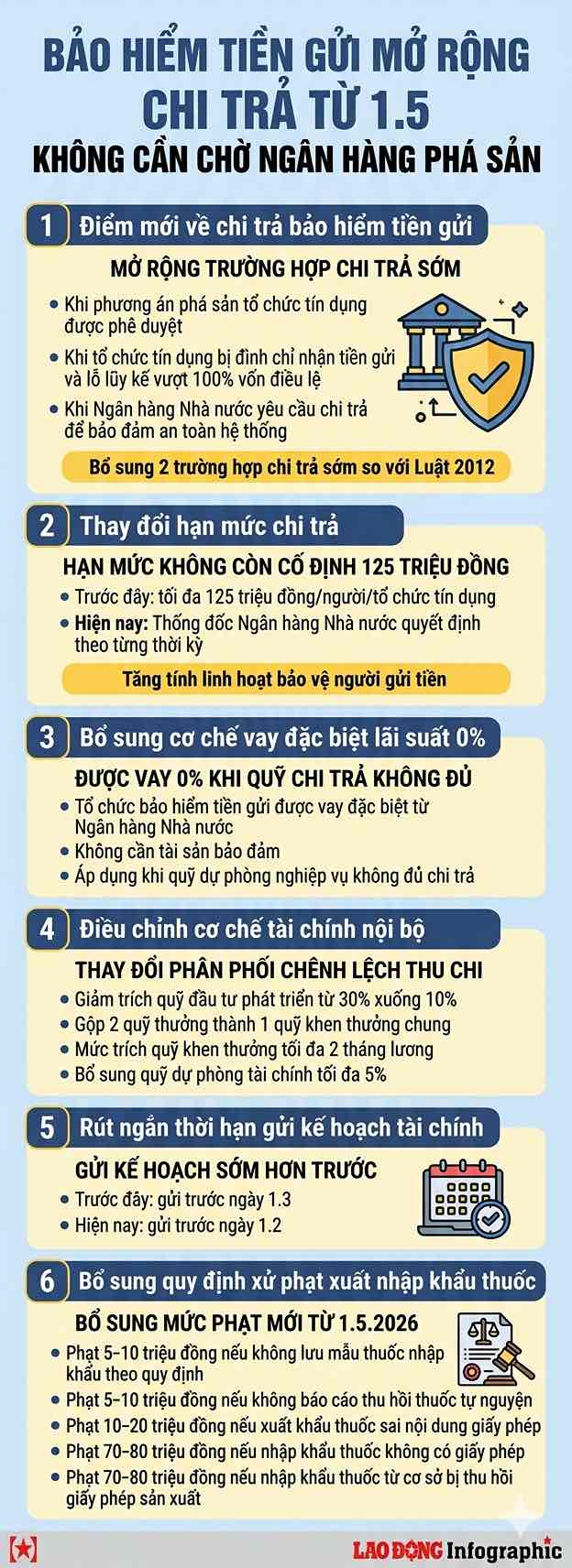

From May 1, 2026, many new regulations on deposit insurance officially take effect under the 2025 Deposit Insurance Law and Circular 33/2026/TT-BTC, in which the expansion of cases of early insurance payment, adjustment of the mechanism for determining payment limits and supplementation of liquidity support tools for deposit insurance organizations are noteworthy.

Expanding the case of deposit insurance payment

Previously, according to Article 22 of the 2012 Deposit Insurance Law, the obligation to pay insurance premiums mainly arose when credit institutions still fell into bankruptcy after the end of special control or when the State Bank determined that a foreign bank branch lost the ability to pay deposits.

According to Article 21 of the 2025 Deposit Insurance Law, the obligation to pay insurance premiums arises from one of the following times:

The bankruptcy plan of the credit institution is approved or the State Bank determines that the foreign bank branch is unable to pay deposits to depositors.

The State Bank of Vietnam suspends the receipt of deposits by specially controlled credit institutions in cases where credit institutions have accumulated losses greater than 100% of charter capital and reserve funds according to the latest audited financial statements.

The State Bank of Vietnam notifies deposit insurance organizations to carry out payments to ensure system safety, order, and social safety when credit institutions lose or are at risk of losing solvency.

The addition of two cases of early payment is considered an important new point, contributing to stabilizing the psychology of depositors and limiting the risk of mass withdrawals at weak credit institutions.

The deposit insurance payment limit is decided by the State Bank for each period.

Previously, according to Decision 32/2021/QD-TTg, the maximum payment limit for all insured deposits (including principal and interest) of one person at an organization participating in deposit insurance was 125 million VND.

According to Clause 1, Article 22 of the 2025 Deposit Insurance Law, the payment limit will be decided by the Governor of the State Bank of Vietnam for each period.

The new regulation helps management agencies flexibly adjust payment limits in accordance with economic fluctuations and inflation, thereby improving the ability to protect depositors.

Supplementing a special 0% interest loan mechanism when the fund is insufficient to pay

According to Clause 1, Article 38 of the 2025 Deposit Insurance Law, deposit insurance organizations are entitled to special loans from the State Bank of Vietnam at 0% interest and do not need collateral when the nghiệp vụ reserve fund is not sufficient to fulfill payment obligations.

Insufficient provision fund is determined when the deposit insurance organization has used up the fund but has not yet met the payment obligation.

In addition, the sale of unvalid valuable papers or the withdrawal of unvalid deposits must ensure the principle of capital preservation in investment activities.

The new regulation helps increase the proactive ability of resources to pay in systemic risk situations.

Adjusting the mechanism for distributing financial revenue and expenditure differences annually

According to Article 17 of Circular 33/2026/TT-BTC, the mechanism for distributing financial revenue and expenditure differences of Vietnam Deposit Insurance is adjusted in the direction of changing the rate of fund allocation.

Specifically, the rate of deduction of development investment funds decreased from a maximum of 30% to a maximum of 10%.

The two bonus funds for managers and the bonus fund for employees are merged into a common bonus fund to cover reward and welfare activities.

The level of bonus and welfare fund allocation for units ranked B is adjusted to a maximum of no more than 2 months' salary.

In addition, supplement regulations to deduct a maximum of 5% into the financial reserve fund, with the maximum level of the fund not exceeding 20% of the charter capital of Vietnam Deposit Insurance.

Adjusting the deadline for submitting annual financial plans

Circular 33/2026/TT-BTC also adjusts the deadline for financial plan submission of Vietnam Deposit Insurance.

Accordingly, before February 1 every year, based on the operating results of the previous year, Deposit Insurance of Vietnam must review and complete the financial plan and send it to the State Bank and the Ministry of Finance to serve financial supervision and evaluate operational efficiency.

This regulation is earlier than before when the deadline for submitting financial plans was implemented before March 1 according to Circular 312/2016/TT-BTC.