Based on Article 7 of Circular 111/2013/TT-BTC amended in Clause 6, Article 25 of Circular 92/2015/TT-BTC stipulating the method of calculating personal income tax (PIT) 2026 according to the new family deduction level as follows:

Personal income tax on income from business, from salaries, wages is the total tax calculated according to each income grade. The tax calculated according to each income grade is equal to the taxable income of the income grade multiplied (×) by the corresponding tax rate of that income grade.

Accordingly, the 2026 PIT calculation formula according to the new personal income tax deduction level, specifically as follows:

PIT payable = Taxable income x Tax rate

In which:

- Taxable income = Taxable income - Deductions (familial deductions; insurance contributions, voluntary pension funds; charity, humanitarian, and scholarship contributions);

Resolution 110/2025/UBTVQH15 increases the family circumstance deduction from 2026, specifically as follows:

- The deduction level for taxpayers is 15.5 million VND/month (186 million VND/year);

- The deduction level for each dependent person is 6.2 million VND/month.

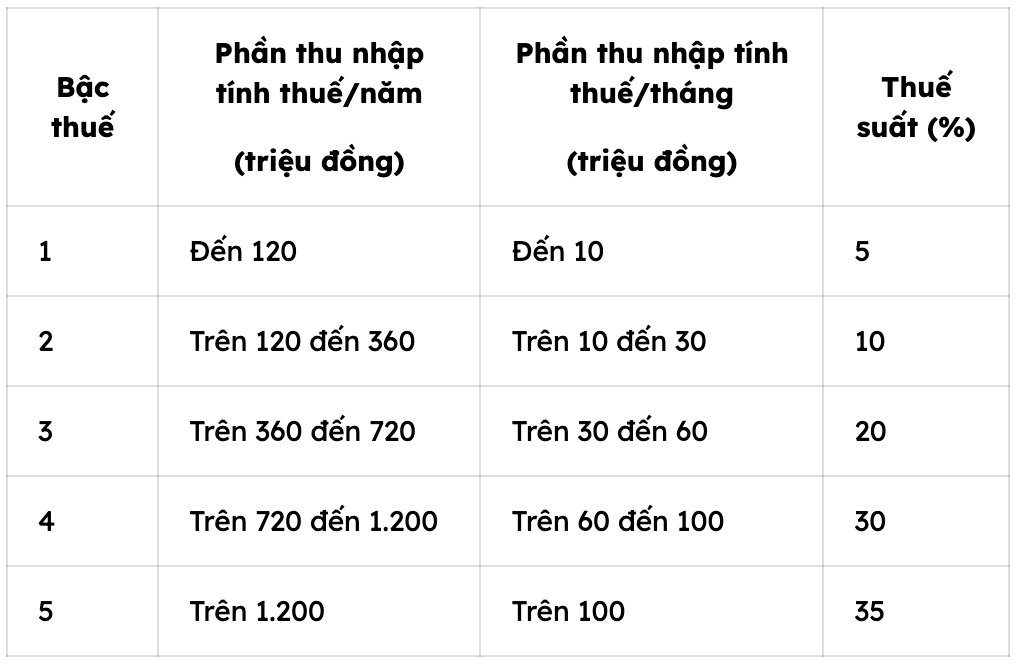

- Tax rate:

The progressive tax schedule of 5 levels is newly applied from the tax period of 2026, i.e. from 01.01.2026 as follows:

For example, Ms. C has an income from salary and wages in the month of 50 million VND and pays insurance amounts of: 8% of social insurance, 1.5% of health insurance on salary, 1% of unemployment insurance. Ms. C raises 2 children under 18 years old, in the month Ms. C does not contribute to charity, humanitarian work, or education promotion. Personal income tax temporarily paid in the month of Ms. C is calculated as follows:

- Ms. C's taxable income is 50 million VND.

- Ms. C is entitled to deduct the following amounts:

+ Discount for personal circumstances: 15.5 million VND

+ Family circumstance reduction for 02 dependents (2 children):

6.2 million VND × 2 = 12.4 million VND

+ Social insurance, health insurance, unemployment insurance:

(46.8 million VND × (8% + 1.5%)) + (50 million VND ×1%) = 4.4 million VND + 500 thousand VND = 4.9 million VND.

Total deductible amounts:

15.5 million VND + 12.4 million VND + 4.9 million VND = 32.8 million VND

- Ms. C's taxable income is:

50 million VND - 32.84 million VND = 17.1 million VND

- Tax amount to be paid:

The amount of tax payable is calculated according to each step of the new progressive tax schedule:

+ Step 1: taxable income up to 10 million VND, tax rate 5%:

10 million VND × 5% = 0.5 million VND

+ Step 2: taxable income over 10 million VND to 30 million VND, tax rate 10%:

(17,154 million VND - 10 million VND) × 10% = 0.7154 million VND

- The total amount of tax Ms. C must temporarily pay in the month is:

0.5 million VND + 0.7154 million VND = 1.2154 million VND.

It's a bit of a bit of a bit of a bit of a bit of a bit.