Vietnam's foreign exchange reserves have gone through three clear stages

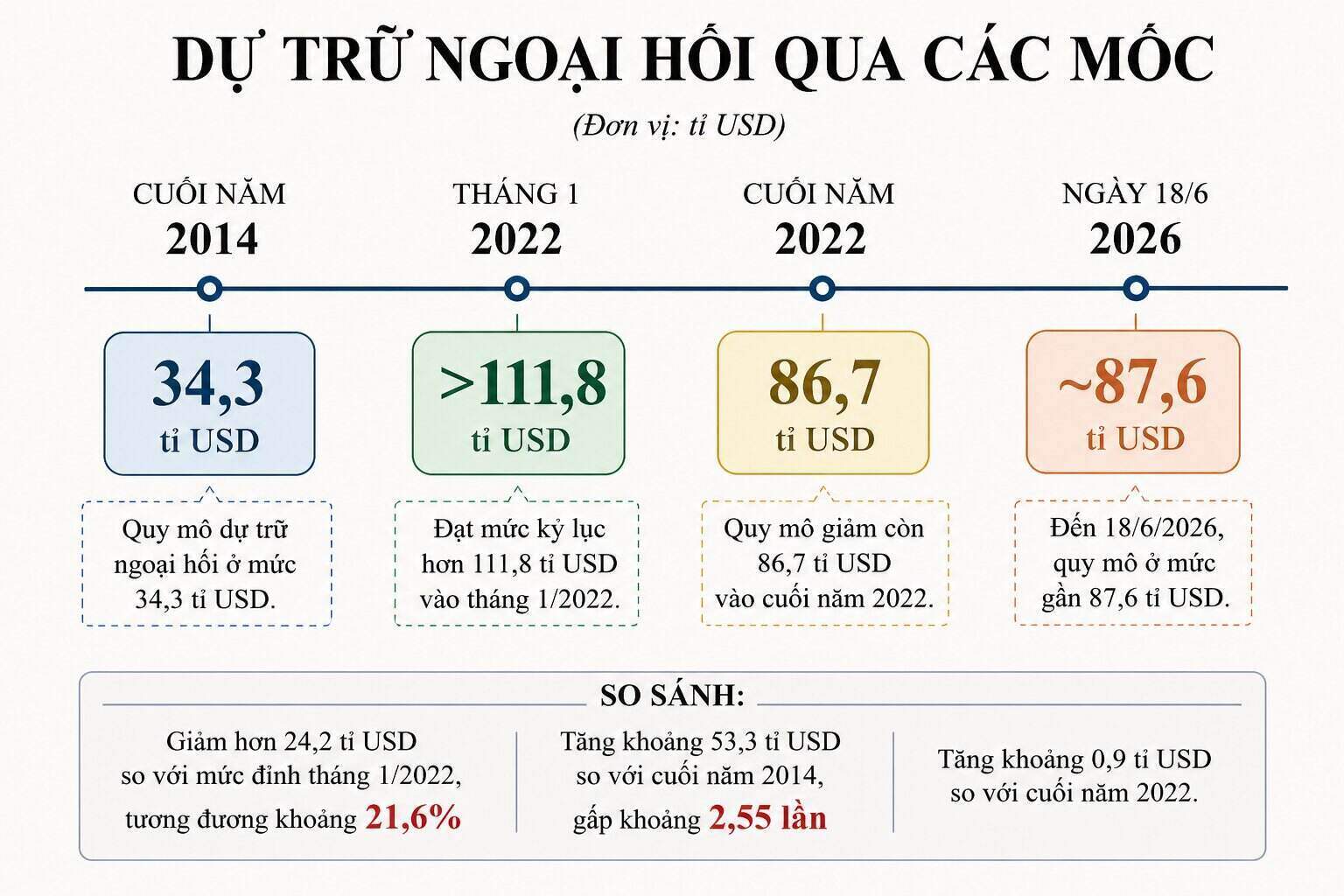

According to the draft Report summarizing the implementation of Decree No. 50/2014/ND-CP on the management of state foreign exchange reserves of the State Bank, as of June 18, 2026, the scale of Vietnam's foreign exchange reserves is nearly 87.6 billion USD.

This figure is 24.2 billion USD lower than the record level of over 111.8 billion USD recorded in January 2022. According to the milestones announced by the State Bank, the scale of foreign exchange reserves has decreased by about 21.6% compared to the peak.

The data series in the report shows that Vietnam's foreign exchange reserves have gone through three distinct phases: rapid increase before 2022, sharp decrease in 2022 and relatively stable maintenance in recent years.

At the end of 2014, the scale of new foreign exchange reserves was at 34.3 billion USD. In the period of favorable market conditions, the State Bank bought foreign currency to supplement reserves, thereby bringing the scale of foreign exchange reserves to a record level of more than 111.8 billion USD in January 2022.

Thus, in more than 7 years, foreign exchange reserves have increased by at least 77.5 billion USD.

However, by the end of 2022, the scale of foreign exchange reserves decreased to 86.7 billion USD. Compared to the peak at the beginning of the year, the decrease in 2022 alone reached more than 25.1 billion USD, equivalent to about 22.5%.

By June 18, 2026, foreign exchange reserves reached nearly 87.6 billion USD, about 900 million USD higher than at the end of 2022. This shows that most of the decrease compared to the peak occurred in 2022; the size of reserves then did not continue to decrease deeply but fluctuated around 87 billion USD.

Compared to the end of 2014, the current reserve level is still about 53.3 billion USD higher and about 2.55 times higher.

Foreign exchange reserves are used to stabilize the market

According to the State Bank of Vietnam, the departure of foreign exchange reserves from the peak level needs to be placed in the context of strong exchange rate and international currency market fluctuations since the beginning of 2022.

In the period from the beginning of 2022 to the end of 2024, the US Federal Reserve implemented an interest rate hike cycle and maintained interest rates at a high level. Along with that were the impacts of the COVID-19 epidemic, the uncertainty of trade policy, tariffs, geopolitical conflicts, rising energy prices and supply chain disruptions.

These factors put pressure on the exchange rate and increased the need for intervention in the domestic foreign exchange market. The State Bank said it has used foreign exchange reserves to intervene, contributing to market stability.

According to the report, foreign currency liquidity in the past time was still ensured smoothly. The legitimate foreign currency needs of the economy, including foreign currency for importing goods and raw materials for production, are fully met.

Foreign exchange reserves are also used as a buffer for the State Bank to coordinate with other monetary policy tools, stabilize the market, control inflation and support economic growth.

Foreign currency flow between the budget and the State Bank changes direction

Another notable change mentioned in the report is the foreign exchange balance of the state budget.

In the previous period, the foreign currency revenue of the budget was often greater than the spending needs. The state budget therefore sold foreign currency to the State Bank many times, thereby supplementing foreign currency sources for foreign exchange reserves.

However, in recent years, the foreign currency revenue of the budget is often not enough to meet the demand for foreign currency spending. The budget incurs a need to buy foreign currency from the State Bank or the market to offset the shortfall.

Thus, the foreign currency flow has had a significant change: from a budget that regularly has surplus foreign currency to sell and supplement reserves, to a state where at times it is necessary to buy foreign currency to serve foreign debt repayment, development investment, equipment import and other foreign currency spending needs.

To handle this situation, the draft amendment to Decree 50 proposes that in case the Ministry of Finance cannot balance foreign currency from the budget, funds and other foreign currency sources managed by the Ministry of Finance, it will buy foreign currency from credit institutions.

If the source of foreign currency purchased from the market still does not meet the demand, the Ministry of Finance will coordinate with the State Bank to sell foreign currency to the state budget.

In the opposite direction, the remaining foreign currency of the budget after being kept within the permitted limit will be sold to the State Bank to supplement official foreign exchange reserves. In case the State Bank refuses to buy, the Ministry of Finance is allowed to sell to credit institutions licensed to trade in foreign currencies.