Vietnam is entering a new era with two goals: Becoming a developed country with high income by 2045 and achieving Net - Zero by 2050. These are two challenging goals because they must fundamentally transform the economy, promote growth in the direction of innovation, digital transformation and green transformation, replacing the growth model based on resource and labor intensity in recent years.

In the context of double-digit growth in the 2026-2030 period and green transformation becoming a global trend, the demand for clean, renewable energy will increase strongly, becoming one of the key factors ensuring rapid and sustainable growth.

Vietnam's current power source structure still depends heavily on traditional energy sources that cause high emissions. As of 2024, nearly 50% of the national electricity output will still come from coal. This proportion not only puts great pressure on the implementation of international commitments on reducing greenhouse gas emissions but also increases the risk of costs, environmental pollution and increases dependence on scarce resources.

According to a report by the World Bank, with more than 3,260 km of coastline, low-lying riverbanks and tropical climate, Vietnam is at the forefront of climate change risks. Hot spells, floods, rising sea levels and super typhoons are not only environmental issues but also threaten food security, infrastructure, industry and urbanization.

Although Vietnam has great potential to develop renewable energy sources, the development of new power sources in recent years has encountered many barriers. The lack of synchronous power transmission infrastructure makes it impossible for many renewable power projects to generate electricity to the grid. The unstable electricity purchase price mechanism, inconsistent legal policies, along with the prolonged appraisal and approval process have slowed down the implementation progress of many large projects. In addition, domestic private enterprises are also having difficulty accessing long-term capital and high-quality technical human resources for green transformation projects.

As a highly open economy, Vietnam is increasingly affected by new trends and policy tools in the world. Key export markets such as the US and EU are tightening standards through new non-tax barriers such as CBAM, CSRD and green requirements in the global supply chain. In that context, green transformation is no longer an option, but has become a prerequisite to maintain national competitive advantage and the position of key export products in the world market.

The major orientations of the Party today, expressed through the "quartet" include: Resolution No. 57 (on breakthrough in science and technology development, innovation and transformation of national numbers), Resolution No. 59 (on international integration in the new situation), Resolution No. 66 (on renovation of construction and law enforcement to meet the country's development requirements in the new era). New 2.0 ”, creating a solid policy corridor for transformation of growth model. Combined with internal potential and international commitment, this is the time when Vietnam is ripe for Vietnam to regenerate energy policies, which depend on fossil fuels to led by green energy, reconstructed with the private sector as the main force of tectonic and assist.

Energy conversion for green growth and sustainable development goals

double-digit growth will lead to demand for electricity consumption

In 2025, it has a particularly important meaning, the year of acceleration, breakthrough, finishing, and the last year of implementing the 5 -year socio -economic development plan 2021-2025, implementing the revolution of streamlining the organizational structure, conducting the Party Congress at all levels to go to the XIV National Congress of the Party and preparing, strengthening the foundation elements, as a strong and prosperous era of our country, the people of the country are strong and prosperous in the age of the country. The tribe, aiming to successfully implement the strategic goals of socio -economic development 10 years 2021-2030.

Resolution No. 25/NQ-CP of the Government on growth targets for sectors, fields and localities ensures the national growth target of 8% or more in 2025, creating a solid foundation to achieve double-digit growth rates in the period of 2026-2030. The Resolution is accompanied by Appendix I on a number of growth targets for sectors and fields and Appendix II on the GRDP growth target for 2025 of provinces and centrally run cities.

In which, TT 11, Appendix I set the target in 2025: The growth rate of total power production and import of the whole system is from 12.5% -13% and the Ministry of Industry and Trade is the agency in charge of monitoring and evaluation. In Resolution No. 192/2024/QH15 of February 28, 2025 of the National Assembly on supplementing the socio -economic development plan in 2025 with the goal of growth of 8% or more. The National Assembly sets the goal of 2025 to promote growth with the goal of 8% or more associated with maintaining macroeconomic stability; Control inflation, ensure the great balance of the economy; harmoniously developing economy and society and environmental protection, ensuring national defense and security; Create a premise to grow higher in the following years. In Article 2 of the main tasks and solutions: The National Assembly will soon enact the Law on Atomic Energy (amended); Review and immediately have solutions to handle problems that are entangled, especially renewable energy projects ...; promote green and new energy conversion (according to Resolution 57-NQ/TW); Enhancing high -quality human resource training according to international standards to meet the needs of the market, especially industries such as atomic energy ...

With the GDP growth target of 8% or more in 2025 and aiming for double-digit growth in the 2026-2030 period, the requirements for national energy infrastructure will become more urgent and challenging many times. According to technical calculations, with the assumption that the electricity elasticity coefficient compared to GDP is 1.5 - meaning that every time GDP increases by 1%, electricity demand increases by 1.5%, if GDP growth in 2025 reaches 8%, electricity demand will increase by about 12%. This is equivalent to the requirement to add about 2,2002,500 MW of new electricity capacity in just one year, putting great pressure on both source investment and the power grid.

In the "Adjusting the National Power Development Plan for the period 2021-2030, with a vision to 2050" (adjusted PDP 8), the GDP growth scenarios have been converted and divided into many stages. Accordingly, the trade electricity elasticity coefficient on GDP is recorded to tend to decrease gradually through each stage:

● 20112015 period: 1.86

● 20162020 period: 1.44

● Phase 20212024: 1.08

In the following planning stages, this coefficient is forecast to continue to decrease:

● 20262030 period: 1.261.28

● 20312035 period: 0.900.95

● 20362040 period: 0.630.71

● Phase 20412045: 0.330.49

● By 2050: ranging from 0.100.44 (depending on the scenario)

The gradual decline of the electrical elasticity coefficient on GDP is a common trend in countries that are shifting the phase from industrialization to knowledge economy. In the early stages of industrialization, the power growth rate is usually higher than the GDP growth rate due to the strong development of sectors with large energy intensity. However, when the economic structure gradually shifts to service, high technology and large added value production but less energy consumption, electric/GDP elasticity coefficient will decrease. This is also the development trend that Vietnam is aiming for in the next decade - rapid growth but on the basis of efficiency and sustainability of energy.

The problem for Vietnam is not only to quickly supplement power source capacity, but also to simultaneously restructure the energy supply and demand model in a long-term and sustainable direction. In particular, the urgent requirement is to improve energy efficiency, gradually reduce the electricity elasticity coefficient on GDP, which is still at a high level, and gradually perfect mechanisms and policies to encourage the development of renewable, green and low-emission energy sources. This is a prerequisite to meet the increasing demand for electricity in the process of economic development.

According to the new growth goals, in which the GDP growth orientation reaches two numbers in the period of 2026–2030, the energy -forecasting scenario determined by the Ministry of Industry and Trade will be a high scenario. This means that the electricity needs will be under great pressure in both medium and long term. At the same time, in order to meet climate commitments and implement the roadway reduction roadmap, Vietnam must reduce the proportion of coal power in the total power structure. Therefore, the pressure to increase electricity production must be resolved by increasing the proportion of renewable energy sources such as wind and solar power, while speeding up the green conversion process throughout the national energy system.

Overview of the electricity industry and risks if the conversion is slow

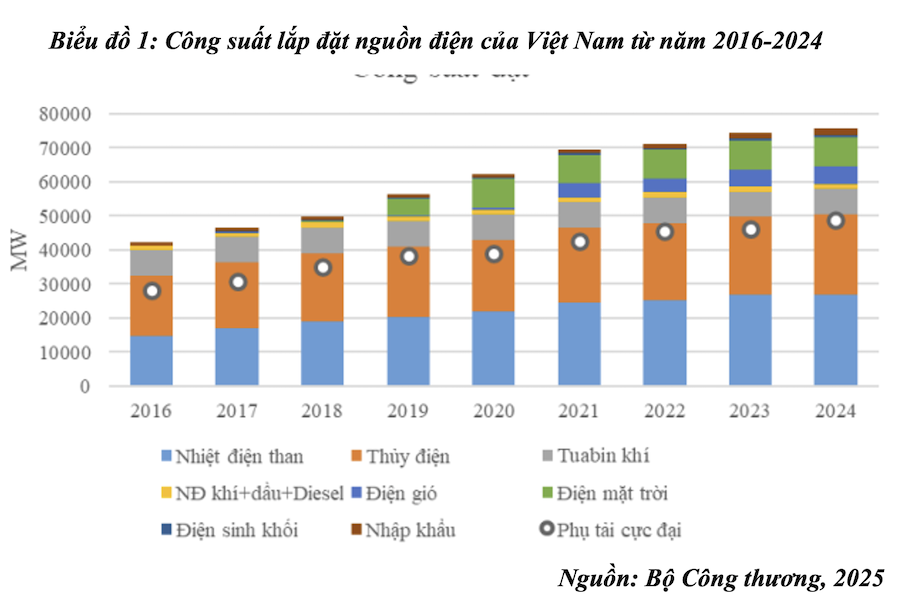

In the period 20162024, the total installed capacity of the Vietnamese power system has nearly doubled, from about 42 GW to about 75 GW (excluding rooftop solar power) as shown in chart 1. Before 2019, the power source system mainly relied on traditional power plants such as coal-fired thermal power, thermal gas and hydropower. However, since 2019, under the positive impact of the Government's incentive mechanisms, solar and wind power sources have made significant progress, starting to make an important contribution to the national power source structure.

The national power development plan for the period 2021-2030, with a vision to 2050 (QHD VIII), issued in May 2023 and recently adjusted in Decision No. 768/QD-TTg dated April 15, 2025, clearly defines the orientation for the development of the electricity industry in a modern, sustainable and environmentally friendly direction, aiming to achieve the goal of net zero emissions by 2050.

Vietnam signed the Joint equitable energy transition (JETP) Agreement in December 2022 - an international initiative to mobilize financial and technological resources to support the green transition process. According to the JETP content, Vietnam aims to reduce emissions from the energy sector to 170 million tons of CO2e by 2030, keeping coal-fired power capacity at a peak of 30.2 GW and raising the proportion of renewable energy in electricity output to 47%.

According to QHD VIII, the total power source capacity is targeted at 150 GW by 2030 and 490573 GW by 2050. In terms of structure, employees are expected to account for 3139% by 2030, or higher if JETP is fully implemented, and 67.571.5% by 2050.

As of 2024, the Vietnamese power system has recorded nearly 9 GW of solar power (excluding rooftop) and over 5 GW of wind power. Meanwhile, traditional power sources still account for a large proportion with a total capacity of about 58 GW, including: 26 GW coal thermal power, 23 GW hydropower and 7 GW gas turbines.

In the period of 20212024, many large-scale thermal power projects have been put into operation, including: Song Hau 1 (1,200 MW), Nghi Son 2 (1,320 MW), Duyen Hai 2 (1,320 MW), Thai Binh 2 (1,320 MW) and Van Phong 1 (1,332 MW).

Regarding the trend of the source structure, the ratio of hydroelectricity (including small hydroelectricity) shows signs of decreasing due to the almost exhausted exploitation potential, only about 31% of the total power structure in 2024. Solar and wind energy has made great development from nearly zero in 2018, by 2024, 12% and 7% of the total capacity were set. In contrast, gas turbine power is not added in recent years, causing the proportion to decrease from 18% in 2016 to 10% in 2024. The remaining types of power sources now account for a relatively small proportion in the whole system structure.

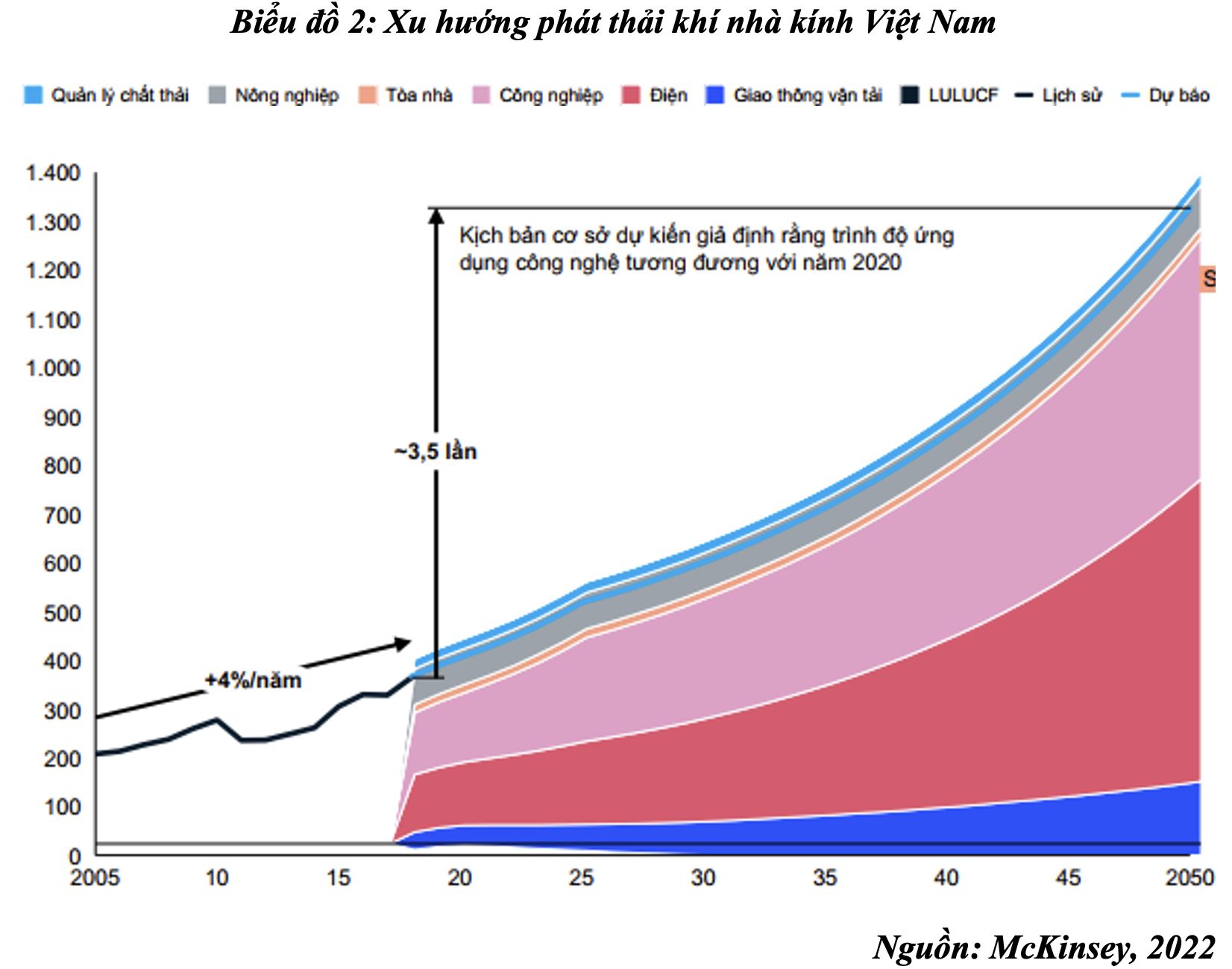

According to McKinsey, the energy sector is the largest source of emissions in the structure of 7 main sectors of Vietnam. In the non-actional scenario, Vietnam's total GHG emissions could increase 4 times by 2050, compared to nearly 364 million tons of CO2e. The emissions of the energy sector by 2050 could reach approximately 600 million tons of CO2e with an expected growth rate of 5.3%.

Although Vietnam has clearly announced its emission reduction target by 2030 and 2050, McKinsey emphasized that specific solutions in the electricity industry need to be implemented immediately to realize these commitments. Specifically, Vietnam needs to add at least 150 GW of wind power equivalent to about 23% of the estimated theoretical potential of 650 GW, and at the same time develop about 70 GW of solar power to account for 18% of theoretical potential of about 380 GW. The power generation structure needs to be adjusted so that renewable energy accounts for over 80%, combined with improving the storage and transmission capacity of electricity from regions with large production potential such as the Central Highlands and the South Central Coast to large load centers such as Ho Chi Minh City and Hanoi.

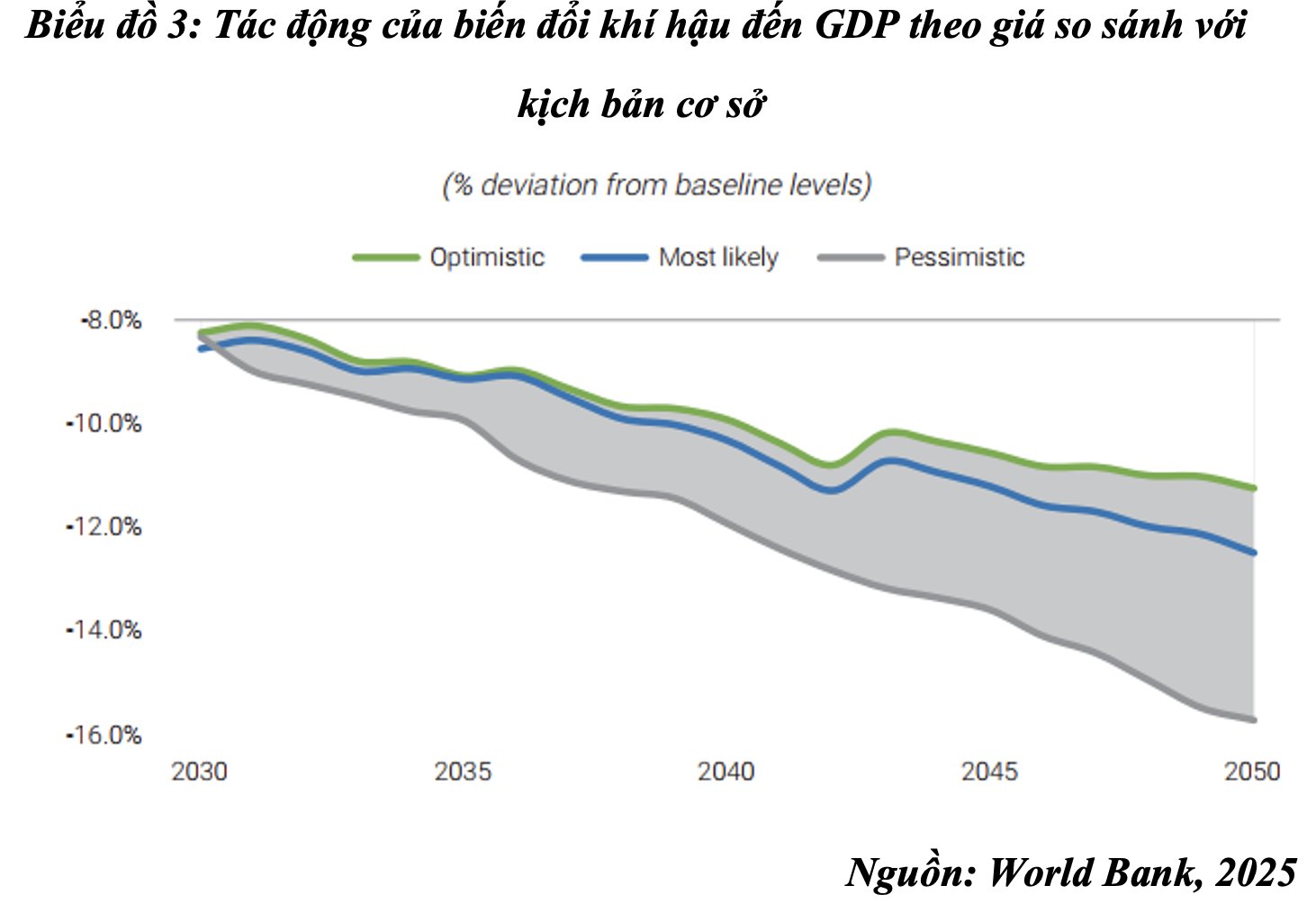

If the transition process to a green growth model is delayed, Vietnam will face a series of serious economic, social and national competitiveness risks - not only in the long term but in the next decade. The report "Growing Greener - Pathways to a Resilient and Sustainable Future" of the World Bank has pointed out the risks from climate change directly related to economic growth. Without timely acting of Vietnam's actual GDP, it may decrease by 9.1% by 2035 and 12.5% in 2050 compared to the basic scenario. This impact comes from three main channels: (1) Reducing labor productivity due to stress due to high temperatures, (2) loss of property and infrastructure due to natural disasters, and (3) damage in agriculture. Even in the period of 2020–2030, this impact was able to reduce the average real growth rate of 0.5 percentage points per year, and lasted to the 2040s with a decline in 0.25 percentage points per year.

Potential of renewable energy in Vietnam

Vietnam possesses a particularly favorable geography for developing solar power and wind power. With more than 3,260 km of coastline, the average wind speed reaches 7 m/s, along with the average solar radiation level of 1,3871,534 kWh/kWp/year in the Central Highlands, South Central and Southern regions. In addition, Vietnam also has the potential to take advantage of biomass energy sources with a total potential of up to 50 million tons of oil converted (TOE). According to the World Bank's assessment results, Vietnam is a country with greater wind energy potential than countries in the region such as Cambodia, Laos, and Thailand.

In addition to "new" renewable energy sources such as solar power, wind power, and biomass power, Vietnam is also developing other sources such as electricity from sea waves and Biogas biogas, combined with traditional sources such as LNG, hydropower, and electricity to diversify the energy structure and increase the flexibility of the system.

Vietnam is ranked 31st globally in terms of attractiveness in investment and implementation of renewable energy (2021). According to data from the Foreign Investment Agency (Ministry of Planning and Investment), in the period of 2020-2021, total FDI investment in the electricity production and distribution sector will reach over 5.1 billion USD, an increase of more than 4 times compared to the previous year, mainly in solar power and wind power projects in the Central and Southern coastal areas.

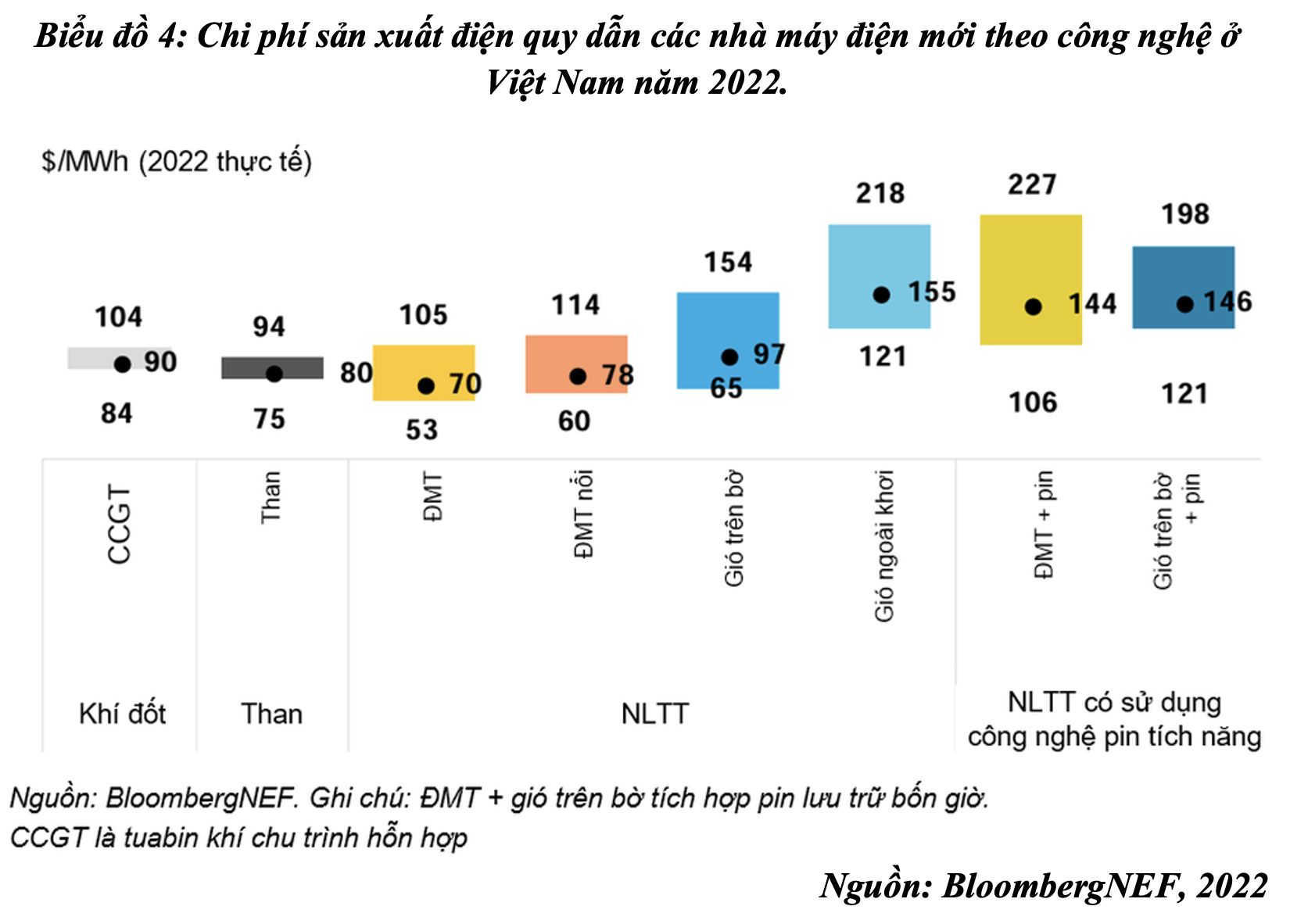

In addition, the cost of investment and production of renewable energy is decreasing sharply, improving competitiveness compared to traditional sources. According to Bloomberg New Energy Finance (Bloomberg NEF), the cost of producing LCOE (Levelized Cost of Electricity) for solar power in Vietnam is getting cheaper. According to the actual price in 2022, it is 53-105 USD/MWh. The LCOE of wind power has also decreased significantly, at 65-154 USD/MWh. Thanks to advances in technology and market size, improved installation and maintenance capabilities, increasingly reasonable prices for solar and wind power production in Vietnam, stable production capabilities, and increased market opportunities.

From 2022 onwards, investment in on land wind power has become cheaper than investment in building new coal-fired thermal power plants. Vietnam is also forming a domestic supply chain with the participation of ph photovoltaic battery manufacturing plants, while owning a relatively synchronous transmission system and technical infrastructure, creating favorable conditions to expand large-scale renewable energy projects.

Difficulties of businesses in green transformation

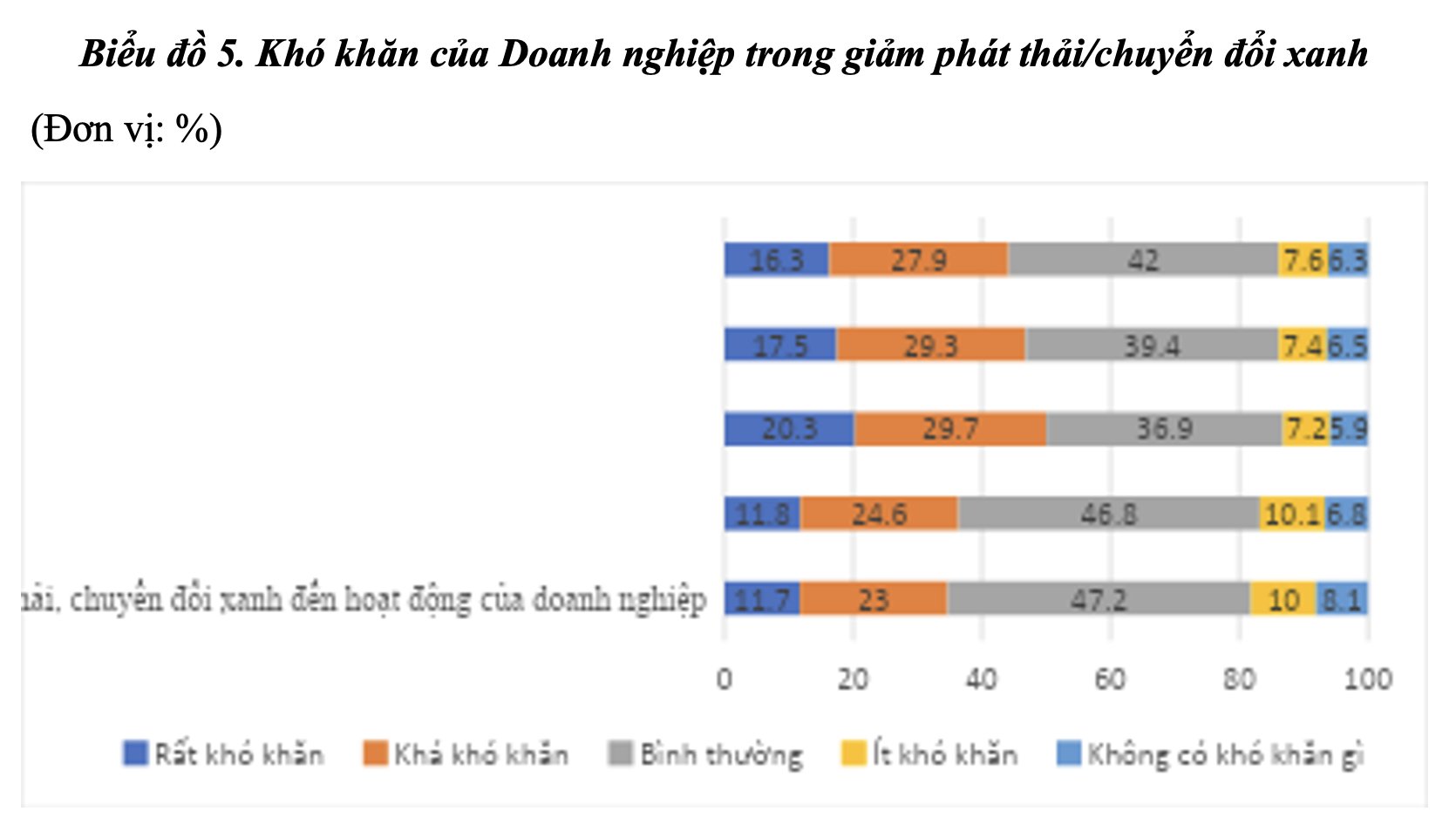

According to a survey conducted by Board IV in 2024, the majority of enterprises in Vietnam are facing many barriers in the process of reducing emissions and converting to green. The three biggest difficulties identified by businesses include: (i) lack of capital to implement emission reduction solutions; (ii) lack of professional and experienced personnel in the field of green transformation; and (iii) lack of specific technical solutions, suitable for the production and business conditions of the business ( charter 4).

In which, the problem is considered the biggest obstacle. Up to 50% of surveyed enterprises said they were facing difficulties in capital, while only 5.9% said they did not encounter any obstacles. The rate of enterprises in the processing - manufacturing and agricultural - forestry - fishery industries facing capital difficulties is 53.7% and 52.9%, respectively. Domestic enterprises are facing more difficulties than FDI enterprises (50.3% compared to 46.6%). Notably, mid-sized enterprises are the group facing the largest capital difficulties with 62.7% of enterprises with revenue from VND1,000 - 1,500 billion saying they lack financial resources for green transformation.

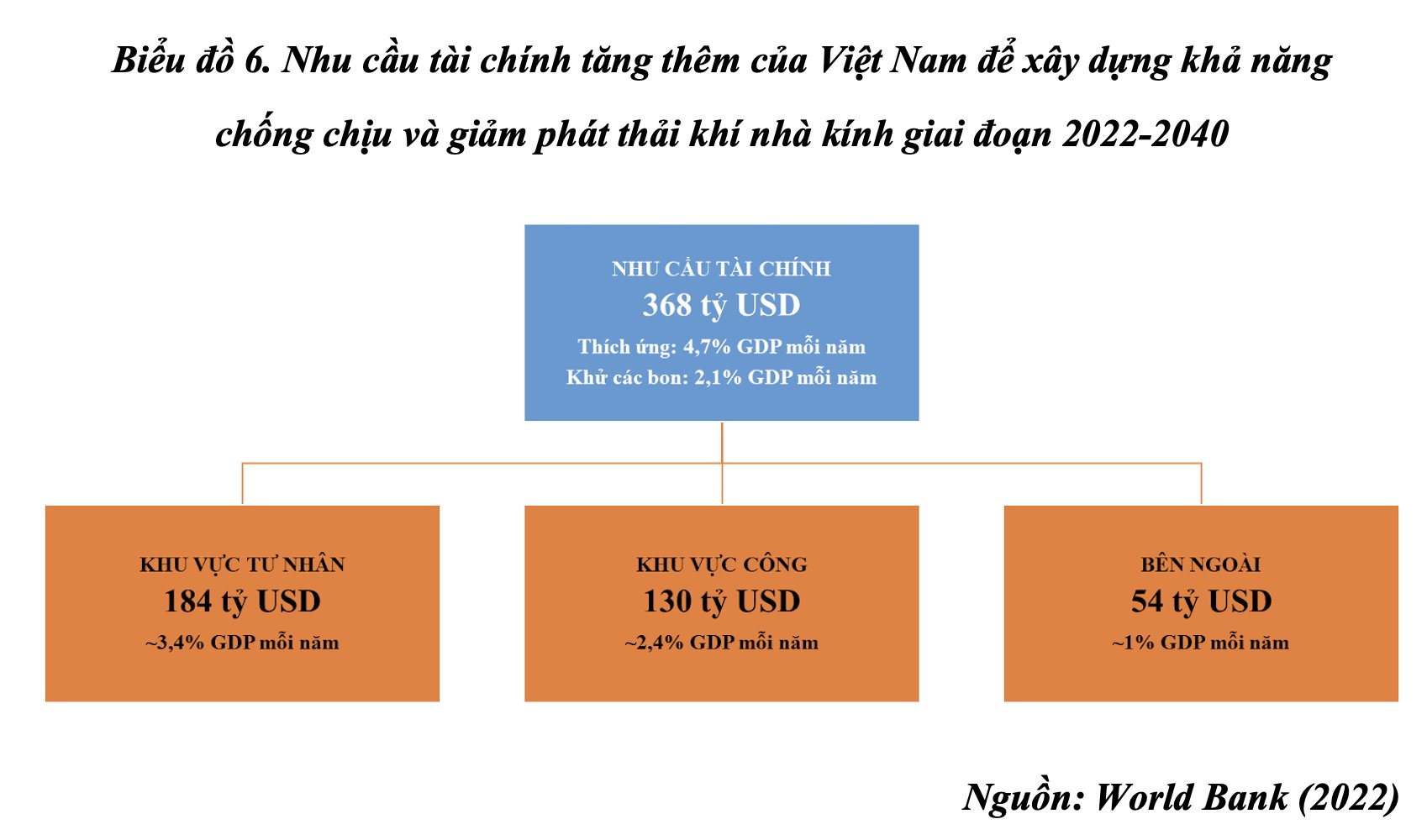

While demand is already huge, Vietnam's green finance market is still developing slowly. According to the World Bank's estimate (2022), Vietnam needs about 368 billion USD in the period of 2022-2040 to build resilience and reduce greenhouse gas emissions, equivalent to 6.8% of GDP per year. Of which, the private sector is expected to mobilize nearly 184 billion USD, or nearly 50% of total capital demand.

However, in fact, the green credit scale is still very limited. By the end of 2023, the entire green credit balance was nearly 621,000 billion VND, accounting for about 4.5%of the total outstanding loans of the economy, mainly focusing on renewable energy, clean energy (nearly 45%) and green agriculture (30%). The implementation of green credit still faces many problems, such as lack of clear legal framework, lack of synchronous policies, capital sources of credit institutions are mainly short & medium -term capital, while green projects need long -term capital and preferential interest rates. For green bonds, there is still a lack of detailed guidance on project criteria, capital surveillance mechanism, and transparent legal regulations.

In addition, accessing international financial resources, despite their great potential, is not easy. JETP Partnership plans to allocate 15.5 billion USD in the 2024-2028 period to support Vietnam in implementing energy transition projects. However, most of this financial amount is only disbursed to projects that have not yet mobilized capital or are "in the idea proposal stage". International organizations have reflected that the implementation progress is still slow, along with many barriers to administrative procedures, appraisal, and compliance with international standards, limiting the ability of businesses to access JETP capital.

If there are no solutions to remove bottlenecks in institutions, capital and technical capacity soon, the green transformation process of enterprises, especially the domestic private sector, will be slow down, reducing the effectiveness of national commitments on climate and wasting opportunities to access global financial resources.

Some proposals

In order to achieve the national dual target and effectively implement the guidelines and guidelines of the Party and the State shown in the newly issued central resolutions, it is necessary to build a system of systematic renewable, synchronized and highly enforcement energy development policies. This policy framework should be designed with a specific implementation roadmap, clearly defining the roles - responsibilities - powers of stakeholders (state management agencies, localities, businesses, financial institutions), along with effective assessment indicators (KPIS) established from the beginning to ensure progress, quality and transparency in deployment.

First of all, it is necessary to urgently issue a Prime Minister's Decision stipulating criteria for confirming green projects, as a foundation for granting green credit, issuing green bonds and accessing other preferential mechanisms. The draft Decision clearly identifies project types in 7 key economic sectors, with transparent assessment methods that can be measured and verified. The completion of this legal framework will help promote the formation of a domestic green financial market, while creating favorable conditions for domestic enterprises to access preferential capital sources and join the global supply chain with low emission standards.

Second, it is necessary to effectively implement Decree No. 57/2025/ND-CP on direct power purchase and sale mechanism (Direct PPA), allowing large power users to sign contracts directly with renewable energy power generation units. This is an important step in the process of developing a competitive electricity market and forming green industrial clusters. To promote this mechanism effectively, the Government, ministries and relevant departments need to simultaneously issue specific technical instructions on connection, allocation of transmission costs, payment mechanisms and ensuring system safety.

Thirdly, it is necessary to promote the pilot implementation of the domestic carbon market in accordance with the roadmap in Decree No. 06/2022/ND-CP. Including the establishment of carbon credit exchanges, completing the measurement - reporting - evaluation system (MRV), and testing of emission quotas by industry. The connection of the domestic carbon market with international mechanisms such as credit exchange mechanism under Article 6 of Paris agreement will create new financial motivation, promoting high commercial clean energy projects.

Fourth, it is necessary to continue to invest synchronously in energy infrastructure, especially transmission and storage systems, associated with the planning of integrating electricity - land - sea. The development of renewable energy on a large scale is only truly effective when the power system is capable of absorbing and distributing it properly. Therefore, inter-regional transmission, acumulation and hydropower projects and power storage projects need to be included in the priority list for public investment and international cooperation.

Resolution No. 57-NQ/TW of the Politburo on scientific and technological development, innovation and conversion of national numbers have clearly defined energy, especially new energy, clean energy is one of the central areas that need to be prioritized for infrastructure investment, promoting application research and strategic technology development. At the same time, Resolution No. 68-NQ/TW on the development of the private economy continues to affirm the role of the private sector is an important driving force, aiming to quickly form and develop large private enterprises in the fields of the pillar, including energy industry, in association with national key projects and global value chains.

In fact, the demand for a consistent, transparent and predictable policy system, which clearly affirms the principle that every private enterprise is entitled to participate in areas that are not banned by law, ensuring the principle of non -re -accusation and protecting legal rights through effective contract implementation. Ensuring a stable and public legal environment is a key factor for the private sector to be assured to invest in the energy sector, contributing to meeting the increasing power demand for the two -digit economic growth goals of the period of 2026–2030, as well as successfully implementing development goals to 2045 and 2050.

At the same time, there should be a focused selection policy to attract private investment in renewable energy infrastructure, support the formation of large-scale energy technology enterprises, and promote the development of an innovation ecosystem in the energy industry. In particular, it is necessary to implement programs to support small and medium enterprises to build sustainable development strategies according to ESG standards, access to green credit, improve technical capacity and train human resources in accordance with the requirements of a low-carbon economy.