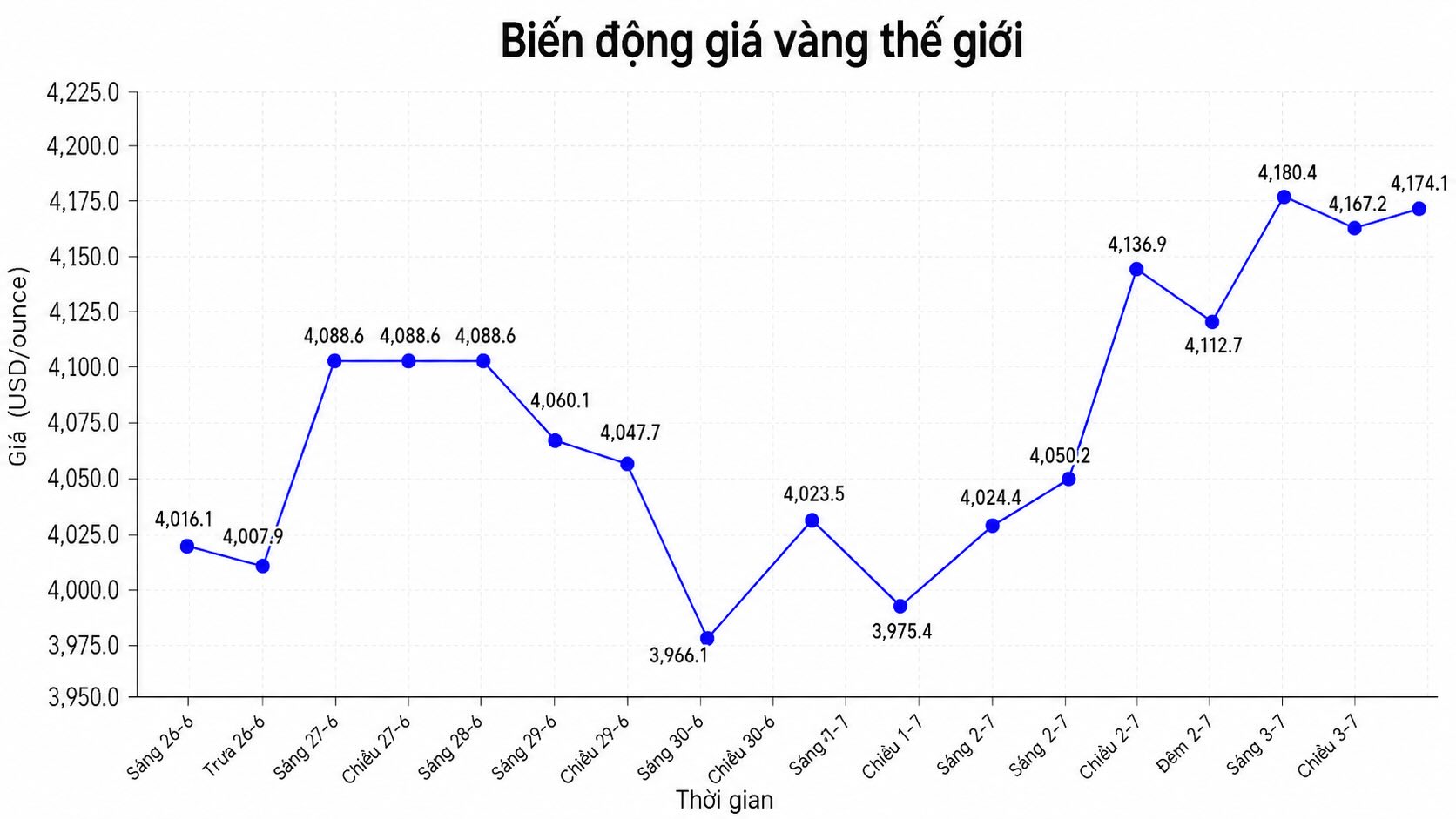

After a period of strong increase, world gold prices have shown a significant correction, raising the question of whether the prolonged price increase cycle of the precious metal is weakening?

According to some major financial institutions, gold may not be easy to break through immediately in the short term because real yields are still high. As yields increase, the opportunity cost of holding gold - non-interest-generating assets - also increases. A strong USD also makes gold more expensive for investors holding other currencies.

However, a noteworthy point is that most medium and long-term forecasts still lean towards a positive trend. Organizations such as State Street Global Advisors, HSBC, Goldman Sachs as well as surveys from the World Gold Council and OMFIF all emphasize a common factor: Structural gold demand has not yet weakened, especially from central banks.

Cautious scenario: Gold fluctuates in the range of 4,000-4,750 USD/ounce

In a less positive scenario, gold prices may continue to move sideways or recover limitedly if US yields are high and the USD has not weakened significantly. This is an unfavorable environment for gold, because when yields increase, the opportunity cost of holding non-rentable assets such as gold also increases.

State Street believes that short-term resistance forces such as high yields, strong USD and the possibility of the Fed maintaining a tough stance may cause gold to fluctuate around the 4,000-4,750 USD/ounce range. HSBC also believes that gold is likely to still trade in a narrow range in the short term, as high real yields continue to limit the upward momentum.

A noteworthy factor is that gold did not increase as strongly as expected during the Middle East tension period. According to HSBC, this does not mean that gold lost its shelter role. As oil prices rise, fears of inflation return, yields and the USD rise together, a part of investors have sold gold to increase liquidity. In other words, gold is still a defensive asset, but it can be realized into cash when the market is tense.

Base scenario: Gold heading towards 4,750-5,500 USD/ounce

In the base scenario, gold prices still have room to increase from the end of 2026 to the beginning of 2027, although the diễn biến may not be flat. State Street forecasts gold may rise to the 4,750-5,500 USD/ounce range in the next 6-9 months. This organization believes that physical gold demand in Asia, central bank buying power and portfolio diversification demand will continue to support prices.

World Gold Council data shows that central banks net bought 41 tons of gold in May, the second highest level since the beginning of the year. Poland was the largest buyer with 18 tons, China bought 10 tons, while Uzbekistan, Kazakhstan and Singapore also recorded remarkable buying power.

Since the beginning of the year, Poland has bought 64 tons of gold, Uzbekistan bought 33 tons, China bought 25 tons and Kazakhstan bought 20 tons. These figures show that the official sector's gold buying activity is not just a short-term response, but associated with a reserve restructuring strategy.

A World Gold Council survey also shows a record 45% rate of central banks expecting to increase gold holdings in the next 12 months. Meanwhile, nearly 90% of central banks believe that global official gold reserves will continue to increase. OMFIF also noted that many reserve managers expect gold prices to trade in the range of 5,000-6,000 USD/ounce in the coming year.

According to HSBC, portfolio diversification needs, buying power from central banks and stable ETF capital flows are factors that help maintain a positive view on gold in the medium term. In the context of stocks and bonds tending to fluctuate more synchronously, gold continues to be seen as a tool to help reduce portfolio risk.

Positive scenario: Gold surpasses 5,500 USD/ounce

In a positive scenario, gold prices could surpass 5,500 USD/ounce if many supporting factors appear: the Fed shifts to a softer stance, the USD weakens, ETF capital returns strongly and central banks continue to buy gold at a high level.

State Street offers a strong increase scenario with the range of 5,500-6,250 USD/ounce, although the probability is lower than the base scenario. Goldman Sachs also believes that demand from the official sector is still an important pillar of the market, and forecasts that gold prices may approach 4,900 USD/ounce next year.

In addition to China and major gold buyers in Asia, the gold accumulation trend also appears in some central banks in Latin America. South Korea is also said to have prepared to invest in gold ETF funds abroad to diversify foreign currency assets.