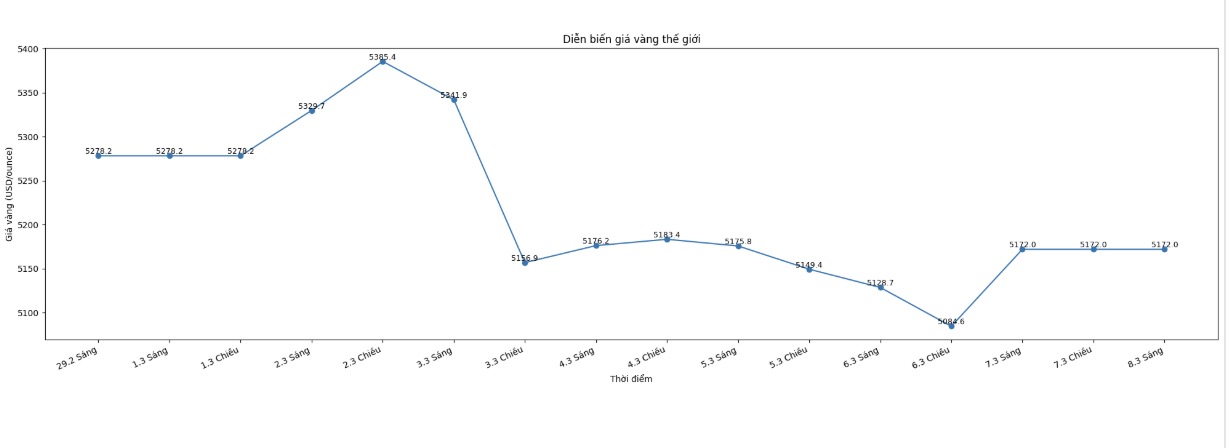

The trading week began with a familiar reaction. After the US and Israel launched missiles into Iran when the market opened on Sunday evening, gold prices quickly surged, reaching 5,400 USD/ounce. However, this upward momentum did not last long. The wave of price increases triggered strong selling pressure as many traders took advantage of profit-taking, causing prices to quickly fall back.

Gold price increases in the role of safe-haven assets are often difficult to maintain for long. The market usually reacts very quickly to geopolitical shocks, but when the initial wave of concern subsides, traders often return to focus on broader macroeconomic factors.

This seems to have happened this week as investors re-evaluate the impact of rising energy prices, currency fluctuations, and monetary policy expectations.

While geopolitical tensions are increasing, gold is facing an important resistance: a stronger USD and expectations that the US Federal Reserve (Fed) may not have much room to ease monetary policy in the short term.

Conflicts in the Middle East have pushed energy prices up and raised concerns about inflationary pressure returning. Rising oil prices could spread throughout the global economy, causing transportation and production costs to increase.

If inflationary pressures persist, central banks may be forced to maintain tight or neutral monetary policy, even if economic growth slows down.

For the Fed, this creates a difficult problem. The risk of prolonged inflation may prevent policymakers from cutting interest rates as quickly as the market expects.

High interest rates and high US Treasury bond yields often support the USD, while increasing opportunity costs when holding non-performing assets such as gold.

However, gold prices still maintained the support zone at historical highs, showing that fundamental demand is still quite strong. Many analysts believe that there are structural factors that can limit the increase in interest rates. As global public debt increases, borrowing costs maintained at high levels for a long time will put great pressure on the government budget.

At some point, central banks may be forced to cut interest rates or intervene in the bond market to maintain economic stability.

Currently, global financial markets seem to have not yet valued a prolonged geopolitical crisis. Some analysts believe that the latest military escalation may still be under control, allowing the market to gradually stabilize as tensions cool down.

However, the longer the conflict lasts, the greater the risk of financial instability returning. Prolonged instability in the Middle East will increase the possibility that investors will once again turn to gold as a tool to hedge geopolitical and economic risks.

In addition to the immediate crisis, many analysts believe that the long-term outlook for gold is linked to structural changes in the global economy. The trend of deglobalization, geopolitical fragmentation and the use of economic tools as a "weapon" are forcing many countries to reconsider financial alliances and reserve strategies.

Although the buying rate has slowed down, central banks continue to increase gold reserves to diversify assets and reduce dependence on the USD. In an increasingly multipolar financial system, gold is still one of the few assets with global liquidity that is not associated with political or partner risks.

Although gold price fluctuations in the short term may still be strong, major pushes that are reshaping the global economy show that demand for this precious metal is unlikely to decline in the near future.