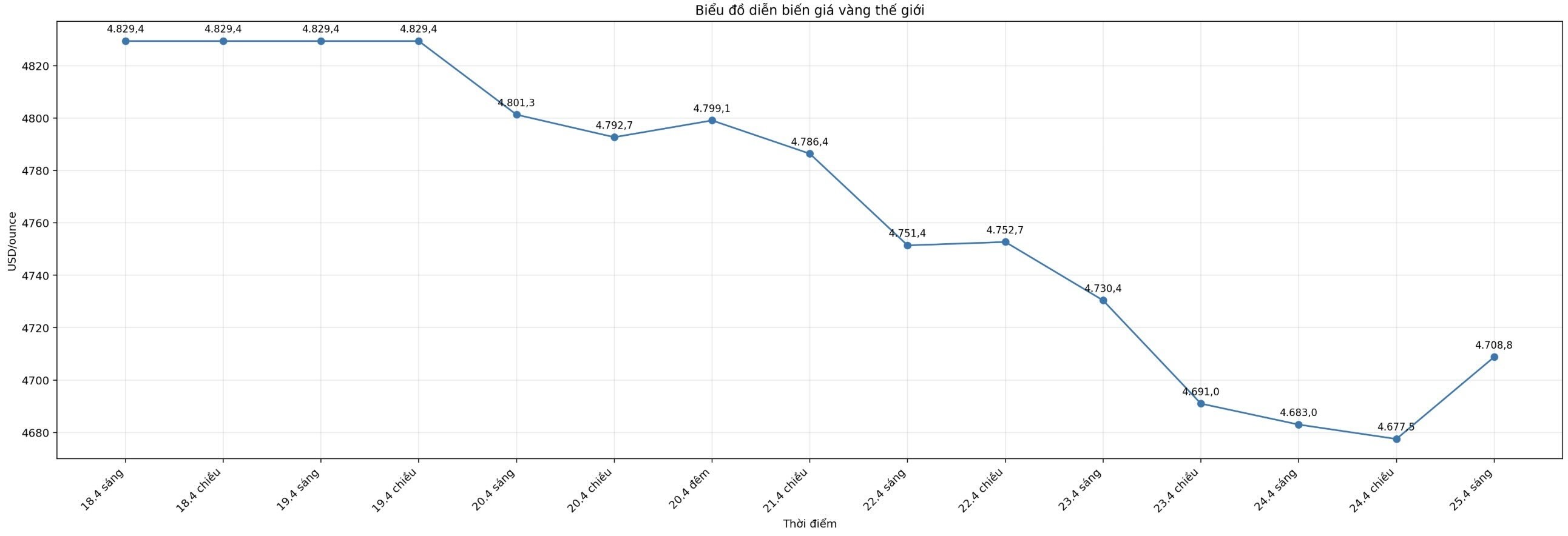

According to Kitco, gold trading volume has decreased in recent weeks, as prices fluctuate in a wide range from 4,600 to 4,900 USD/ounce. Although geopolitical tensions are still prolonged and economic concerns are high, the market has almost no urgent sentiment to promote short-term investment positions.

New concerns about inflation have increased interest rate expectations, thereby increasing the opportunity cost of holding gold and making strong buying difficult to convince.

However, it is also difficult for anyone to dare to bet on the downside and resist gold - the world's leading geopolitical neutral safe haven asset.

This feeling of boredom is not necessarily the problem, but reflects how the gold market is operating at the present time. Although price fluctuations are relatively limited, gold continues to play an anchor role in an increasingly stressful financial system. The current accumulation phase is not due to lack of interest, but to changes in the way gold is used and the group of gold buyers.

Recent initiatives by the London Bullion Market Association and the World Gold Council show continued efforts to classify gold into the High-Quality Liquidity Assets (HQLA) group. If recognized, gold will be in the same group as cash and government bonds in terms of approval in financial regulations.

Although this regulation has not been officially completed, central banks seem to be acting as if it had happened. The fact that the formal sector has continuously bought in in recent years shows growing concerns about traditional reserve assets.

Although gold has fallen compared to the record peak of January, the price remains at a historical high and global demand remains sustainable. Market commentary in recent months has increasingly focused on the growing gap between asset valuation and real risk, especially in stocks and government debt.

Geopolitical rifts continue to be an underestimated threat to global economic stability. In that context, gold is increasingly seen not only as a defensive tool against a specific economic scenario, but as an insurance against broader systemic tensions.

This fundamental demand is clearly reflected in the operations of central banks, especially the People's Bank of China. In March, when gold prices recorded the strongest monthly drop in decades, the central bank of China bought gold at the fastest pace in more than a year.

Price drops are being seen as buying opportunities, not warning signals. This explains why gold still maintains its historical high price range even when the upward momentum has slowed down.

Although short-term fluctuations sometimes disrupt the correlation of gold with other types of assets, gold still plays a role as a tool to diversify portfolios in the long term.

From a longer-term perspective, the fact that gold does not bring yields is not as disadvantageous as often seen in short-term interest rate cycles. Unlike most financial assets, gold does not bring partner risk - a characteristic that becomes more valuable during systemic instability.

The recent sideways phase, in itself, does not show the weakening core attractiveness of gold. On the contrary, the market seems to be absorbing high prices without creating significant selling pressure, suggesting that long-term holders still control the market. The return of gold to a quiet, sideways trading state may be reflecting stability rather than stagnation.