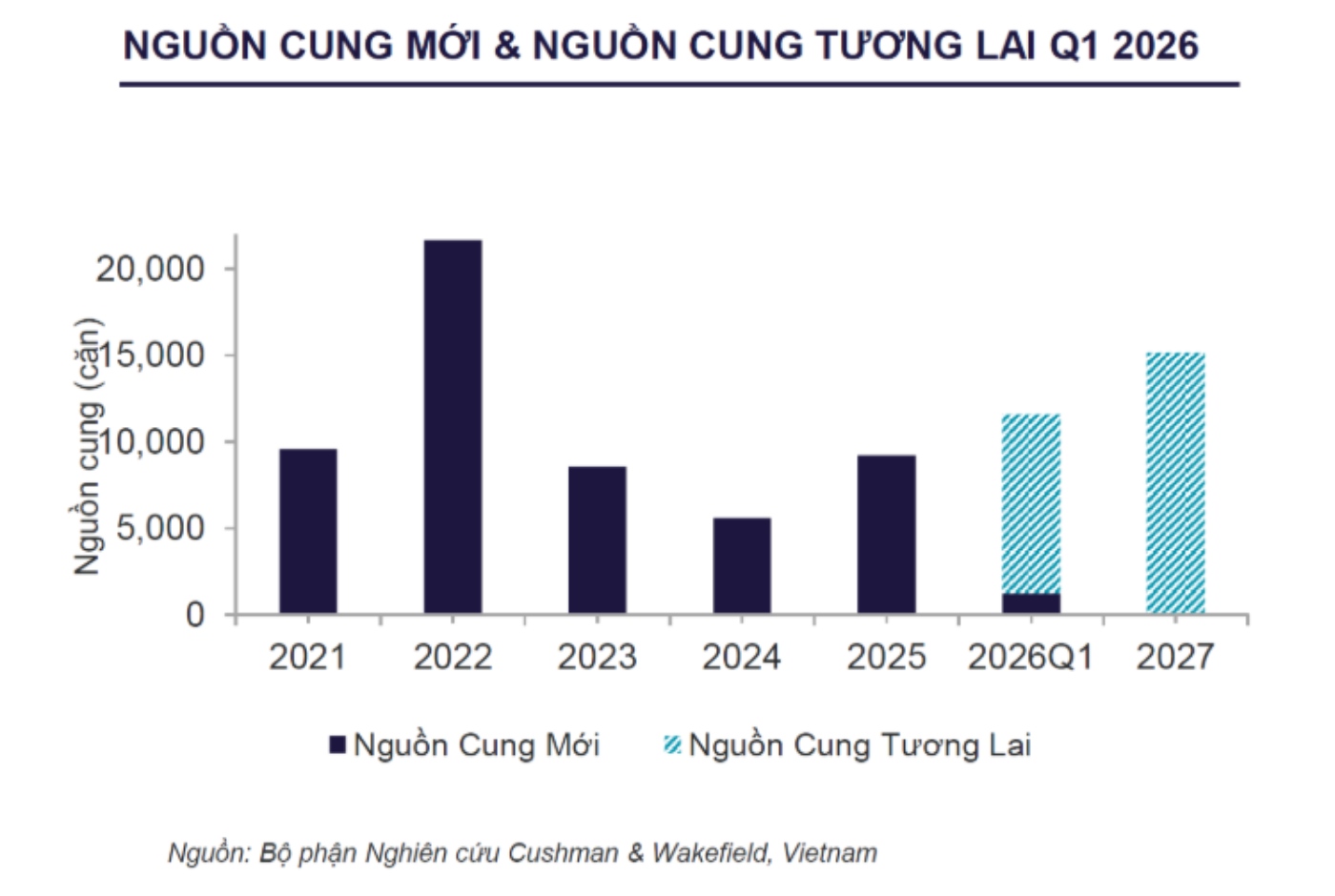

Cushman & Wakefield's overview report on the Ho Chi Minh City real estate market in Q1/2026 shows that the central area of Ho Chi Minh City recorded a sharp decrease in the supply of new apartments, with about 1,200 apartments offered for sale, down 62% compared to the previous quarter and down 47% compared to the same period last year. According to Cushman & Wakefield, this slowdown reflects the cautious, "waiting and observing" mentality of investors at the beginning of the year.

The East area continues to account for the largest proportion of new supply with about 80.3%, followed by the South area with about 19.7%. By segment, luxury apartments account for about 72% of new supply, while the high-end segment accounts for about the remaining 28%.

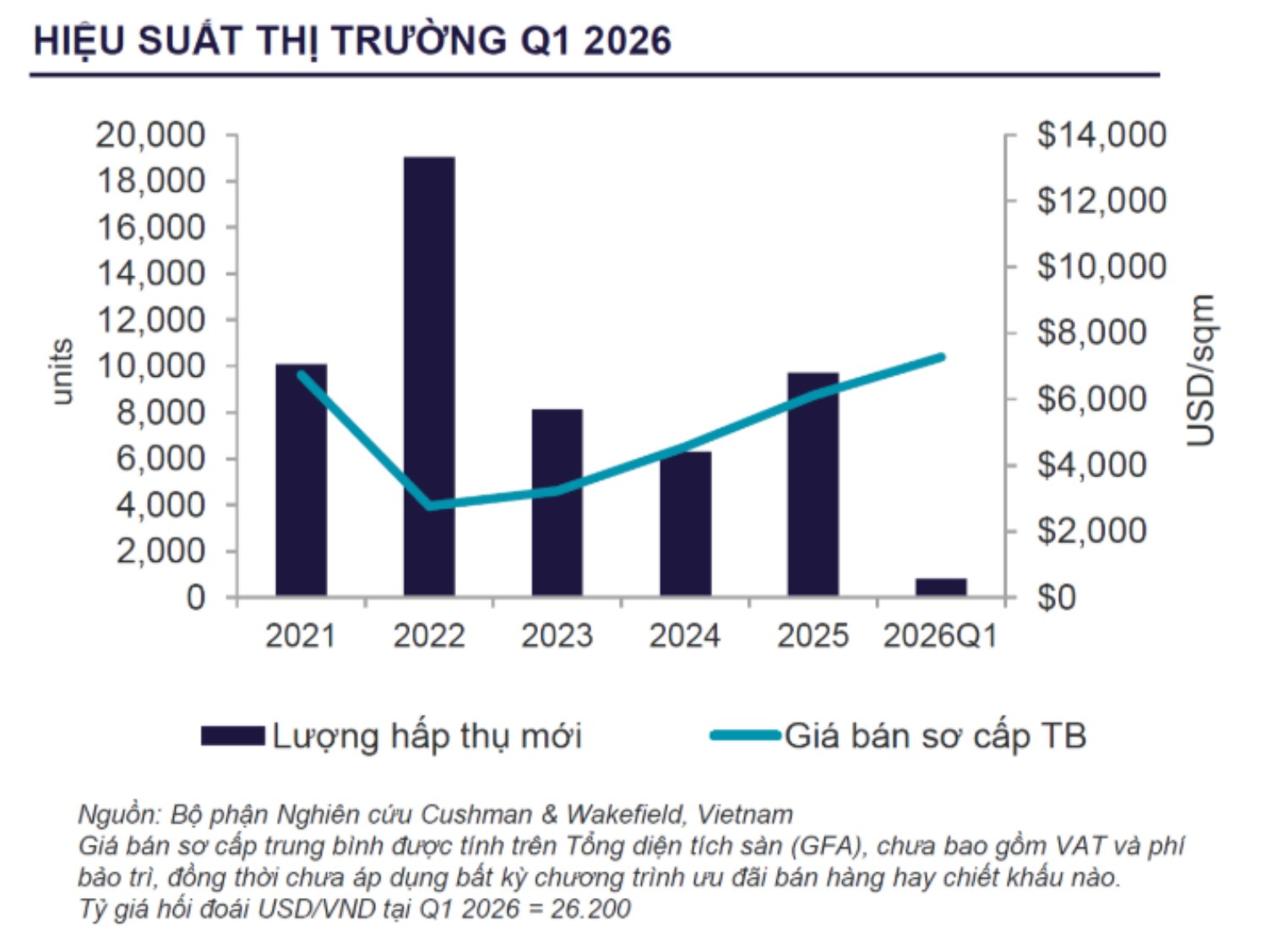

In Q1/2026, the market recorded new intake of less than 1,000 units, equivalent to about 25% of new supply, down 74% compared to the previous quarter and down 31% compared to the same period last year. According to Cushman & Wakefield, the combination of escalating primary prices and undiversified product structure, especially the lack of choices in the affordable and mid-range segments, has significantly reduced buyer sentiment compared to the growth momentum of 2025.

This trend shows a mismatch between the supply of the luxury segment and the actual demand of the mid-range market. In addition, credit tightening and increased borrowing costs are becoming major barriers, slowing down the absorption process when buyers have a cautious mentality, "waiting and observing" more favorable monetary policies in the coming quarters.

While new supply decreased to a low level, the average primary price has reached the highest level ever, nearly 7,300 USD/m2 (equivalent to 191.26 million VND/m2), an increase of about 19% compared to the previous quarter and an increase of about 53% compared to the same period last year. According to Cushman & Wakefield, this price level represents the base market price and does not include early booking incentives or quick payment discounts.

This unit believes that the average primary selling price in the central area of Ho Chi Minh City is expected to continue to be maintained at a high level due to increased input cost pressure and adjustments to increase real estate purchase loan interest rates. At the same time, capital flows from other areas, especially investors in the North, are pouring into the core area of Ho Chi Minh City with the expectation of price increases after a long period of shortage of new supply.

After the merger, the market is expected to continue to grow stably based on three factors including supply-demand balance, credit control and legal support. This opens a new cycle for the expanding Ho Chi Minh City apartment market.

According to Cushman & Wakefield, the new growth poles of Ho Chi Minh City, including Binh Duong province (old) and Ba Ria - Vung Tau (old), recorded more than 7,000 new apartments and more than 6,100 transactions, showing the increasing role of satellite areas in supporting housing needs.

Ms. Le Hoang Lan Nhu Ngoc - Senior Director, Head of Strategic Consulting Department of Cushman & Wakefield Vietnam - said that the Ho Chi Minh City apartment market is entering a more multi-polar growth phase. According to her, while the core area is still sought after and continues to maintain a high price level, pressure on affordability and limitations on product diversity are driving buyers to look for options further than the center.

This creates stronger momentum in satellite areas, where new supply, infrastructure connectivity and price levels are more suitable for current needs.

As the Ho Chi Minh City market gradually expands and takes shape, new growth poles will play a more strategic role in supporting housing demand and shaping the next growth cycle of the city's apartment market" - Ms. Le Hoang Lan Nhu Ngoc shared.