In a recent interview, Mr. Jerry Prior - Chief Operating Officer and Senior Portfolio Manager at KraneShares Mount Lucas Managed Futures Index Strategy ETF (NYSE: KMLM) - said that the factors driving the long-term upward trend of gold prices are still intact, especially the downward trend of countries depending on the USD as a key reserve asset.

Considering that gold prices have been revalued recently, I think this may be a pretty good entry point. The long-term dedollarization trend is structural and will continue" - Mr. Prior said.

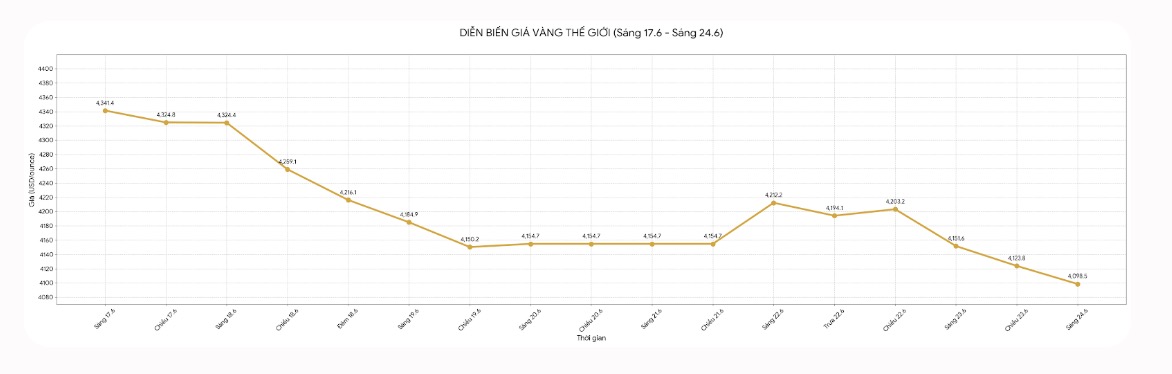

Recently, gold has been under strong selling pressure as traders react to tougher monetary policy views from US Federal Reserve (Fed) Chairman Kevin Warsh, and concerns about reduced tensions in the Middle East.

According to Mr. Prior, speculative investors, buying power from central banks and trending trading funds all contributed to the decrease in gold prices.

He believes that after the strong change in speculative positions in the market, most of the downward pressure has been reflected in prices.

Gold prices may fall below the 4,000 USD/ounce mark, but when oil supply begins to return, we will see central banks buy gold again to rebuild reserves," he said.

According to Mr. Prior, one of the most important changes in the gold market in recent years is that many countries want to diversify reserves and reduce holdings of assets valued in USD.

He believes that the US dollar being used as a tool of geopolitical pressure has become an important driving force for central banks to increase gold purchases and this trend is difficult to reverse.

“We believe that most of the gold's upward momentum is explained by this factor. Countries are looking for a value-saving asset outside the USD and US Treasury bonds. When oil production increases again and cash flow returns, we do not think capital will flow into the US Treasury bond market, but may return to gold,” Mr. Prior said.

Despite maintaining a positive view on gold, this expert warns that investors may continue to face fluctuations in the short term. Maintaining high interest rates and good inflation expectations may put pressure on the precious metal.

He also noted that gold does not always increase in price in a high inflation environment, especially when rising interest rates increase the opportunity cost of holding unprofitable assets.

However, he believes that investors should focus on long-term fundamental factors instead of short-term interest rate fluctuations.

Gold is a defensive asset in the investment portfolio. Retail cash flow once poured into gold has been somewhat relieved, so the risk of a panicked sell-off wave appearing at this time may be lower," he said.

Mr. Prior believes that the current macroeconomic context continues to support allocating a portion of the portfolio to gold. He predicts that inflation may remain higher than the pre-pandemic period as the trend of bringing production closer to the consumption market and restructuring the supply chain reverses the globalization process that has helped reduce price pressure for decades.

Before the pandemic, cheap goods from China contributed to curbing inflation in many developed economies. However, this momentum is changing, making it more unlikely that inflation will return to a stable low level as in the previous two decades.

In that context, Mr. Prior assessed that the recent correction of gold is not like the beginning of a prolonged downward cycle, but may just be a rebalancing phase in the long-term upward trend.

Looking towards the end of the year, he predicts gold prices may increase to about 4,500 USD/ounce as buying demand from central banks recovers and the trend of dedollarization continues to support capital inflows into precious metals.

I believe that the structural dedollarization trend, along with the increase in oil production in the Middle East, will bring buyers back to the market. Gold may continue to rise sharply from the current zone," Mr. Prior said.