According to Mr. Rodolphe Bohn - foreign exchange and commodity strategist at HSBC (one of the world's largest banking and financial services corporations), factors such as high geopolitical risks, increased fiscal deficits and persistent purchasing power from central banks will continue to support precious metals.

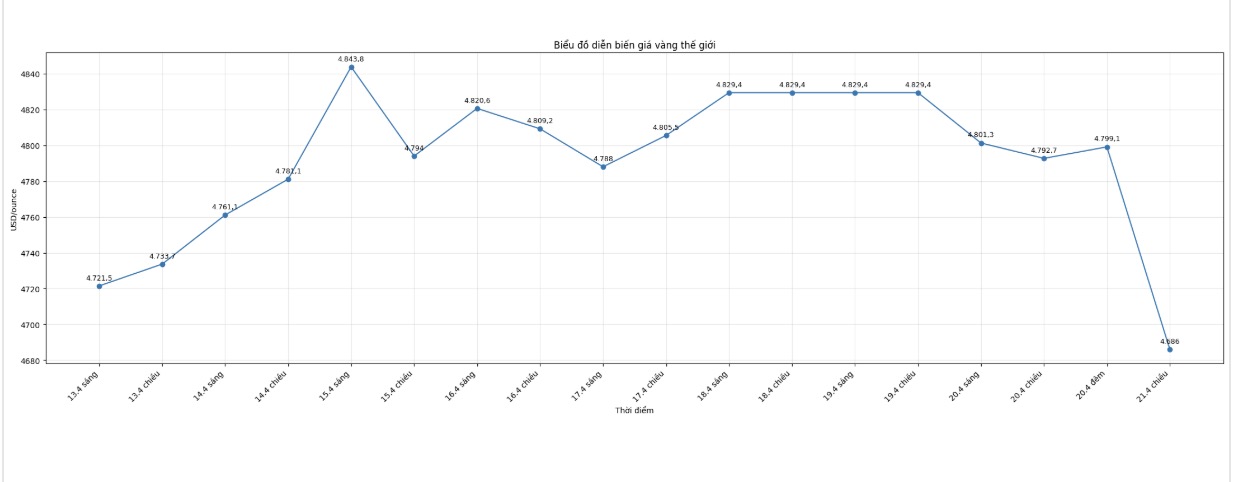

Mr. Bohn said that gold prices have experienced a period of strong fluctuations in the first months of 2026. From 544 USD/ounce at the end of January, gold prices fell to 4,400 USD/ounce on March 26, amid escalating tensions with Iran.

According to HSBC, in the period when the market avoided risks, oil prices rose sharply, the USD appreciated due to becoming a preferred safe-haven asset, bond yields rose, while stocks fell. At that time, gold did not clearly play its role as a "geopolitical barrier", because investors sold gold to increase liquidity, while most of the safe-haven demand flowed into the USD.

However, developments after the recent ceasefire show that gold prices may recover quickly as the market gradually stabilizes.

HSBC believes that the relationship between gold and oil prices is dynamic and can vary depending on the nature of the market shock. Before the conflict broke out, these two commodities tended to increase in the same direction. But then, the correlation quickly weakened as oil and gold prices went in two different directions.

Usually, when the USD appreciates, both gold and oil are under pressure. However, the supply shock from the Middle East pushed oil prices up, even when the USD's increase put pressure on gold. In the current context, a sharp increase in oil prices no longer means that gold prices will fluctuate according to the same scenario as before.

Regarding monetary policy, HSBC believes that this is still a key factor for gold trends. Although this bank does not expect the US Federal Reserve (Fed) to cut interest rates soon, high inflation and the risk of weakening growth will continue to support demand for gold.

Mr. Bohn said that high real yields are often a drag on gold because the precious metal does not generate profits. Since the conflict broke out, long-term yields have become more important as they simultaneously increase with the stronger USD, weakening stocks and rising oil prices.

Although HSBC still forecasts that the Fed will keep interest rates unchanged in the period 2026 - 2027, thereby potentially limiting gold's upward room, the risk of an inflationary trough is still a factor supporting the demand for holding this safe asset.

In addition, fiscal factors continue to strengthen the long-term outlook for gold. HSBC believes that budget deficits and rising public debt in the US as well as many other countries are boosting demand for hard assets, especially in the context of investors' concerns about financial stability and policy management space.

According to estimates by the International Monetary Fund (IMF), US public debt has approached 100% of GDP in 2025. Meanwhile, increased defense spending globally is also adding to the debt burden. HSBC believes these trends are unlikely to reverse in the medium term, thereby continuing to create support for gold prices.

Regarding buying power from central banks, HSBC said demand has cooled down compared to the peak period of 2022 - 2024. Some central banks have even sold gold to preserve foreign exchange reserves amid rising energy import bills and defense spending.

However, HSBC expects gold buying demand from the central banking sector to improve again by the end of the year, when the long-term foreign exchange reserve diversification strategy is reaffirmed.

Not only investment demand, high gold prices are also changing the physical supply and demand balance in the market.

In the short term, HSBC believes that the direction of gold prices will largely depend on the degree of real cooling of tensions in the Middle East. A sustainably maintained ceasefire or moving towards a complete end to the conflict, along with the official reopening of the Strait of Hormuz and stable oil prices at a lower level, will help reduce financial pressure, ease inflationary concerns and pull yields down.

In that context, HSBC still maintains an optimistic view on gold prices in the medium and long term.