According to Cushman & Wakefield Vietnam's 10-year review of the Vietnamese real estate market report, the Southern industrial real estate segment is entering a more strategic growth phase.

After a decade driven by a strong expansion of supply, rising land prices and sustainable development of production activities, the region has passed a pure growth cycle in scale, and is now increasingly oriented towards "quality", shaped by infrastructure upgrades, supply chain restructuring, product completion and greater focus on operational efficiency.

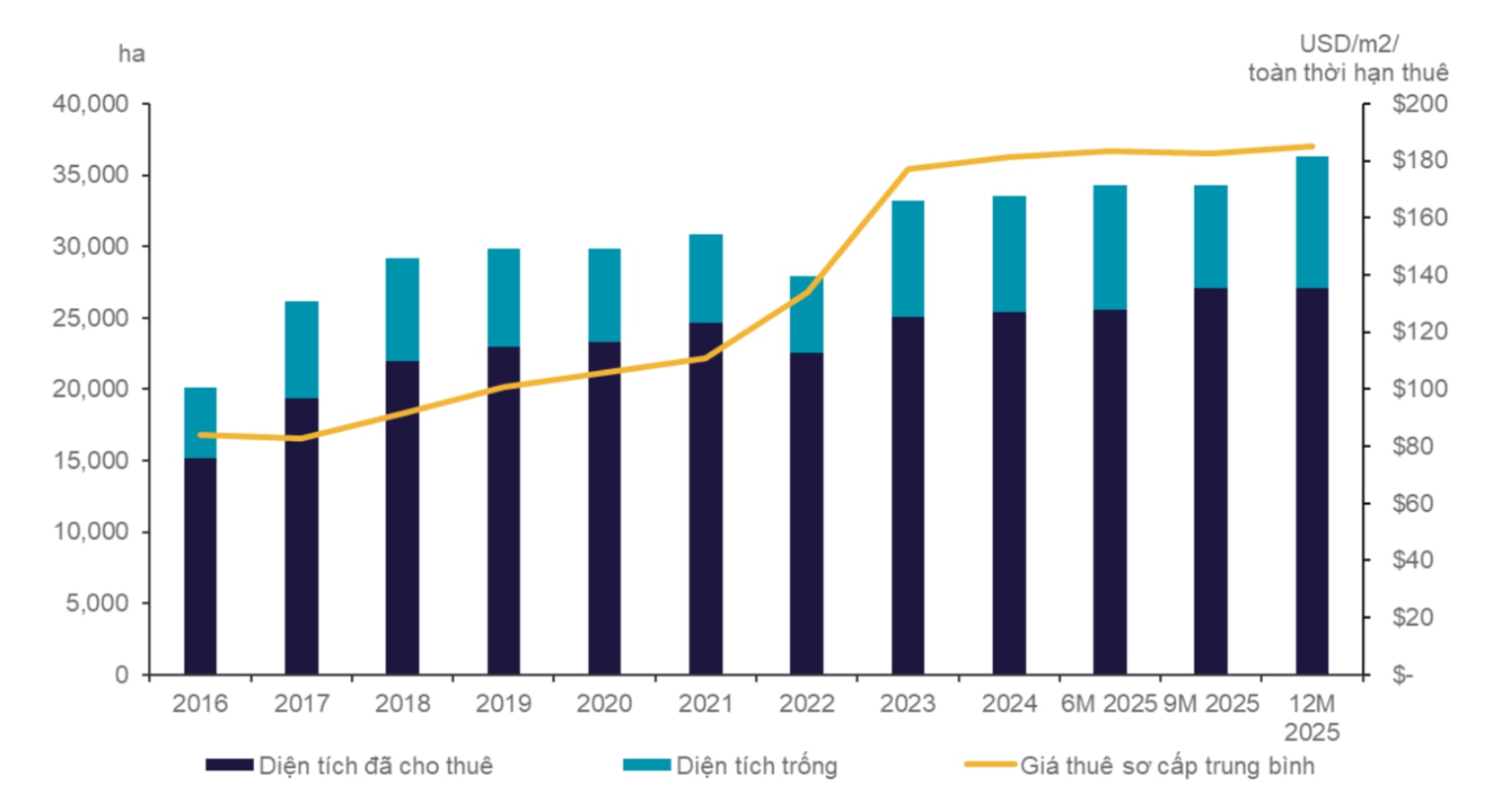

In the past 10 years, the industrial park land market in the South recorded a total supply increase of 80.21%, while the average primary price increased by 120.5%, equivalent to a compound annual growth rate (CAGR) of 9.18% in this period. In the ready-built asset segment, ready-built warehouses (RBW) recorded a total supply increase of 141% in the reviewed period, while rental prices increased by 43.8%, equivalent to CAGR 5.3%. Ready-built factories (RBF) recorded a supply increase of 134%, with rental prices increasing by 16.7%, equivalent to CAGR 2.2%.

Analysis shows that the market has shifted from a "strong expansion" phase to a "adjustment to increase value" phase, reflecting an increasing focus on modern standards, operating efficiency, sustainability factors and higher quality solutions for tenants.

This shift is supported by Vietnam's solid production platform, increasingly expanding trade connections and Vietnam's continuous attractiveness as a production base for international investors. These structural drivers have maintained demand for industrial land and ready-made products throughout the South, especially as tenants increasingly prioritize the resilience of the supply chain, operational efficiency and strategic location choices.

In the South, that demand has promoted the formation of deeper industrial clusters and a clearer regional growth structure. Within the Southern Key Economic Region (according to Cushman & Wakefield's definition, including Ho Chi Minh City, Tay Ninh and Dong Nai), the total industrial park land supply currently reaches 36,400 ha at 161 projects. This area currently also has about 6.60 million m2 of pre-built factory area (RBF) at 205 projects and 6.65 million m2 of pre-built warehouse area (RBW) at 189 projects.

By 2036, the supply of industrial park land in the region is expected to increase to at least 58,557 ha at about 250 projects, while the total RBF supply is expected to reach 7.76 million m2 and the total RBW supply is expected to increase to 7.31 million m2. This future supply continues to consolidate the region's role as one of the key corridors for production, logistics and industrial investment of Vietnam, while showing that future growth will increasingly be shaped by quality, location strategy and level of integration with wider supply chains.

Ms. Chuong Quoc Doan - Deputy Director of Industrial and Office Leasing Consulting Department, Cushman & Wakefield Vietnam - said: "The Southern industrial market has grown strongly over the past decade, but it is clear that the focus of the next phase will shift from quantity to quality. A more strategic phase, where infrastructure connectivity, product quality, operational efficiency and sustainability will play a greater role in creating long-term value. For both investors and tenants, this is becoming a market with deeper specialization and differentiated competitiveness.

Ms. Doan added that the Southern key economic region continues to be supported by deep production platforms, a formed logistics network and strong future supply. At the same time, tenants' expectations are also increasing. The increasing demand is directed towards better-planned industrial assets, more modern pre-built asset models, and locations that can support both production efficiency and supply chain resilience.