From March 5, business households and individual businesses must notify the tax authority when changes related to the business location arise, according to the provisions of Circular 18/2026/TT-BTC issued by the Ministry of Finance.

This Circular stipulates the dossiers, order and procedures for tax management for business households and individual businesses. One of the notable contents is the requirement that taxpayers must promptly notify the directly managing tax authority when there are changes in business locations.

Cases that must be notified

According to new regulations, taxpayers must send a notice to the directly managing tax authority when one of the following cases arises:

- Open new business locations

- Change information related to business location

- Temporarily suspend operations at the registered location

- Terminating operations at business locations

This regulation applies to both business households and individual businesses, even in cases of expanding the scale or changing the form of operation.

According to Decree 68/2026/ND-CP, notifications must be made within 10 working days from the time of change. After receiving them, the tax authority will respond so that taxpayers can complete the procedures according to regulations.

The tax rate is applied differently depending on the business sector. Specifically, the distribution and supply of goods is taxed at 0.5% on revenue. Services or non-contracting construction activities apply a tax rate of 2%. For some specific sectors such as asset leasing, insurance agents, lottery agents or multi-level marketing, the tax rate applied is 5%.

Meanwhile, production, transportation or services related to goods and construction with raw material contracts are taxed at 1.5%. For digital content services such as electronic games, digital movies, digital music or digital advertising, a tax rate of 5% is applied. Other types of business that do not fall into the above groups will apply a tax rate of 1%.

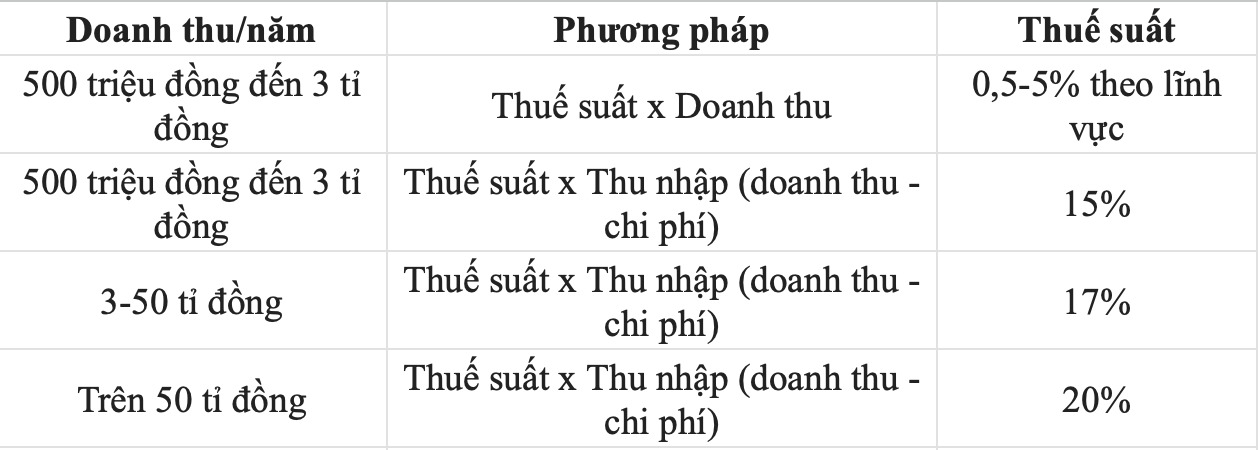

In addition to the tax calculation method based on the percentage of revenue, business individuals can also apply the income-based calculation method. Accordingly:

Personal income tax = Tax rate x Taxable income.

(Taxable income is the remainder after taking revenue minus expenses for business operations)

This method is mandatory for individuals with revenue over 3 billion VND per year. In which, if revenue is over 3 billion VND to 50 billion VND, a tax rate of 17% will be applied. If revenue exceeds 50 billion VND per year, the tax rate applied is 20%.

For individual businesses with revenue from over 500 million VND to 3 billion VND per year, the income tax calculation formula can also be applied. At that time, the general tax rate is 15% and does not distinguish by business sector.

The Decree also stipulates that business individuals must maintain a stable tax calculation method for at least two consecutive years from the first year of application. In case an individual is paying tax according to the revenue-to-revenue ratio method but the actual revenue in the year exceeds 3 billion VND, from the following year, they must switch to the income-based tax calculation method.

In parallel with that, business households and individual businesses with value-added tax revenue of 1 billion VND or more per year must use electronic invoices with codes from tax authorities or electronic invoices generated from cash registers with data connections with tax authorities as prescribed.