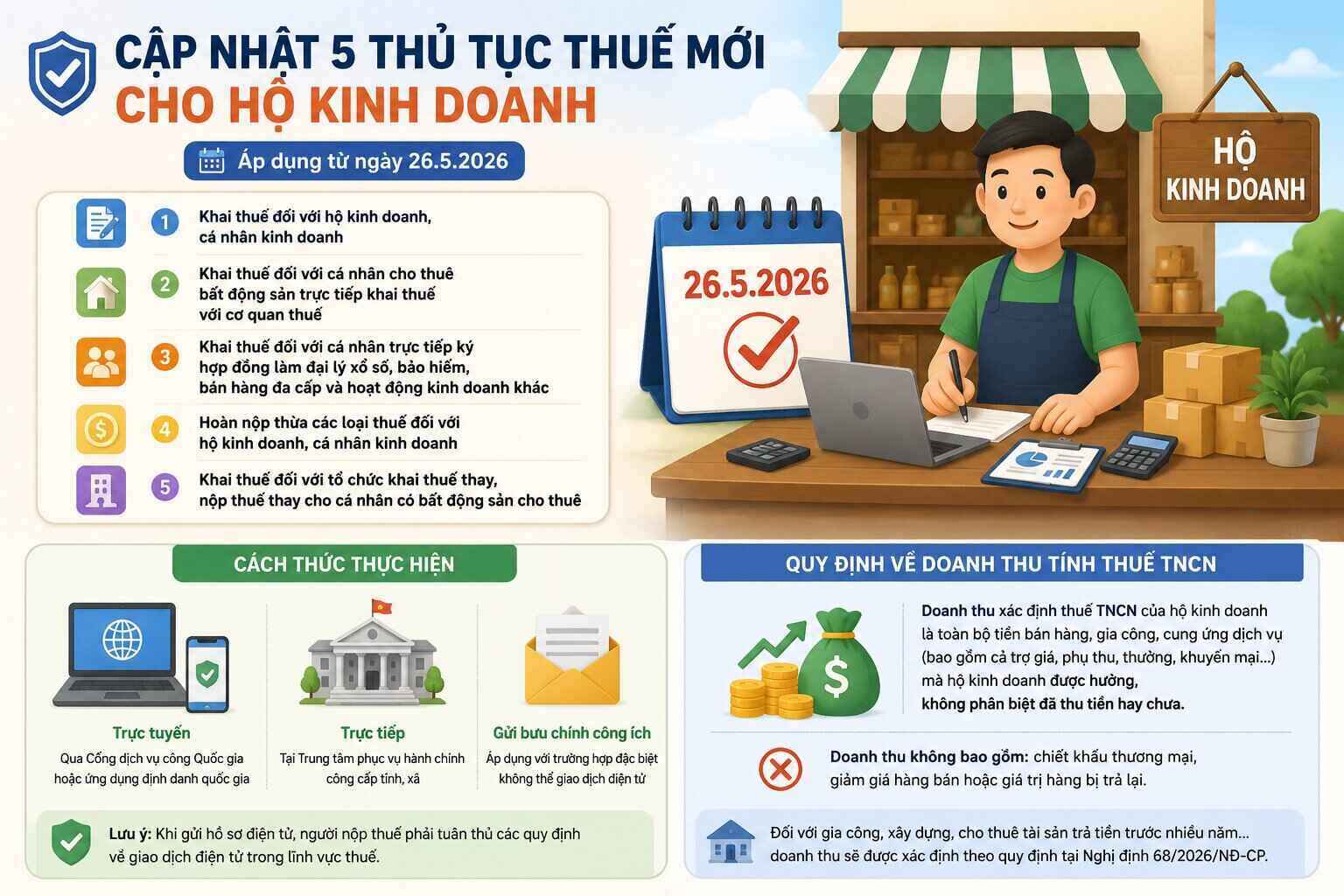

5 amended tax procedures from May 26, 2026

According to Decision 1272/QD-BTC, administrative procedures in the field of tax management that are amended and supplemented include:

- Tax declaration for business households and individual businesses.

- Tax declaration for individuals leasing real estate who directly declare taxes with tax authorities.

- Tax declaration for individuals directly signing contracts to act as lottery agents, insurance, multi-level marketing and other business activities.

- Overpaid tax refunds for business households and individual businesses.

- Tax declaration for organizations that declare taxes on behalf of, pay taxes on behalf of individuals with real estate for lease.

New points in tax declaration procedures for business households

From May 26, 2026, depending on the subject and method of tax payment, business households need to declare according to form No. 01/TKN-CNKD or 01/CNKD issued together with Circular 50/2026/TT-BTC.

How to do it:

Via the National Public Service Portal or the national identification application.

At provincial and commune-level public administrative service centers or send via public postal services (applied to special cases where electronic transactions cannot be carried out).

Important note: When submitting electronic dossiers, taxpayers must strictly comply with the regulations in Circular 19/2021/TT-BTC and Circular 46/2024/TT-BTC on electronic transactions in the tax sector.

Regulations on revenue for personal income tax (PIT) calculation

According to Article 5 of Decree 68/2026/ND-CP, the revenue determined for personal income tax of business households is the entire amount of money from sales, processing, and service provision (including subsidies, surcharges, bonuses, promotions... ) that business households enjoy, regardless of whether money has been collected or not.

Specific notes: Revenue does not include commercial discounts, discounts on goods sold or the value of returned goods. For activities such as processing, construction, or leasing assets with prepayment for many years, revenue will be determined according to specific regulations in Decree 68/2026/ND-CP.