On March 4, 2026, the Tax Department updated guidance document No. 1296/CT-NVT on personal income tax finalization for income from salaries and wages.

Change in family deduction level

For the 2025 finalization period, the family circumstance deduction level is determined according to the provisions of Resolution No. 95/2020/UBTVQH14 dated June 2, 2020 of the National Assembly Standing Committee, specifically as follows:

The deduction level for taxpayers is 11 million VND/month (132 million VND/year).

The deduction for each dependent is 4.4 million VND/month.

From the tax period of 2026 (from January 1, 2026), the family circumstance deduction level is adjusted according to Resolution No. 110/2025/UBTVQH15 of the National Assembly Standing Committee, replacing the current regulations in Resolution No. 95/2020/UBTVQH14. Accordingly, the new family circumstance deduction level is regulated as follows:

The deduction level for taxpayers is 15.5 million VND/month, equivalent to 186 million VND/year.

The deduction for each dependent is 6.2 million VND/month.

This adjustment of the family deduction level takes effect from January 1, 2026 and is applied to the 2026 tax period, helping to increase the minimum taxable income threshold and reduce tax obligations of taxpayers in the context of increasing living expenses and average income.

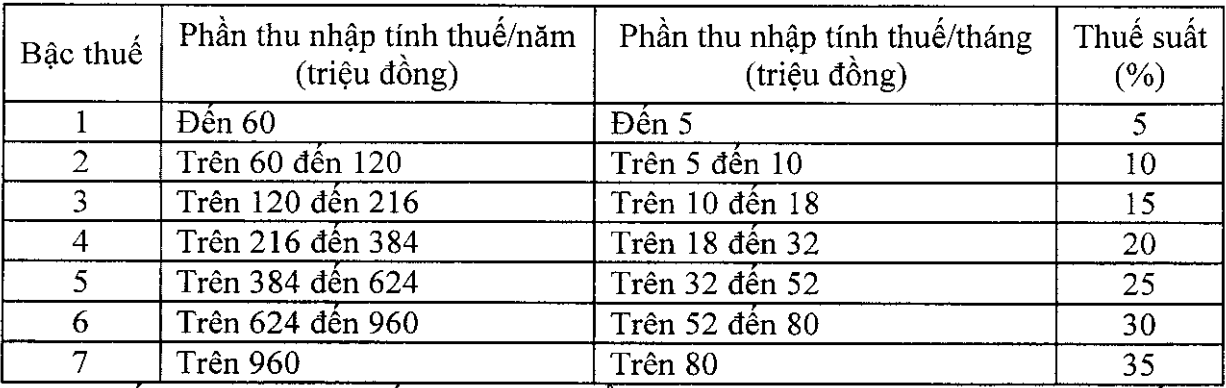

New progressive tax schedule

For the 2025 finalization period, according to the Personal Income Tax Law No. 04/2007/QH12, income from salaries and wages of resident individuals applies a progressive tax schedule including 07 tax brackets as follows:

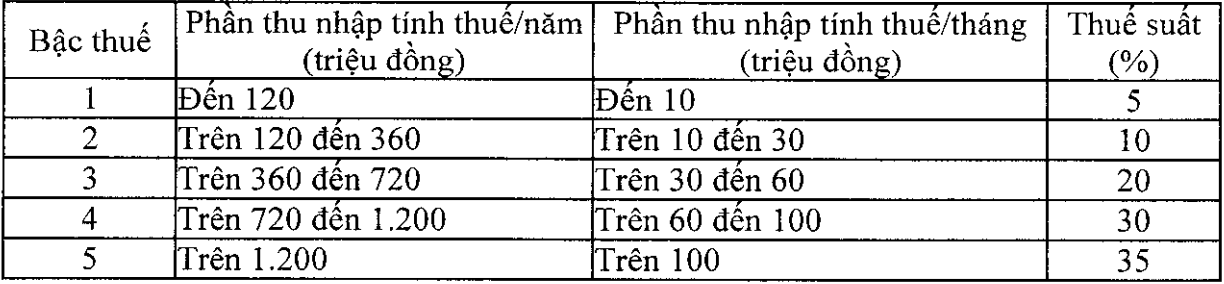

For the tax period of 2026, from January 1, 2026, according to the Law on Personal Income Tax No. 109/2025/QH15, income from salaries and wages of resident individuals applies a progressive tax schedule including 05 tax brackets:

Tax finalization guidelines for employees

Taxpayers need to proactively review the actual situation arising in the year to determine whether they are subject to direct finalization, authorization of finalization or not to finalize according to regulations. Accordingly, cases that must finalize PIT include:

Organizations and individuals paying income from salaries and wages:

- Organizations and individuals paying income from salaries and wages are responsible for declaring and finalizing PIT regardless of whether tax deductions arise or not, and finalizing PIT on behalf of authorized individuals.

- In case organizations and individuals paying income are dissolved, bankrupt, terminate operations, terminate contracts or reorganize enterprises, they must declare personal income tax finalization at the time of dissolution, bankruptcy, termination of operations, termination of contracts or reorganizing enterprises.

Individuals with income from salaries and wages:

- Individuals with residence having income from salaries and wages from two or more places that do not meet the conditions for authorizing finalization according to regulations must directly declare personal income tax finalization with the tax authority where the individual has additional income to be paid or the tax authority pays more or is deducted in the next tax declaration period.

- Individuals present in Vietnam counted in the calendar year is less than 183 days, but counted in 12 consecutive months from the date of first presence in Vietnam is 183 days or more, then the first year of settlement is 12 consecutive months from the date of first presence in Vietnam.

- Individuals who are foreigners ending their working contracts in Vietnam declare tax finalization with tax authorities before leaving the country. In case individuals have not completed tax finalization procedures with tax authorities, they shall authorize income-paying organizations or other organizations and individuals to finalize taxes according to regulations and finalize taxes for individuals. In case income-paying organizations or other organizations and individuals receive authorization to finalize, they must be responsible for the amount of PIT to be paid additionally or for the refund of the surpaid tax of individuals.

- Individuals residing with income from salaries and wages residing abroad and individual residents with income from salaries and wages residing in international organizations, embassies, consulates who have not deducted tax in the year, the individual must finalize directly with the tax authority, if there is an additional tax payable or a surplus tax payable or it is deducted in the next tax declaration period.

- Resident individuals who have income from salaries and wages and are actually eligible for tax deductions due to natural disasters, fires, accidents, and serious illnesses affecting their ability to pay taxes, do not authorize organizations or individuals to pay income for tax finalization on their behalf but must directly declare tax finalization with the tax authority according to regulations.