The fact that bank employees at Vietcombank (VCB) or MB secretly offer interest rates up to 8 - 8.45%/year - completely contrary to the public listings (as Lao Dong Newspaper has reflected) - is not a coincidence.

Separating the Q1/2026 financial statements (BCTC) of these two banks, it can be seen that the capital thirst is very clear. Behind the surface of the profit figure is a serious mismatch between mobilization and lending, pushing cost of goods sold to thousands of billions of VND.

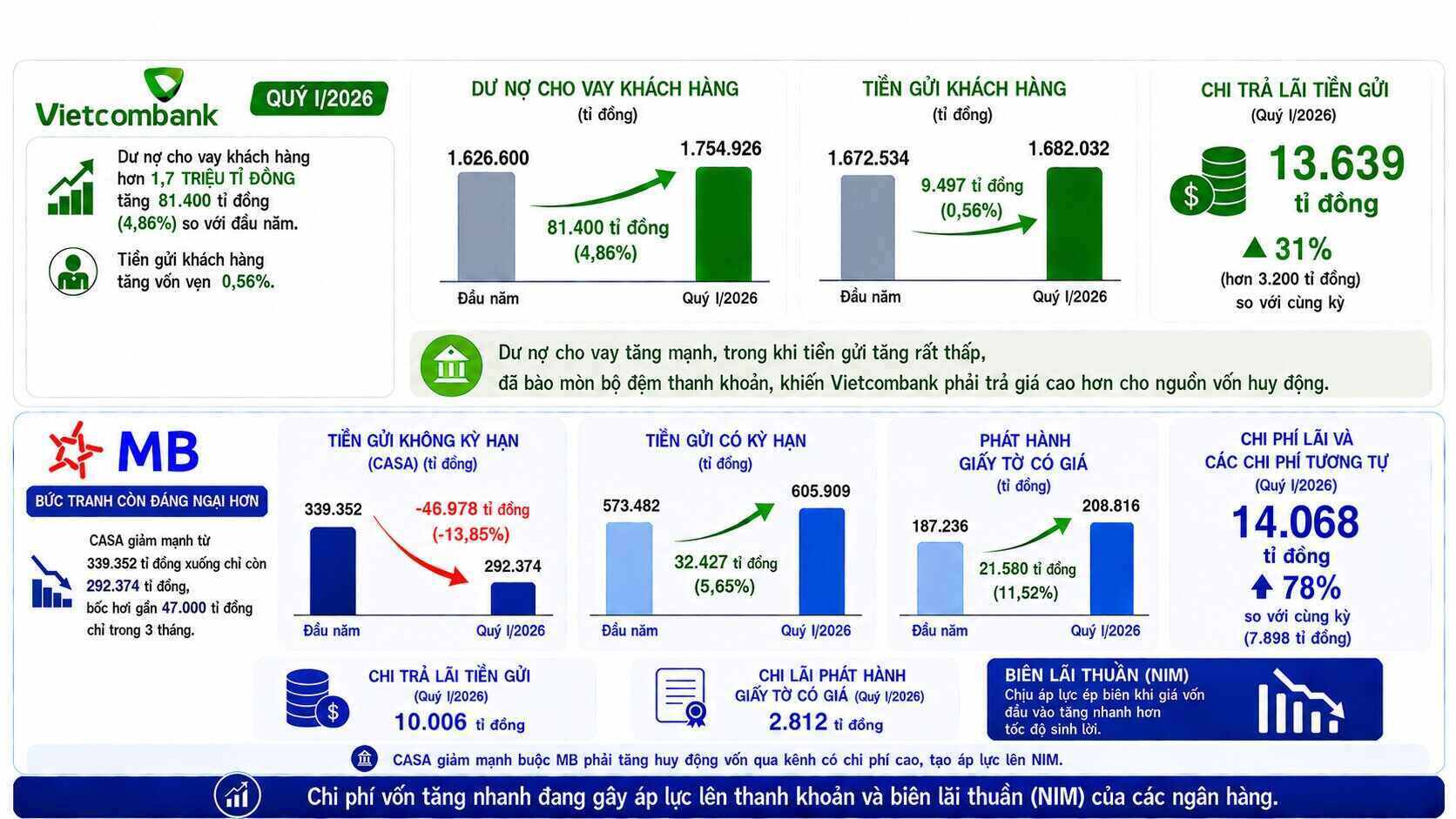

Output "tense", input "miss".

At Vietcombank, in the first quarter of 2026, outstanding loans to customers reached more than 1.7 million billion VND, a sharp increase of nearly 81,400 billion VND (+4.86%) compared to the beginning of the year. Meanwhile, customer deposits only reached 1,682,032 billion VND, an increase of only 9,497 billion VND. Thus, for every 1 VND of new deposit mobilized from customers, the bank had to disburse up to 8.5 VND into the economy.

The demand for disbursement is 8.5 times higher than the net mobilized cash flow from residential customers and economic organizations, which has significantly eroded the core liquidity buffer of the bank. To keep cash flow from flowing to other channels, the inevitable consequence is that Vietcombank has to pay a more expensive price.

Accordingly, in the first quarter, this bank had to spend up to 13,639 billion VND to pay deposit interest, an increase of more than 31% (more than 3,200 billion VND) compared to the same period.

At MB, the financial picture shows even more concerns. Non-term deposits (CASA) have decreased sharply from 339,352 billion VND to only 292,374 billion VND, evaporating nearly 47,000 billion VND in just 3 months. To compensate for the cash flow gap to finance credit activities, MB was forced to pivot to higher-cost mobilization channels.

Term deposits increased sharply from 573,482 billion VND to 605,909 billion VND. In parallel, the volume of issuing valuable papers also increased sharply from 187,236 billion VND to 208,816 billion VND.

The consequences of buying capital at high prices immediately reflected in the cost structure. Profit expenses and similar expenses jumped to 14,068 billion VND, an increase of more than 78% compared to the figure of 7,898 billion VND in the same period.

Meanwhile, interest income increased by about 48%, reaching 28,982 billion VND, but deposit interest payment alone consumed 10,006 billion VND, and interest payment for issuing valuable papers cost an additional 2,812 billion VND. In summary, the net interest income of this bank is only 14,913 billion VND. The net interest margin (NIM) is clearly under great pressure to squeeze the margin when the input cost is inflated faster than the rate of return of output assets.

Liquidity pit and risks from real estate

At MB, the shortage of mobilized cash flow combined with credit growth is creating a fairly large term risk gap. Net cash flow from business activities is heavily negative, up to 64,971 billion VND, far less than the negative level of 26,075 billion VND in the same period last year.

Notably, in the liquidity risk section, in the "Until 1 month" period, MB is recording a negative net liquidity difference of up to 112,617 billion VND. This means that the amount of liabilities to be paid in the next month is far exceeding the amount of assets that can be converted into cash in the same term.

Accordingly, the amount of money and cash equivalents at the end of the term of MB has sharply decreased from VND 229,259 billion at the beginning of the year to only VND 169,985 billion at the end of the first quarter.

Notably, in a time of capital shortage, MB's real estate business balance still skyrocketed to 131,895 billion VND (accounting for 11.77% of total outstanding balance).

With Vietcombank, to compensate for the shortfall of local capital, this bank must strongly depend on deposits from the State Treasury and interbank loans.

Accordingly, government and State Bank debts (mainly payment deposits from the State Treasury) surged from 160,128 billion VND to 198,629 billion VND (+24%).

Deposits and loans from other credit institutions increased from 321,158 billion VND to 367,184 billion VND (+14.3%).

Issuance of valuable papers also increased from 27,101 billion VND to 29,094 billion VND to raise long-term capital.

Grid areas" in asset quality

Not only is the cash flow tense, but the asset quality of both banks also shows signs. At Vietcombank, although bad debts are officially controlled, in just the first 3 months of the year, Group 2 debt (debt to be noted) has jumped from 2,704 billion VND to 4,040 billion VND, equivalent to an increase of nearly 50%.

At MB, the debt group jumping rate is also quite fast. Total bad debt (Group 3 to Group 5) increased from VND 14,027 billion at the beginning of the year to nearly VND 15,948 billion. The bad debt ratio (NPL) increased slightly from 1.29% to about 1.42%.

Worryingly, substandard debt (Group 3) increased sharply by more than 33.7% (reaching more than 4,382 billion VND). Potentially irrecoverable debt (Group 5) also increased by more than 15% to more than 7,406 billion VND.

Debt to be noted (Group 2) also increased by nearly 16%, reaching more than 11,837 billion VND. This is a very large risk buffer zone that can be converted into bad debt in the following quarters.