According to Clause 4, Article 13 of Decree 68/2026/ND-CP, from March 5, 2026, business households and individual businesses must notify the tax authority of the entire number of bank accounts and e-wallets related to production and business activities by electronic means.

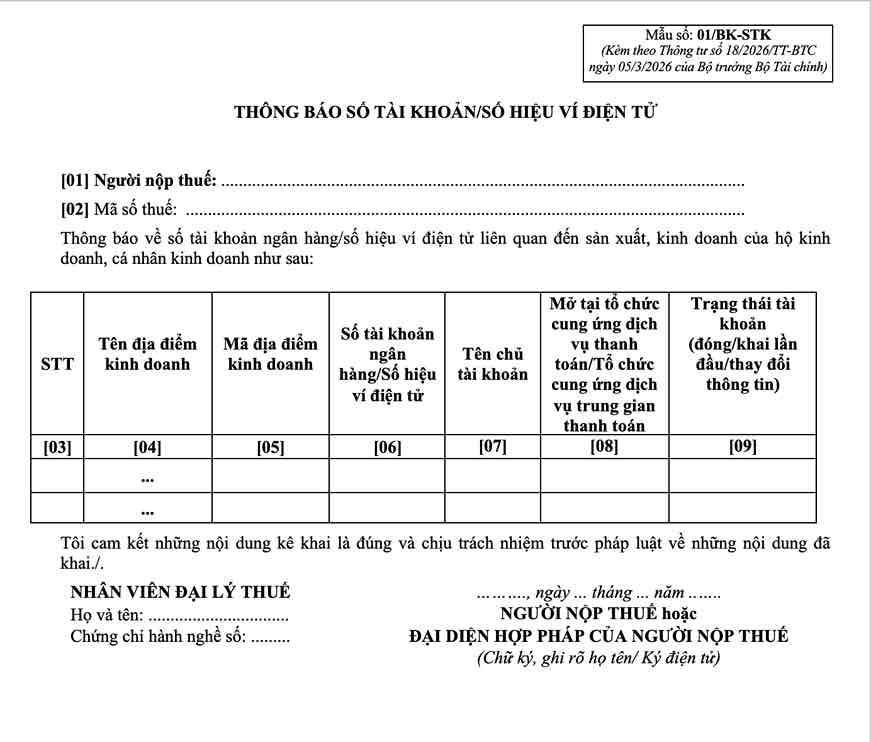

The notification is implemented according to Form No. 01/BK-STK issued with Circular 18/2026/TT-BTC.

For business households with revenue over 500 million VND/year, this form is sent together with the first tax return of the year according to the guidance in Circular 18/2026/TT-BTC.

This regulation aims to standardize business cash flow data in the context of tax authorities shifting to management based on actual revenue instead of the previous khoán method.

Cases where bank account notifications must be sent

According to the guidance in Article 4 of Circular 18/2026/TT-BTC, business households must notify bank accounts in the following cases:

- Business households operating with revenue over 500 million VND send a notice according to Form 01/BK-STK with the first tax return of the year;

- New business households starting business send this form with a revenue notice or first-time tax declaration dossier;

- In case of changing the account number or changing the e-wallet used in business, it must be notified to the tax authority according to regulations.

In addition, the tax authority requires business households to notify all accounts used to receive sales money, regardless of whether they are opened at banks or intermediary payment organizations.

Not notifying an account may entail tax procedure risks

According to the provisions of Decree 68/2026/ND-CP, the notification of a bank account is part of the taxpayer's obligation to provide information to serve revenue data management.

In case business households do not notify or not fully notify account information related to business activities, the tax authority may request supplementation of dossiers or conduct data review to determine tax obligations in accordance with tax management laws.

The implementation of notifications in the correct form and at the right time is therefore an important step to help business households ensure the consistency of declaration data, limiting the occurrence of obstacles when fulfilling tax obligations under the new management mechanism.