From January 1, 2026, Clause 6, Article 10 of Resolution 198/2025/QH15 has specifically stipulated that business households and individuals do not apply the tax contract method. Business households and individuals pay taxes according to the law on tax management.

At the same time, in Section 2.2 Section 2, Part I, Article 1 of the Project attached to Decision 3389/QD-BTC in 2025, the Ministry of Finance guides: From January 1, 2026, business households will officially switch from the contract tax method to the method of self-declaration and tax payment.

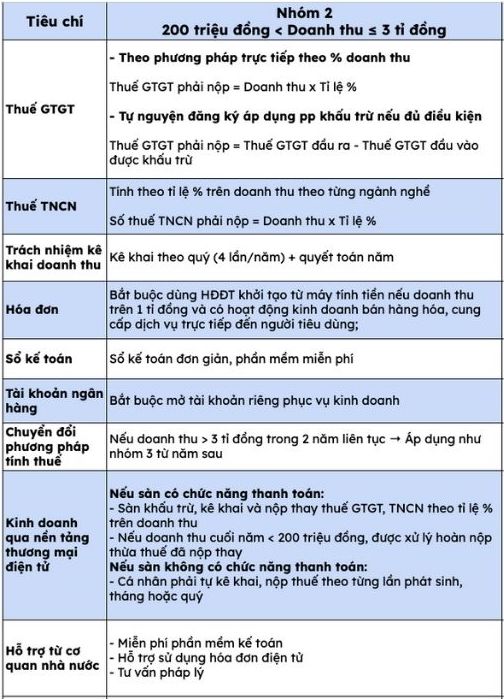

In Table 2, tax management models for households and individuals are classified and instructions on how to calculate tax on business households in 2026 in detail when removing contract tax to declare and pay taxes on self for 3 groups of business households.

For business households with a revenue of VND 200 million or more and under VND 3 billion in group 2, value added tax (VAT) will be paid as follows:

According to the direct method on % of revenue

VAT payable = Revenue x %

Voluntarily register to apply the deduction method if eligible

VAT payable = Output VAT - Input VAT deductible

With personal income tax (PIT) collection calculated as a percentage of revenue for each industry:

Number of personal income tax payable = Revenue x %

Business households and individuals are responsible for quarterly declaration (4 times/year) and annual settlement.

If the revenue is over 1 billion VND, businesses are required to use electronic invoices generated from cash registers and conduct business in selling goods and providing services directly to consumers. Simple accounting book and free simple software support.

In addition, business households are required to open their own accounts for business. In case, revenue over 3 billion VND for 2 consecutive years will be applied as group 3 from the following year.

Notably, households and individuals doing business through e-commerce platforms need to pay attention to the following 2 cases:

If the exchange has the function of payment: The exchange deducts, declares and pays VAT and personal income tax in percentage of revenue. If the year-end revenue is below VND 200 million, the business household will be processed to refund the excess tax paid on behalf of the business.

If the exchange does not have the function of payment: Individuals must self-declare and pay taxes for each arising, month or quarter.

In particular, state agencies will provide free accounting software, support businesses to use electronic invoices and provide legal advice.