According to Mr. Doug Moglia - macro and market strategist at Rockefeller Global Investment Management, silver prices continue to benefit from the upward cycle of the precious metal group, but the potential for tactical increase has become more limited.

Mr. Moglia said that as speculation accelerated last year, the upward momentum of precious metals has spread to higher beta-coefficient metals such as silver and platinum.

This is a common development in upward price cycles, when cash flow first turns to assets directly linked to macroeconomic changes such as gold, and then rotates to assets with the ability to amplify higher profits.

However, expert Rockefeller noted that silver should be seen as a more volatile version of gold. Historically, silver has often been called "gold with higher beta" due to its high volatility, thinner liquidity and influence from many different factors.

More than 50% of silver demand comes from the industrial sector, while gold is mainly driven by investment, central banking and jewelry demand.

According to Doug Moglia, silver has fallen into structural deficit since 2021, due to demand from green energy such as solar panels, electric vehicles and AI-related applications such as semiconductors, grids. However, the non-automatic supply shortage has caused silver prices to rise sharply.

The reason is that although silver has a large proportion of industrial use, this metal is still often traded as a currency along with gold. Therefore, silver prices are greatly influenced by market sentiment, monetary policy, currency fluctuations and increased investment capital flows.

Mr. Moglia also said that the supply response of silver is quite special. About 70% of silver production is a byproduct in the process of mining other metals, so the supply does not increase significantly even when silver prices rise.

This helps the basic foundation of silver to remain positive, but short-term developments are currently more influenced by cash flow and market inertia.

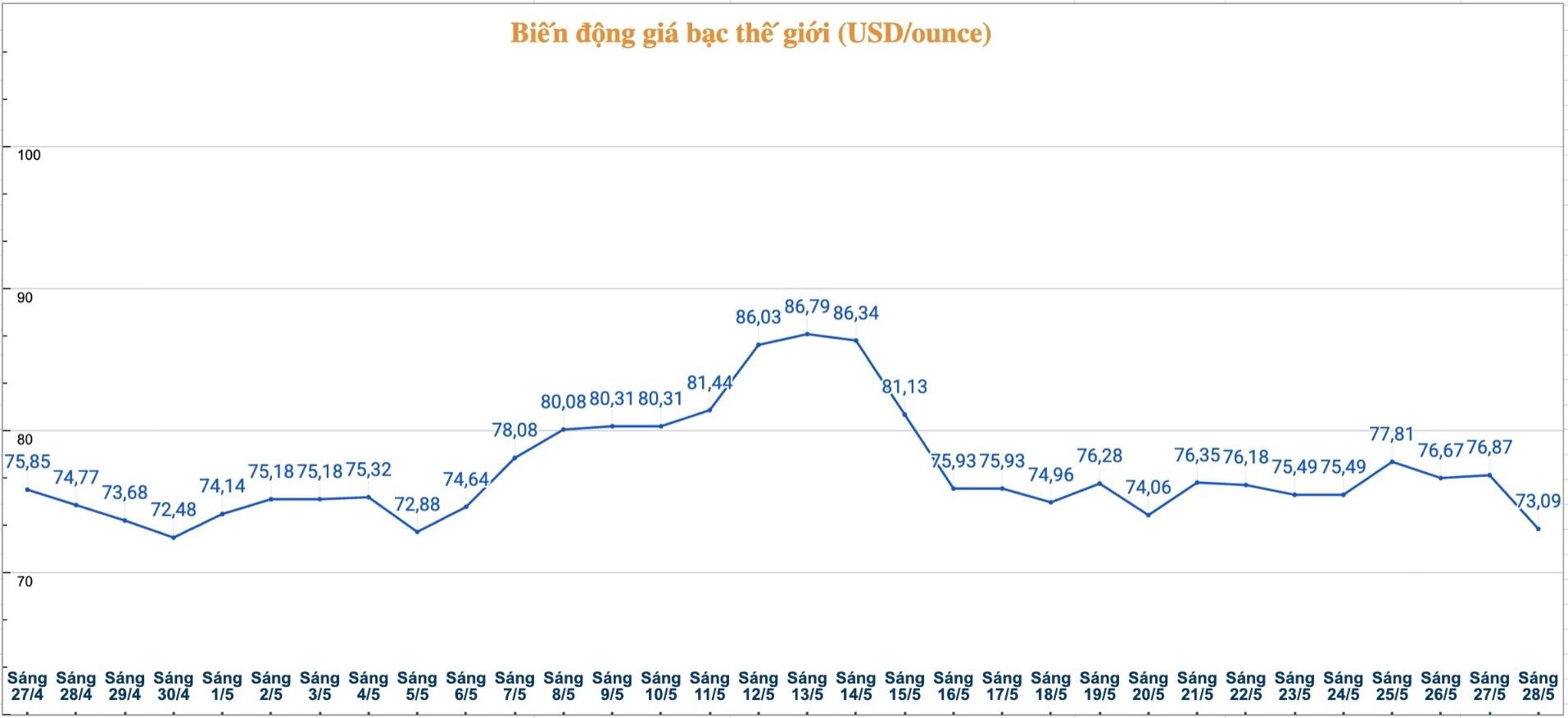

An important indicator mentioned by expert Rockefeller is the gold/silver ratio. In May 2025, this ratio quickly reached 100, only the second time in the past 50 years, showing that silver at that time was very cheap compared to gold. However, after recent fluctuations, the gold/silver ratio has returned to the long-term average of 50-60.

According to Mr. Moglia, this normalization shows that the relative increase in silver compared to gold is no longer as attractive as last year. In other words, silver still has a supporting foundation from industrial demand and supply deficits, but the outstanding increase compared to gold may narrow in the near future.

In that context, investors need to be cautious with the hot increases of silver. This metal may bring a larger profit margin than gold in market excitement periods, but also potentially risk strong correction when speculative cash flow reverses direction.