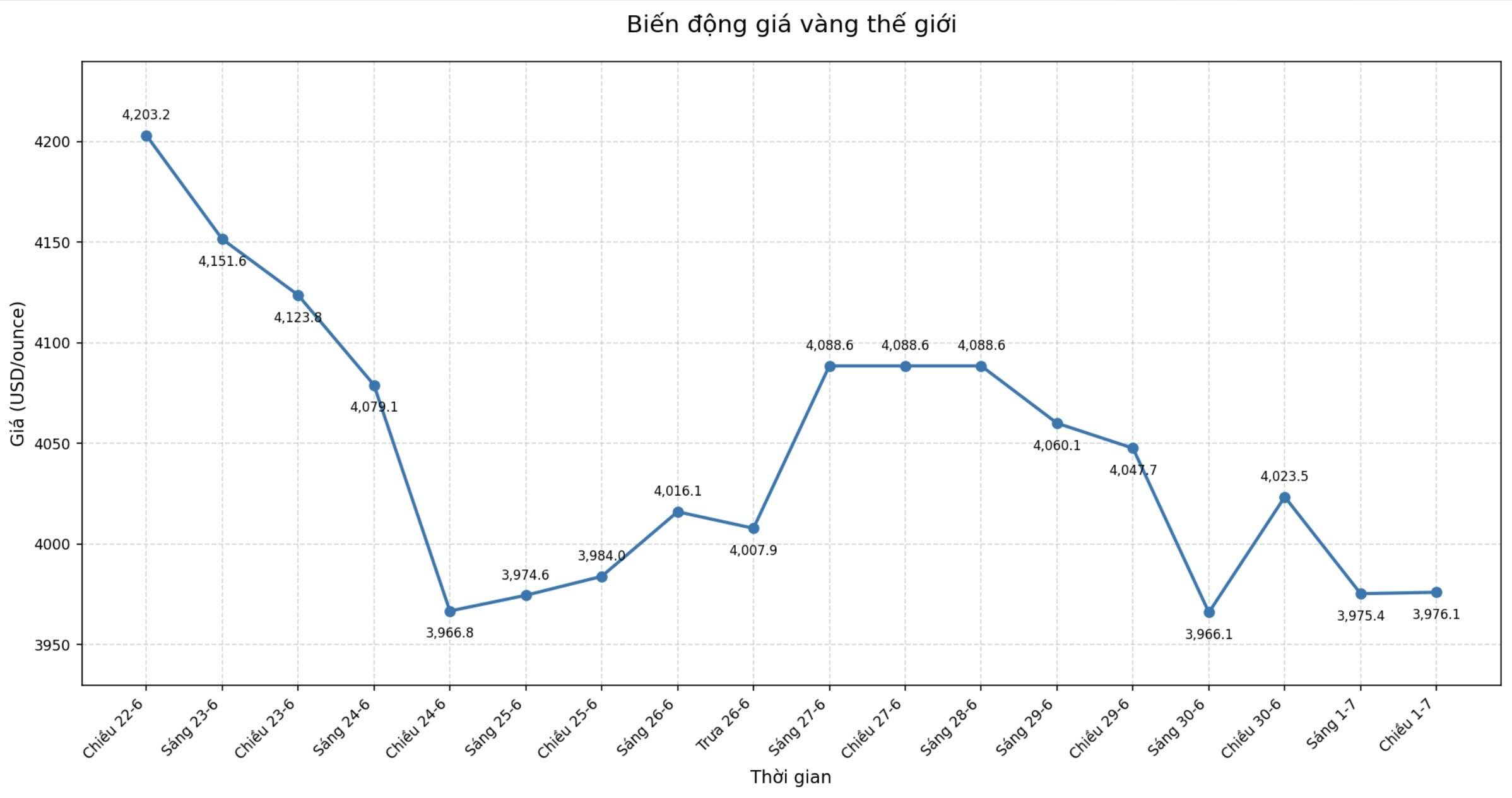

The world gold market is reacting more strongly to the monetary policy outlook of the US Federal Reserve (Fed) instead of the tense developments in the Middle East.

Although the US-Iran conflict and risks in the Strait of Hormuz have not been completely resolved, gold prices continue to face pressure as investors focus on the possibility of the Fed maintaining high interest rates for a long time.

This development shows that the traditional shelter role of gold is temporarily being overshadowed by macroeconomic factors. It can be seen that the market currently values gold mainly based on interest rate prospects, US Treasury bond yields and the strength of the USD instead of just reacting to geopolitical fluctuations.

The focus of the market is still the most recent meeting of the US Federal Open Market Committee (FOMC). The Fed maintained the target interest rate band at 3.50-3.75%, but at the same time raised the forecast for the 2026 centralized federal fund interest rate to 3.8%, higher than the 3.4% given in March. The 2026 PCE inflation forecast was also adjusted up from 2.7% to 3.6%, reflecting the Fed's more cautious view of inflation risk.

These signals were quickly strengthened as job data in the US continued to be positive. The JOLTS report showed that the number of vacancies in May exceeded market expectations, thereby increasing the perception that the Fed would not soon ease monetary policy. The yield of 10-year US Treasury bonds accordingly remained high, increasing the opportunity cost of holding gold - an asset that does not yield yields.

Meanwhile, geopolitical tensions are still developing complicatedly but no longer create enough momentum for precious metals. After concerns about maritime security in the Strait of Hormuz, the US and Iran have signaled the resumption of negotiations, helping the market reduce concerns about the risk of serious disruption to oil supply.

Although transportation through Hormuz has not yet fully returned to normal, most investors believe that oil flows will continue to be maintained. This makes oil prices still fluctuate but has not created a shock large enough to trigger a wave of gold seeking like in previous crisis periods.

Notably, rising oil prices in recent times have created a reverse impact on gold. Higher energy prices increase concerns about inflation, thereby strengthening expectations that the Fed will maintain a tougher stance for longer. As a result, priority cash flow reflects interest rate prospects instead of increasing gold holdings to hedge geopolitical risks.

Developments in the financial market also clearly reflect changes in investor sentiment. US stocks recovered as expectations of US-Iran talks resumed, while gold could not benefit from its role as a safe-haven asset. This shows that the market is considering gold as a asset sensitive to interest rates more than a tool to defend against geopolitical shocks in the short term.

Technically, gold still needs to rise back to the important resistance zone to confirm the recovery trend. Conversely, if support zones continue to be breached in the context of high bond yields and the USD, adjustment pressure may continue to be prolonged.

In the short term, the gold market is likely to continue to be mainly affected by US economic data, especially inflation and labor markets, along with Fed officials' statements. Only when monetary policy prospects become less tough or a geopolitical shock that is large enough to change global cash flow has gold the opportunity to regain the leading role of a safe-haven asset.