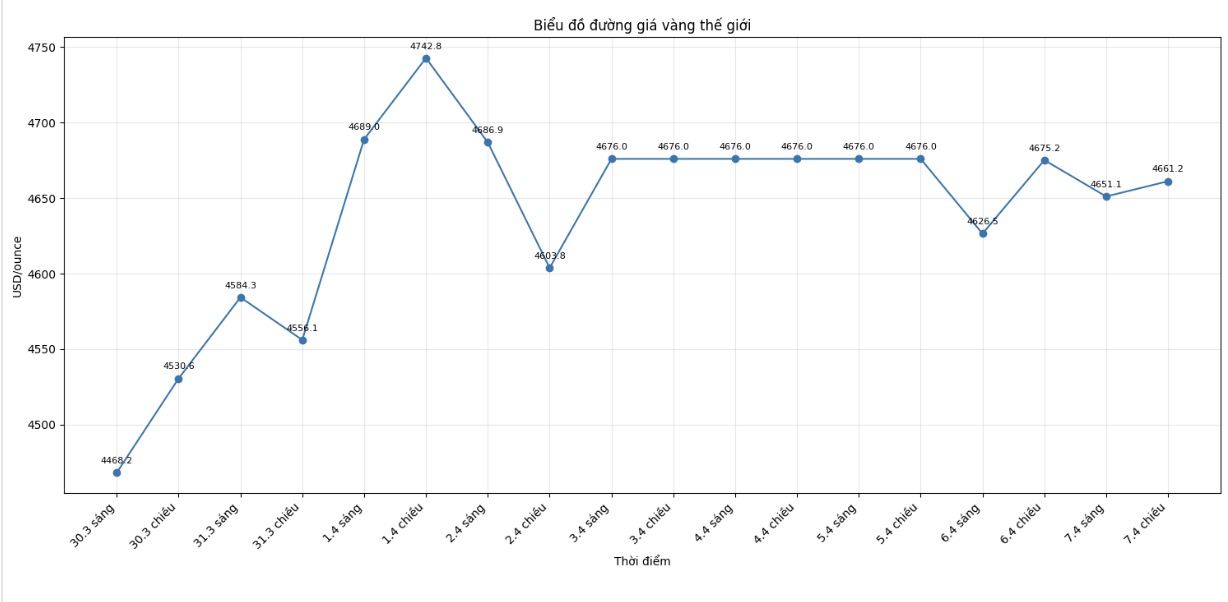

World gold prices are facing many short-term resistances, although the context of rising inflation and war tensions in Iran was once expected to strongly support the precious metal.

In the latest Capital Market Outlook report, Ms. Emily Avioli - Vice President and Investment Strategist at Merrill - said that recent developments in gold prices are going against traditional shelter roles.

According to Ms. Avioli, instead of breaking through as the Middle East conflict escalates, gold prices have weakened significantly. This precious metal has fallen by about 16% since the conflict began and tends to fluctuate in the same direction as risky assets in the past 4 weeks.

This opposite development raises the question of whether investors should still maintain an optimistic view of gold in the coming time.

However, Merrill's experts believe that the current adjustment mainly reflects investment position factors, interest rate expectations, and the strength of the USD, rather than the weakening of gold's fundamentals.

Ms. Avioli emphasized that the decline in gold prices appeared after a period of very strong increase. Supported by large purchases from central banks and the return of individual investors, gold prices have climbed since 2022 and once surpassed the 5,400 USD/ounce mark in January.

According to market rules, after too strong increases in a short period of time, goods often enter a stage of accumulation or adjustment to absorb the previous unusual increase. The current decrease in gold prices is said to be reflecting this process.

Another reason comes from profit-taking pressure. After a historic increase, investment positions in gold in the market have been at a prolonged level, causing many investors to take advantage of selling to preserve profits when risk avoidance sentiment appeared when war broke out.

In addition, the demand for selling gold to supplement liquidity may have been amplified when the amount of cash outside the market of investment institutions fell to a record low in January.

In addition, rising yields also put significant pressure on gold prices. Rising energy prices have raised concerns about inflation, thereby changing the outlook for monetary policy. The market is increasingly rejecting expectations of when the US Federal Reserve (Fed) will cut interest rates, even futures contracts reflecting the possibility that the Fed may continue to raise interest rates.

As real yields increase, the opportunity cost of holding non-genuine assets such as gold also increases, reducing the relative attractiveness of precious metals compared to income-generating investment channels.

The strengthening USD is also a major drag on gold prices. Since the conflict broke out, investors have tended to turn to the greenback as a safe haven asset. For decades, gold has often fluctuated in the opposite direction to the USD, as this precious metal has been seen as an alternative means of preserving value for the US dollar.

However, Ms. Avioli believes that the current difficulties do not change the structural drivers that have supported gold for many years.

According to this expert, a large fiscal deficit is still a constant concern, the USD is likely to return to a gradually weakening trend, while central banks still have the motivation to diversify foreign exchange reserves instead of being too dependent on the USD.

Merrill therefore still maintains the view that gold has a place in the balanced investment portfolio as a strategic diversification asset. As instability related to the Middle East conflict subsides, factors driving gold demand are expected to return soon.