World gold prices fell sharply in Tuesday's trading session, losing more than $100/ounce while the USD appreciated and concerns about inflation increased due to tensions related to Iran.

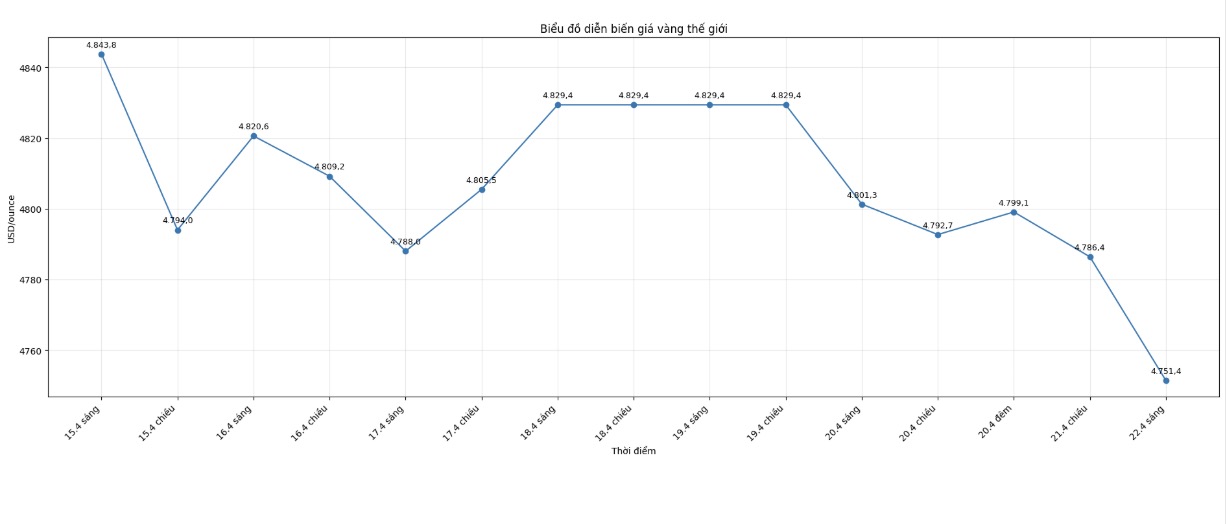

Opening at 4,842 USD/ounce, gold prices at times fell to nearly 4,700 USD/ounce during the session. The decline shows the paradox of the precious metal market: geopolitical tensions once pushed money to flock to gold as a safe haven, but also increased the risk of inflation and tight monetary policy - unfavorable factors for gold.

This morning, gold prices are recovering but still recorded a fairly deep decrease compared to the previous day. At the time of writing the article (9:00 AM on April 22 - Vietnam time), world gold prices were listed at 4,751.4 USD/ounce, while silver traded around 77.49 USD/ounce.

One of the biggest pressures on gold is the rise of the USD index. The strengthening greenback makes gold more expensive for investors holding other currencies, thereby weakening demand for this precious metal.

According to analysts, the market is currently particularly interested in the second round of negotiations between the US and Iran, scheduled to take place in Pakistan, before the 2-week ceasefire expires at the end of this week.

US President Donald Trump declared that he would not extend the ceasefire agreement if the two sides do not reach a new agreement. He also affirmed that the Strait of Hormuz will continue to be blockaded until there is progress in negotiations.

This development raises concerns about a large-scale energy supply shock, thereby increasing global inflationary pressure. In that context, the possibility of central banks continuing to maintain high interest rates, even raising interest rates, is becoming a factor putting pressure on gold prices.

Usually, rising interest rates will reduce the attractiveness of gold because this is a non-interest-generating asset. The opportunity cost of holding gold is therefore also higher.

Investors are also following a series of US economic data released this week, which could cause the market to fluctuate more strongly. Notably, the ADP jobs report, the number of initial jobless claims, the PMI index for April and the Michigan University inflation expectations survey.

If inflationary indexes continue to rise sharply, the possibility of the US Federal Reserve (FED) maintaining a tight monetary policy will be greater, thereby creating more adjustment pressure on gold prices.

Data from CME Group shows that the market is almost certain that the FED will keep interest rates unchanged in the range of 3.5% - 3.75% in April, with a probability of up to 99.5%.

However, in the long term, many major financial institutions still maintain a positive view of gold. JPMorgan and Goldman Sachs forecast that gold prices may fluctuate in the range of 4,000 - 6,300 USD/ounce in the period up to 2026, thanks to buying power from central banks and geopolitical risks that have not cooled down.

The demand for gold from central banks has slowed down in the first months of 2026 compared to the average of 27 tons/month of the previous year, but has expanded geographically. Malaysia, South Korea and China are all continuing to increase gold reserves.

This is considered an important support, helping to limit the risk of gold falling into a prolonged deep decline cycle.

In the short term, the gold market is still under pressure from a strong USD, inflation concerns and geopolitical risks. Developments from the negotiating table in Islamabad in the next few days may decide whether the recent decrease of more than 100 USD/ounce is just a short-term correction or the beginning of a deeper decline.