Supply increases, liquidity decreases

In Q2/2026, according to the One Mount Group Market Research & Customer Understanding Center, the primary apartment market in Hanoi and Ho Chi Minh City both recorded a clear improvement in supply compared to the first quarter of the year.

In Hanoi, the total new supply reached about 9,300 units, an increase of 6% quarter-on-quarter and 23% compared to the same period last year. Meanwhile, in Ho Chi Minh City, the new supply reached about 11,000 units, an increase of 51% compared to the same period last year.

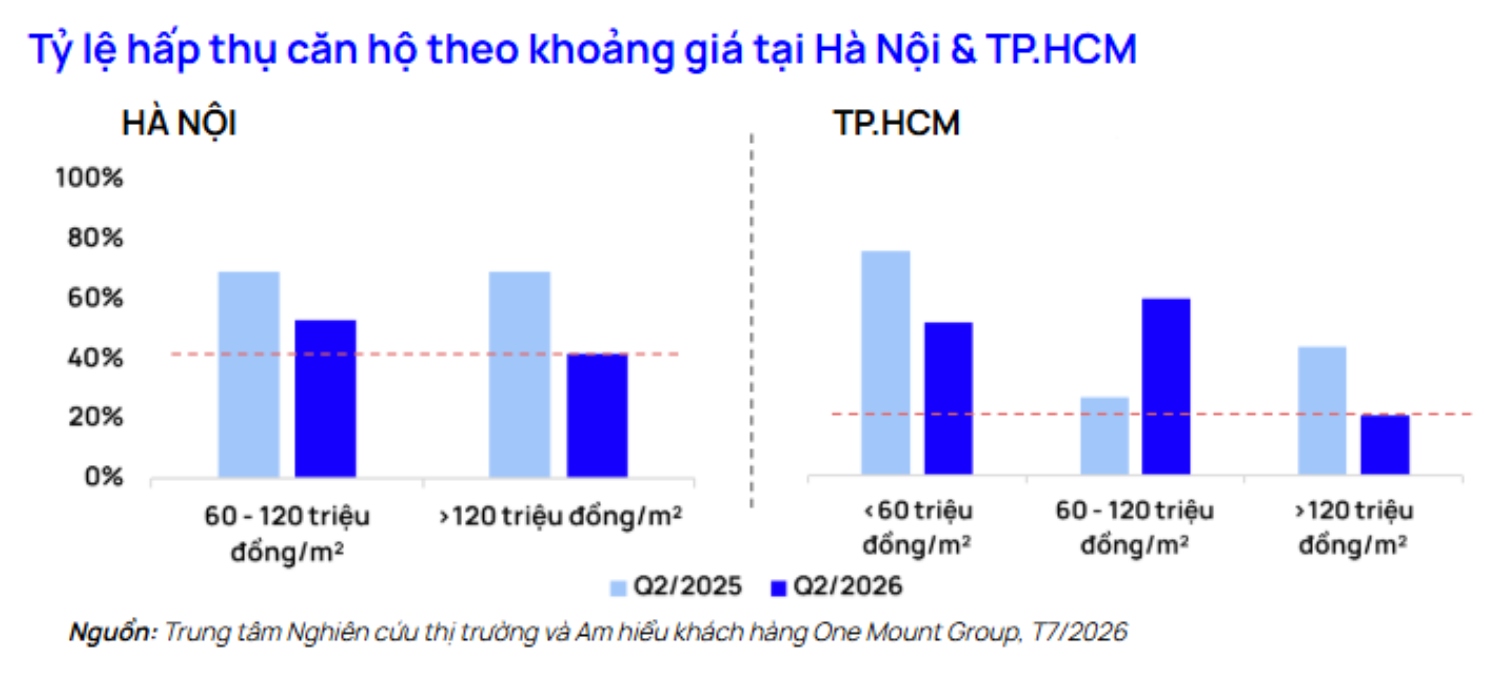

Under the impact of the macroeconomic context, market demand in Q2/2026 shows signs of slowing down compared to the previous quarter. However, instead of uniform decline, liquidity is clearly differentiated: projects under 120 million VND/m2 record positive absorption rates, while the price group higher than 120 million VND/m2 faces a longer selling process.

In Hanoi, the market consumed 7,100 apartments, down 3% quarter-on-quarter and down 8% year-on-year. The absorption rate in the quarter reached 50%, down 18 percentage points compared to the same period in 2025. Notably, projects priced above 120 million VND/m2 recorded slower liquidity with an absorption rate of only 53%, significantly lower than the same period last year (69%).

In Ho Chi Minh City, the market recorded 9,500 transactions, an increase of 16% compared to the same period last year. However, the absorption rate only reached about 50%, down 2 percentage points compared to the first quarter of 2025. In which, projects in the price segment from 60-120 million VND/m2 played a leading role, accounting for 53% of total market transactions and achieving an absorption rate of 59%. Conversely, the absorption rate of product groups with prices above 120 million VND/m2 only reached 20%.

Realizing that demand has stagnated, many investors have proactively adjusted their sales strategies in the second quarter of 2026. Some projects recorded official opening prices lower than previously announced, and at the same time applied support policies such as extending payment schedules and preferential interest rates up to 5 years to improve the accessibility of buyers.

In the center of Hanoi, the average selling price in Q2/2026 reached 121 million VND/m2, unchanged compared to the previous quarter and up 46% compared to the same period last year.

The primary price level in Ho Chi Minh City in Q2/2026 continued to record differentiation by region. In the central area, the primary selling price reached about 103 million VND/m2, maintaining relatively stable compared to the previous quarter.

New supply forecast to increase

In the second half of 2026, the primary market in Hanoi and Ho Chi Minh City is forecast to continue to record an increase in new supply as many projects are in the completion phase to be eligible for sale.

In the last 6 months of 2026, Hanoi is forecast to add about 17,000 - 23,000 new apartments, raising the total sales volume for the whole year to 35,000 - 40,000 units. Selling prices in the center of Hanoi are expected to grow by 10 - 13%, while the Van Giang area (Hung Yen) is forecast to increase slightly by 3-5% compared to last year thanks to the launch of many new projects with reasonable prices.

In the last 6 months of 2026, Ho Chi Minh City is expected to add about 15,000 - 20,000 new apartments, bringing the total supply for sale for the whole year to about 30,000 - 35,000 units. However, selling prices in the center of Ho Chi Minh City are expected to remain relatively stable, with an increase of 3-5% compared to 2025. Meanwhile, Binh Duong area is forecast to have faster price growth (about 15-20% YoY), thanks to the participation of foreign investors with projects with increasingly high-end finishing standards.

One Mount Group Market Research and Customer Understanding Center commented: "Faced with macroeconomic fluctuations, the real estate market is recording a clear shift in the psychology and behavior of homebuyers. Instead of heavily relying on financial leverage as in the previous period, current cash flow is tending to prioritize products with reasonable prices, good development quality and the ability to meet real housing needs will continue to be the group leading liquidity in the coming time.