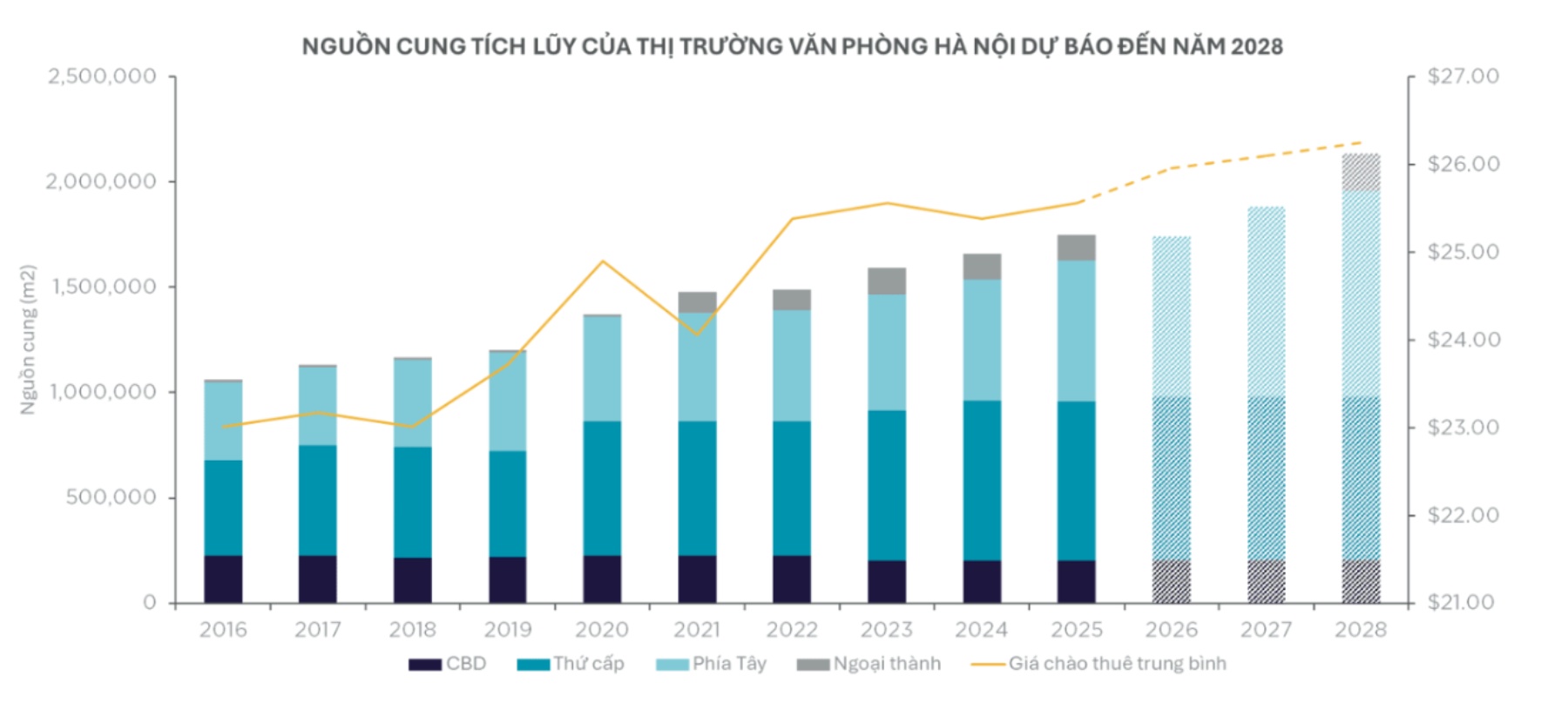

According to a report by Cushman & Wakefield Vietnam, in the past ten years, the total office supply in Hanoi has increased by about 160%, reaching approximately 1.74 million m2 in 2025. Grade A supply leads this growth momentum, increasing faster than Grade B and bringing tenants more high-quality choices in the high-end segment of the market.

At the same time, Hanoi is still one of the cities with the smallest scale of Grade A office supply in the Asia-Pacific region, although the rental price is among the highest in the region.

This shows that the market is still relatively limited in terms of high-end supply compared to the regional average, but still continues to attract demand from tenants looking for higher quality, more efficient and ready-to-future workspaces.

The Hanoi office market is no longer simply defined by scale expansion, tenants are becoming more selective, prioritizing quality, operational efficiency, location strategy and ESG standards. This is changing rental decisions across the market" - Mr. Nguyen Phuoc Thuan, Director of Leasing Department of Cushman & Wakefield Vietnam, said.

An important structural trend is that office supply is shifting out of the center. While Hoan Kiem is still Hanoi's traditional CBD area, office supply is now distributed in many areas, including Ba Dinh, Dong Da, Cau Giay and Tay Ho. Ba Dinh concentrates many high-class buildings, while Cau Giay currently accounts for the largest proportion of supply in the entire market. In the coming time, the development momentum of the market is shifting more strongly to the West, with Starlake and Tay Ho Tay expected to become the next large office clusters attracting significant attention.

Another notable change is the increase in the supply of green-certified offices. New certifications and upgrade activities across Hanoi are gradually raising market expectations, while creating pressure for old assets to maintain competitiveness through renovation and repositioning. LEED and EDGE certified buildings are increasingly clearly appearing in the market, strengthening the increasingly important role of sustainability and building performance factors in the decision-making process of tenants.

In the coming time, Hanoi is forecast to welcome a significant supply wave in the next 3 to 5 years, with more than 120,000 m2 of new office space expected to enter the market each year, mainly from Grade A projects outside the traditional CBD area.

As the market continues to mature, the next chapter of the Hanoi office market is expected to be shaped by a multi-polar development trend, flexible workplace design, efficient operation and development orientation associated with ESG. Office projects that are well managed, associated with convenient transportation infrastructure and multi-functional integration are likely to be in the best position to capture future demands.

According to Savills Vietnam, it is forecast that by 2028, the Hanoi office market is expected to add about 403,000 m2 of new supply, of which Grade A dominates and concentrates in the West and Inner City areas, with limited supply in the central area, showing a trend shifting to higher quality and more distributed supply.

Demand is still assessed as positive but selective, thanks to growth in the service sector and FDI capital flows. The market is developing in a multi-polar direction and associated with infrastructure, while the central area continues to play a role as a focal point for headquarters and high-value functions.

Expanding beyond the central area is no longer just a story of cost optimization, but has become a strategic decision. This trend is driven by increasingly complete infrastructure, higher quality supply, abundant access to human resources, and increasing interest in utilities that truly meet the daily operating needs of businesses and human resources" - Mr. William Gramond, Director of Commercial Leasing Department of Savills Hanoi said.