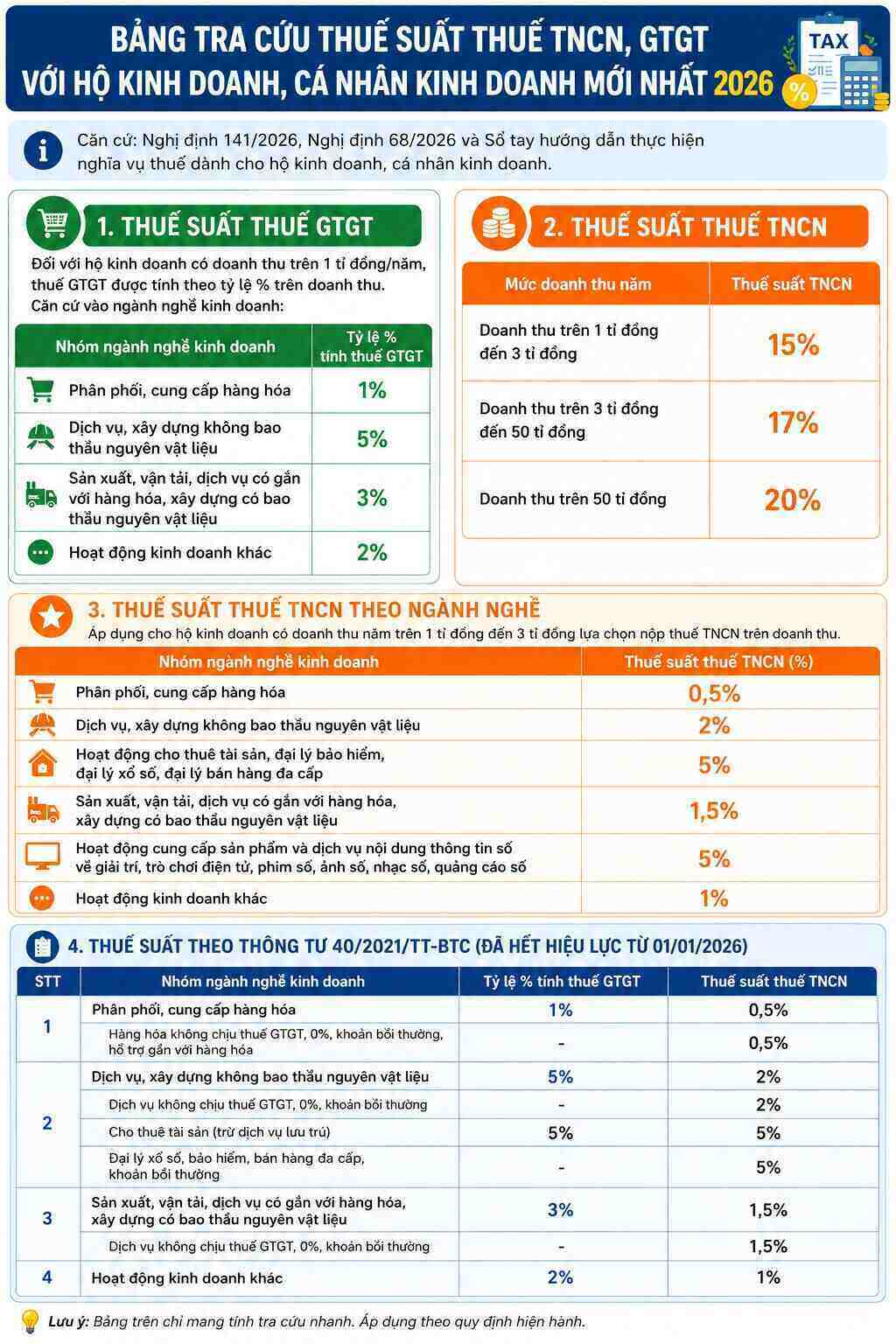

Based on Decree 141/2026/ND-CP, Decree 68/2026/ND-CP and the latest Tax Obligation Guidance Handbook, regulations on tax rates for business households and individual businesses are specified as follows:

1. Value Added Tax (VAT) rate

For business households with revenue over 1 billion VND/year, VAT is calculated as a percentage based on specific business lines:

1% ratio: Applied to the group of distribution and supply industries.

2% ratio: Applied to other business activities.

3% ratio: Applied to production, transportation, services associated with goods, and construction with raw material bidding.

5% ratio: Applied to the group of service and construction industries not bidding for raw materials.

2. Personal Income Tax (PIT) Rate

The determination of the PIT tax rate is divided into two main cases based on the scale and method of tax payment:

Case 1: Accumulative annual revenue tax rate

Revenue over 1 billion to 3 billion VND: Tax rate is 15%.

Revenue over 3 billion to 50 billion VND: Tax rate is 17%.

Revenue over 50 billion VND: Tax rate is 20%.

Case 2: Industry tax rate (Exclusively for business households with revenue from 1 billion to 3 billion VND to choose to apply)

0.5% level: Applied to distribution and supply activities of goods.

1% level: Applied to other business activities.

1.5% level: Applied to production, transportation, services associated with goods; construction with raw material bidding.

2% level: Applied to services, construction not bidding for raw materials.

5% level: Applied to asset leasing activities, insurance agents, lottery agents, multi-level marketing agents; and activities providing digital information content products and services (such as entertainment, electronic games, digital movies, digital photos, digital music, digital advertising).