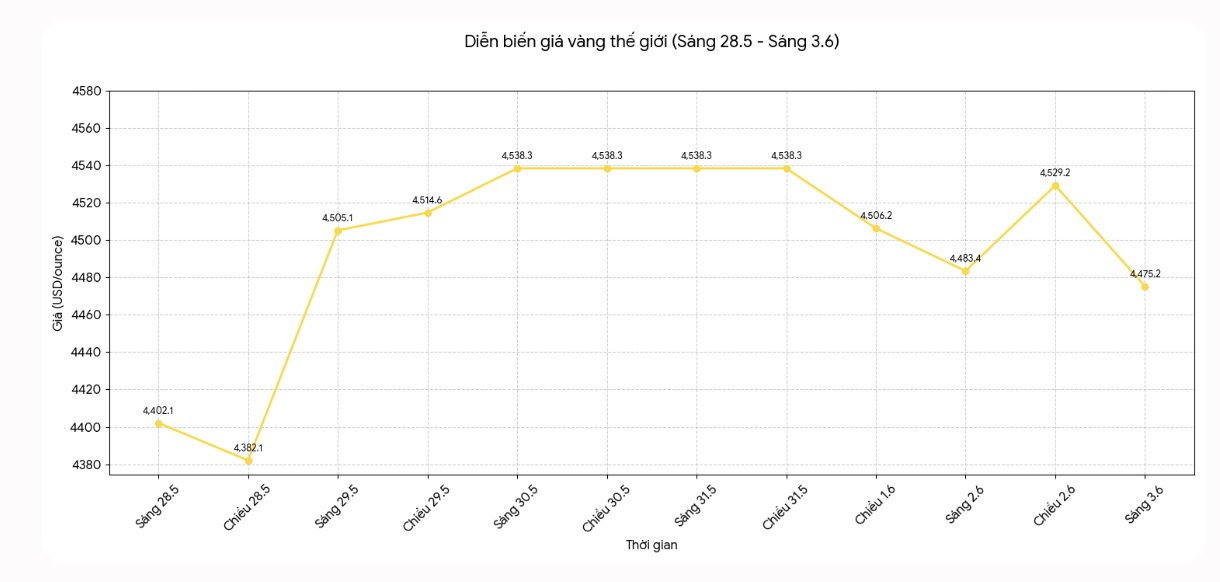

After the first time exceeding the 5,000 USD/ounce mark this year, world gold prices have entered a period of accumulation around the 4,494 USD/ounce mark. Although no longer maintaining the hot upward momentum as before, this precious metal is still assessed by many major financial institutions as having a lot of room to rise in the second half of 2026.

A noteworthy point is that the gold price forecasts for the end of this year are strongly differentiated. Some organizations offer quite cautious scenarios, while many large institutions believe that gold prices may continue to set new highs if macroeconomic factors are favorable.

Goldman Sachs maintains its gold price target at 5,400 USD/ounce by the end of 2026, despite the precious metal having had a strong correction in March. Meanwhile, J.P. Morgan raised the 90-day target to 5,000 USD/ounce and said that in a more positive scenario, gold prices could head towards the 6,000-6,300 USD/ounce range.

Morgan Stanley offers a base scenario around 4,800 USD/ounce in Q4/2026. More cautiously, Macquarie forecasts an average gold price in 2026 at 4,323 USD/ounce, due to concerns that rising US bond yields could put pressure on the precious metal.

A Financial Times survey of 11 analysts showed a consensual forecast for gold prices at the end of the year of $4,610/ounce. However, some opinions suggest that the risk of price increases is greater than the risk of decreases, especially in the context that gold demand from central banks remains high.

According to experts, one of the most important supporting factors for gold prices is the trend of central banks, especially in emerging economies, continuing to increase gold holdings to reduce dependence on the USD. This level of sovereignty demand is considered a sustainable support for gold prices in the medium and long term.

In addition, the monetary policy of the US Federal Reserve (Fed) continues to be a key variable. If the Fed resumes its interest rate cut cycle, the opportunity cost of holding gold will decrease, while the USD may weaken.

The World Gold Council estimates that if interest rates fall more sharply than expected, gold prices could increase by another 5-15% compared to the current zone. In the event that the US economy declines more seriously, the increase could be up to 15-30%.

The trend of dedollarization is also being closely monitored by the market. J.P. Morgan strategists believe that if only 0.5% of US assets held by foreigners are redistributed to gold, this capital flow may be enough to push gold prices up to 6,000 USD/ounce. This is a scenario that was once considered distant, but is now being mentioned more and more in major investors.

In addition, geopolitical risks, trade disputes and inflation hedging needs are still factors supporting gold prices. Capital inflows into gold ETFs also show signs of increasing in 2026, as Western investors return to the precious metal after a period of maintaining a low proportion.

However, the scenario of gold price increase is not without risks. If inflation in the US increases again, forcing the Fed to keep interest rates higher for longer or reverse policy, real yields may increase and the USD strengthen. This is a complex that often adversely affects gold prices. UBS also assesses the Fed's tougher stance as the biggest risk of devaluation for precious metals.

In addition, if major geopolitical conflicts cool down, safe-haven demand may decline, leading to capital withdrawal from gold. Record high prices are also somewhat curbing physical gold demand in price-sensitive markets, especially in Asia.

Although there are still many variables, most experts believe that demand from central banks and Asian buyers may create a support zone for gold prices. The sustained decline of gold prices below 4,000 USD/ounce is assessed to only occur if a major deflation shock occurs - a scenario that many organizations have not yet predicted.

With the current level, gold prices are said to be facing an important turning point. If the Fed cuts interest rates more sharply than expected or confidence in USD-denominated assets continues to weaken, the precious metal may enter a new wave of increase. Conversely, high interest rates and a strong USD are still major obstacles for the market.