According to Mr. Ray Jia - Head of China Research at the World Gold Council (WGC), the Chinese gold market in July reflected the relatively stability of gold prices, with capital withdrawn from ETFs, futures contracts continued to decrease, while imports recorded the weakest first half of the year since 2021.

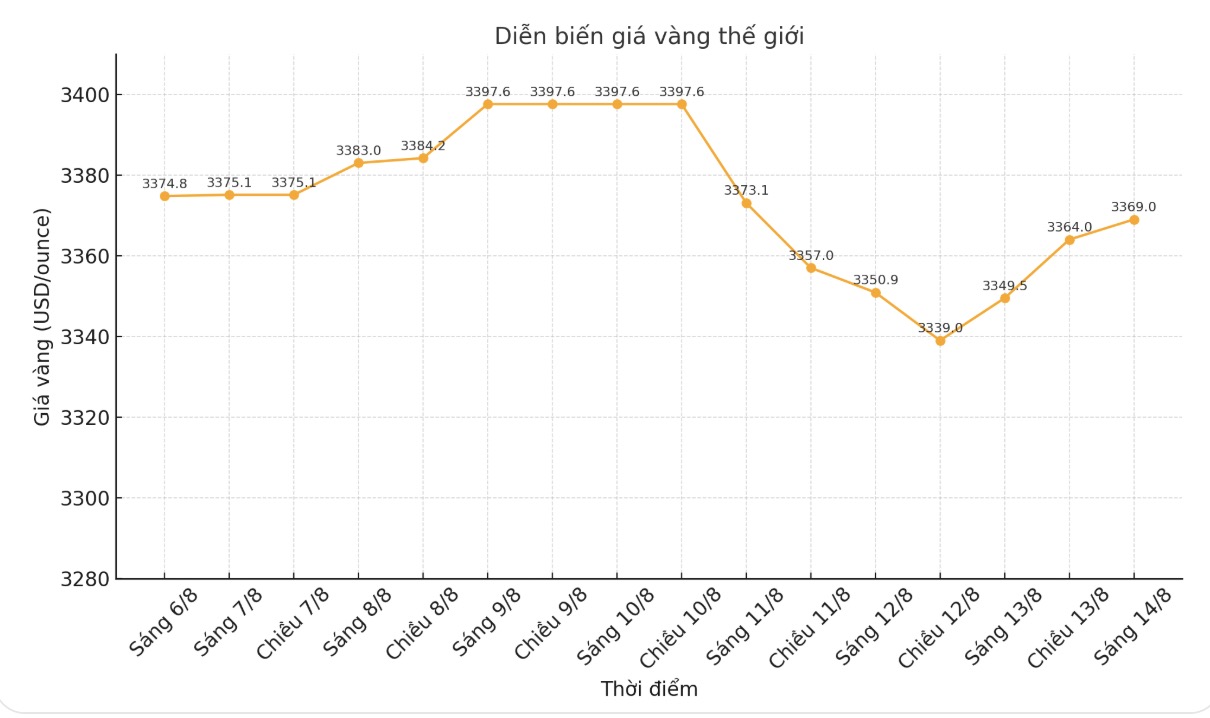

He said that despite the stronger US dollar, concerns about inflation and other risks still prevailed, causing gold prices to increase only slightly. LBMA PM gold standard price (afternoon fixed price announced by the London Gold Market Association, used as international trading standard) calculated in USD increased by 0.3% compared to the previous month.

Meanwhile, the SHAUPM gold price (Shanghai Gold Benchmark PM Price - afternoon standard price announced by the Shanghai Gold Exchange, reflecting the gold price in China) calculated in yuan (RMB) increased by 0.5% due to the RMB depreciating against the USD.

Since the beginning of the year, gold prices in China have increased by more than 22%, far exceeding the increase of most domestic assets.

Retail demand increases slightly thanks to seasonal factors

The amount of gold withdrawn from the Shanghai Gold Exchange (SGE) reached 93 tons in July, up 3 tons compared to the previous month and up 4 tons compared to the same period last year, Jia wrote. This slight increase is mainly due to seasonal factors: jewelry demand often improves in the third quarter.

In addition, better gold bar sales when investors take advantage of stable prices also contribute to the recovery of wholesale demand in July".

However, he warned that this figure is still much lower than the 10-year average, reflecting weak wholesale demand this year, especially in the jewelry segment.

While demand for gold investment continues to increase strongly, jewelry consumption calculated by volume has decreased sharply, causing jewelry businesses hoarding activities to stagnate, said the expert.

Gold ETFs in China Re return to negative status

Mr. Jia said that Chinese gold ETFs recorded a net withdrawal of 2.4 billion RMB (325 million USD) in January: "Due to withdrawal and sideways gold prices, total assets under management decreased slightly by 1% to 151 billion RMB (21 billion USD), holding volume decreased by 3 tons to 197 tons".

However, since the beginning of the year, gold ETFs have recorded a record capital of 61 billion RMB (8.5 billion USD, 82 tons).

In the stock market, China's second quarter GDP exceeded expectations, boosting risk appetite and giving the CSI300 index its strongest month of increase since September 2024. Local government bond yields continue to rise as the economy shows signs of recovery and the expectation of a rate cut by the People's Bank of China (PBoC) has decreased. These factors, combined with a lack of clear trends in gold prices, have reduced the appeal of ETF gold in the month.

In the futures market, the trading volume at the Shanghai Commodity Exchange (SHFE) will average 242 tons/day, down 18% compared to the previous month but still higher than the 5-year average (216 tons/day). The main reason is that gold prices fluctuate narrowly and price fluctuations decrease, reducing the interest of traders.

The PBoC continued to buy gold in July (an additional 2 tons), recording the 9th consecutive month of buying. After 9 consecutive months of buying, China's official gold reserves reached 2,300 tons, accounting for 6.8% of total reserves, up 21 tons from the beginning of 2025.

June import data showed that gold imports in the first half of 2025 were very low. In June, China imported 50 tons, down 45% compared to the previous month, bringing the total in the second quarter to 250 tons, down 18% compared to the same period in 2024. In the first 6 months of the year, total imports reached only 323 tons, down 62% over the same period last year.

Looking ahead, the WGC predicts that the demand for wholesale gold in China will continue to improve seasonally, especially in the jewelry sector, although high prices could keep volumes low. The demand for gold bars and coins will depend on gold price developments and general risk appetite, in which the recent increase in stocks may distract attention.