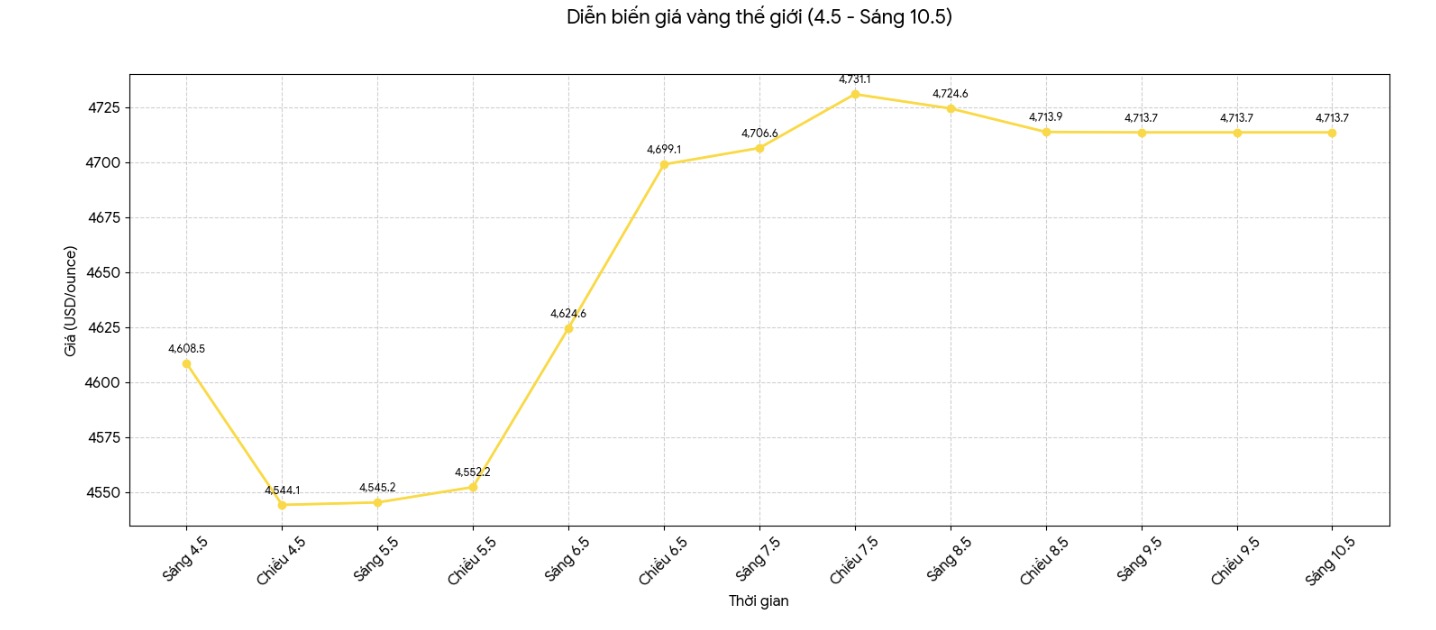

According to Kitco, world gold prices may be in a period of accumulation, but buying demand from central banks is still sending strong support signals for the precious metals market.

The latest data from the World Gold Council shows that central banks net sold about 30 tons of gold in March. The main reason comes from large-scale sales by Turkey and Russia.

However, the overall picture of the gold market is still positively assessed as many countries continue to increase reserves during the price adjustment period. Poland, Uzbekistan and Kazakhstan maintain stable buying activities, while China continues to extend its gold accumulation streak for many consecutive months.

According to analysts, the important thing is not a short-term net selling month, but the strategic trend that has formed in the past 4 years. Gold accumulation is increasingly seen as a long-term policy to diversify foreign exchange reserves, respond to geopolitical instability and reduce dependence on the USD.

China continues to play a central role in this trend. The People's Bank of China has increased its official gold reserves for 18 consecutive months. Data shows that this agency is still taking advantage of buying more when prices fall.

In March alone, China bought an additional 8 tons of gold - the largest purchase since December 2024 - amid gold prices being about 16% lower than the historical peak set in January 2026.

Experts believe that what is more noteworthy is that the proportion of gold in total global reserves is still relatively low. According to the World Gold Council, gold currently accounts for only about 15% of total global reserve assets, meaning the room to increase the proportion is still large.

Even when gold prices are at a high level, many countries are still starting to participate in the market. Kosovo recently bought gold reserves for the first time, showing that even small central banks want to strengthen the stability of reserve assets through precious metals.

This development reinforces the view that the role of gold in the global monetary system is expanding instead of declining.

Analysts also believe that demand from the formal sector is currently less sensitive to price fluctuations compared to previous cycles. This shows that central banks are focusing more on long-term strategies than short-term market fluctuations.

The buying activity of central banks is contributing to creating a "buffer zone" to support gold prices. Although speculative cash flow or ETF funds can still cause prices to fluctuate strongly in the short term, buying power from the official sector helps the market have a more stable foundation each time it adjusts.

However, experts warn that gold may still be under pressure if bond yields rise, the USD strengthens, or geopolitical tensions change rapidly.

However, as long as central banks consider gold as a core reserve asset, deep declines are likely to continue to trigger new buying power from this sector.