Apartment attracts cash flow and real shelter needs

At the "Overview of the Real Estate Market in Q1/2026" event, Ms. Do Thi Ngoc Anh - Senior Business Manager of Batdongsan. com. vn commented that while the level of market interest has recovered after Tet, cash flow and buyer behavior are not evenly distributed, but focus on segments with real-use value and better resistance to macroeconomic fluctuations.

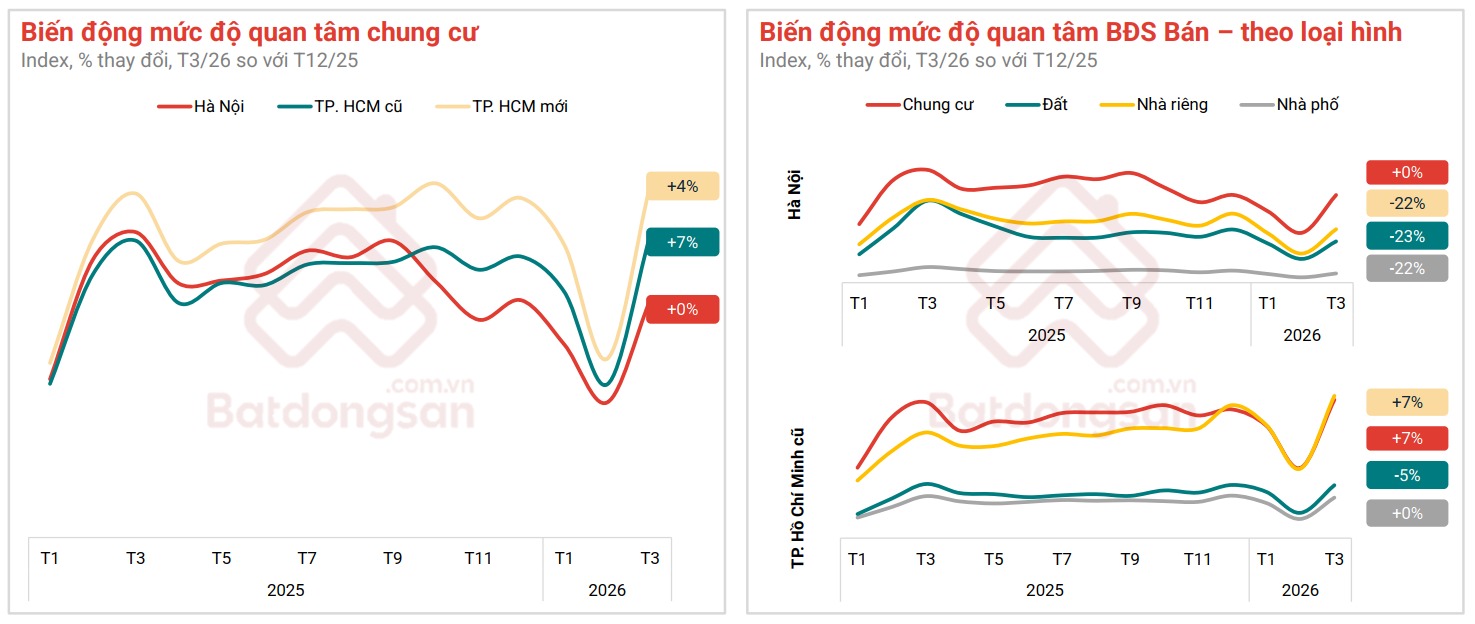

In the differentiated picture, apartments are a prominent segment with growth in interest level, playing a leading role in the recovery momentum of the national market.

Data shows that the level of interest in apartments in many areas in March 2026 increased by 4% - 7% compared to December 2025. This is a significantly higher increase compared to other types, reflecting the search flow returning to this segment.

Not only in terms of search behavior, apartments are also considered the type with the highest liquidity potential in the next 6 months, according to a survey with brokers. A noteworthy point is that the proportion of buyers to live in accounts for the majority.

According to a survey by Batdongsan. com. vn in the first quarter of 2026, 67% of apartment buyers aim to live in, 30% buy to invest in rent and only 4% surf the wave. Ms. Ngoc Anh said that in the past, there were times when the proportion of apartment buyers to surf the wave was up to 30% - 40%. This change reflects a clear shift from short-term investment to real use needs.

In the context of interest rates and macroeconomic factors still fluctuating, apartment selling prices remain stable, with a slight increase of about 1.5% to 2.4% quarter-on-quarter. In Q1/2026, the average asking price of apartments in Hanoi reached 87 million VND/m2 and 69 million VND/m2 in Ho Chi Minh City, showing the "holding price" ability of the segment, thanks to a more sustainable demand base compared to speculative types.

Hanoians move to provinces, Ho Chi Minh City people prefer suburbs

Ms. Do Thi Ngoc Anh - Senior Business Manager of Batdongsan. com. vn shared that the formation of the infrastructure-based urban development model (TOD) is increasingly clear, as new projects are no longer spread out but focus on key traffic axes.

Specifically, Hanoi is developing according to the "belt - across river" structure. Growth momentum is associated with the expansion of urban space, new projects spread evenly from the inner city area along Ring Road 2, Ring Road 3 to the East and West areas. In Ho Chi Minh City, new supply is concentrated in the near-central area, especially along National Highway 13.

This trend demonstrates the strategic shift of real estate towards infrastructure development, where each project is not simply a housing product but also associated with flexible connectivity and sustainable added value in the long term.

Big data from Batdongsan.com.vn also reflects the different shifts in interest between the two major cities. People in Ho Chi Minh City are gradually expanding to the inner city suburbs, especially in Ring Road 3. The proportion of interest in areas around Ring Road 3 and the expanded Ring Road 3 has increased from 39% in 2023 to 46% in the first quarter of 2026.

According to Ms. Ngoc Anh, there are differences in the specific investment psychology of each region: "Investors in Ho Chi Minh City tend to follow adjacent markets, associated with infrastructure and connectivity, while Hanoians tend to expand their portfolios to many different geographical areas.

The proportion of apartment searches in Hanoi decreased from 91% in 2023 to 76% in the first quarter of 2026, while the proportion of interest in apartments in the Northern and Central provinces gradually increased over the years. Specifically, in the Northern region, the provinces attracting the largest number of apartment searches from Hanoi people are Hung Yen and Hai Phong; while in the Central region, Da Nang and Khanh Hoa are two attractive destinations for investors from the Capital.