According to Cushman & Wakefield Vietnam's 10-year review of the Hanoi housing market report, the market is entering a new stage of development, in which future growth is expected to expand further than the traditional urban core. If the past decade was marked by strong price increases in both apartment and townhouse segments, then the next stage of the market is likely to be increasingly shaped by the trend of expansion to the suburbs, the formation of new development corridors and the appearance of large-scale urban poles in the expanded Hanoi area.

Apartment market shifts towards a multi-polar market

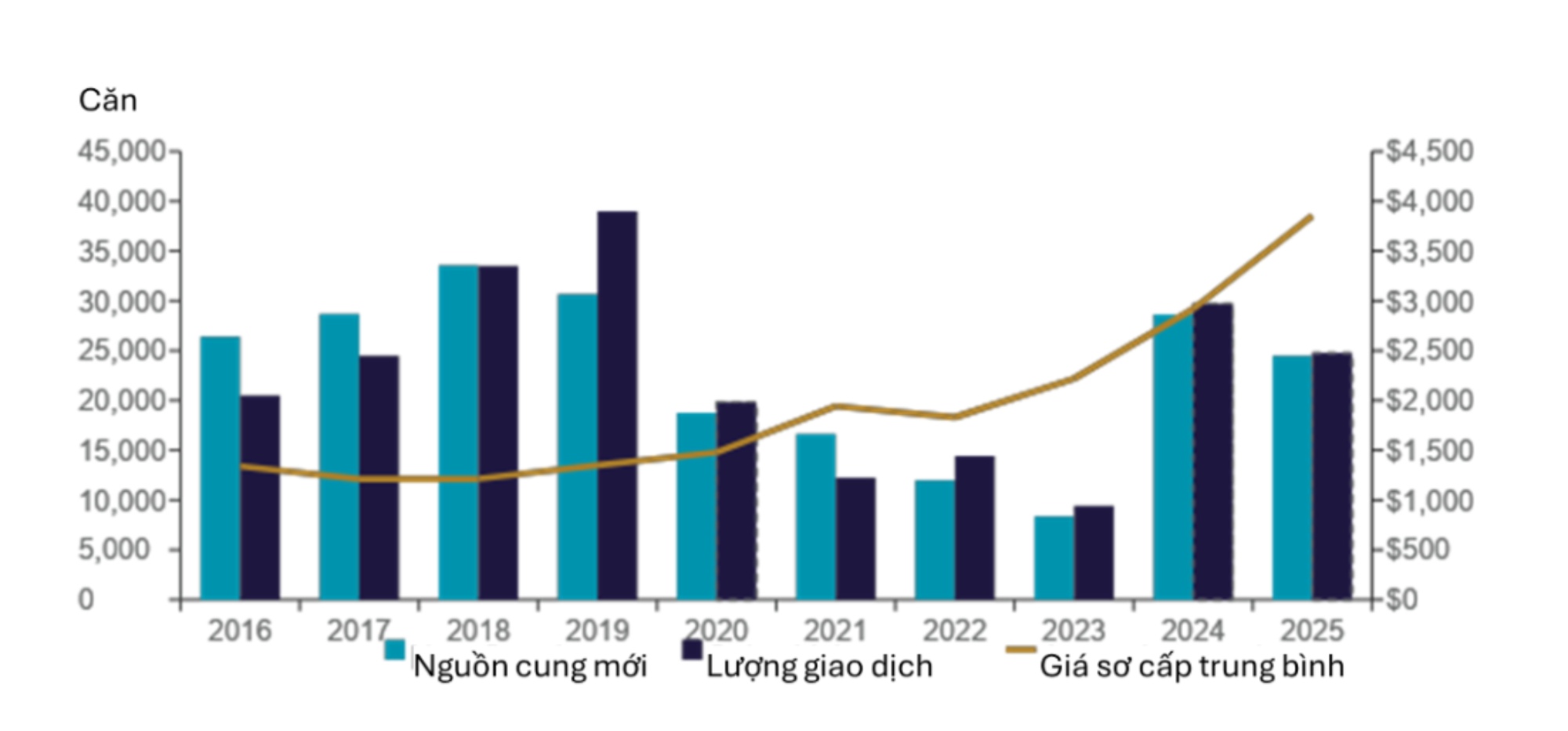

According to Cushman & Wakefield Vietnam, in the past 10 years, the Hanoi apartment market has recorded significant growth, with total supply increasing 2.9 times and the average primary price increasing 288%, equivalent to a compound annual growth rate (CAGR) of 11%.

According to Cushman & Wakefield Vietnam, the persistent increase in primary prices in this period partly comes from the shortage of affordable housing supply.

Not only changing in price and supply, the Hanoi apartment market is also undergoing a larger structural shift. Housing projects have gradually expanded from the initial urban area model to a more diverse location range, including suburban areas, the West, secondary areas and locations associated with the center. This shows that the market is increasingly moving in a multi-polar direction. That trend is forecast to be even clearer in the next decade. Apartment supply in the expanded Hanoi area is forecast to increase from at least 440,000 units in 710 projects in 2025 to at least 760,000 units in 1,150 projects in 2035.

Most of this new supply is expected to appear in new residential areas more than 30km from the city center, while many large-scale urban poles will also join the market and contribute to the formation of satellite cities in the future. Ring roads, new bridges and the implementation of the 2024 Land Law from 2026 are important drivers for this next growth phase.

Landed houses: supply increases slowly, but value still increases

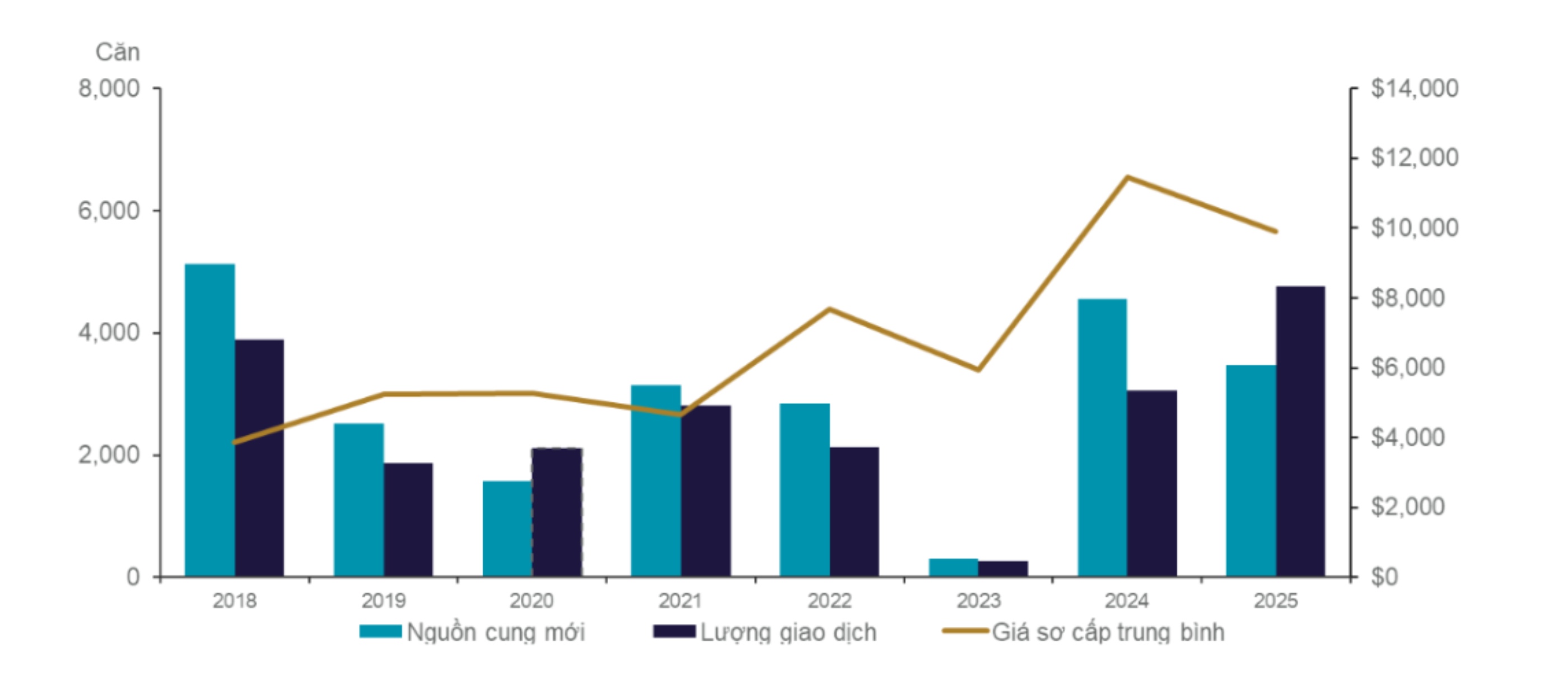

The landed house segment has different supply developments, but still recorded a noteworthy price increase trajectory. In the assessment period, total supply increased 1.4 times, while the average primary price increased by 257%, equivalent to CAGR 13%. Although the supply growth rate is lower than the apartment segment, this segment still maintains a strong value increase.

In the coming period, the supply of landed houses in the expanded Hanoi area is forecast to increase from at least 132,000 units belonging to 520 projects in 2025 to at least 210,000 units belonging to 700 projects in 2035.

Similar to the apartment segment, the supply of landed houses in the future is expected to continue to spread outside the city center, thanks to the emergence of large-scale urban poles and the improvement of inter-regional infrastructure connectivity. Ring Roads 1, 2, 3 and 4, along with the highway and metro system, are reportedly identified as important long-term drivers for value growth.

Ms. Nguyen Ly Ly - Market Research Manager, Cushman & Wakefield Vietnam, said: "In the past 10 years, Hanoi's housing market has gone through many different stages, from recovery after a period of economic weakness and high interest rates, to strong growth, stagnation under the impact of Covid-19, legal and credit tightening, before entering a recent recovery phase. Throughout that cycle, the price level continued the upward trend. In the coming period, when the market expands to areas outside the center and new urban poles are more clearly formed, we believe that there will be more room to develop supply at more diverse price levels, thereby opening up opportunities for products that are more suitable for real housing needs.