Supply recovery, product structure shift

Sharing at the Conference to announce the Real Estate Market Report for the first quarter of 2026 with the theme "Macroeconomic Fluctuations and Restructuring Period" organized by the Vietnam Association of Realtors (VARS) on the afternoon of April 15, 2026, Ms. Pham Thi Mien - Deputy Director of the Vietnam Real Estate Market Evaluation Research Institute (VARS IRE) - said that in the first quarter of 2026, the entire market recorded about 52,000 commercial housing real estate products for sale. Of which, new supply reached about 38,000 products, slightly decreased compared to the previous quarter but still 2.5 times higher than the same period in 2025.

The supply structure continues to have a clear shift from a concentrated state to a multipolar trend, distributed more evenly between regions. Notably, the Central region accounts for 26% of the new housing supply, thanks to its advantages in land fund, infrastructure and urban development orientation.

Although supply is recovering, real estate prices are still maintained at a high level due to increased input cost pressure, especially land, financial and raw material costs. In the product structure, apartments continue to account for the leading proportion, up to 67% of the total newly opened supply.

Increased supply is gradually increasing the level of competition in the market, while creating more choices for buyers. The apartment segment structure has had a clear adjustment.

The luxury and super-luxury apartment segment only accounts for about 20% of new supply, down 20 percentage points compared to Q4/2025. Conversely, high-end apartments account for the largest proportion with 53%, up 29 percentage points compared to the previous quarter, mainly concentrated in satellite megacities.

The mid-range segment accounts for about 27% of the supply, with the main source of goods coming from provinces and cities in the suburbs of Ho Chi Minh City.

Notably, the commercial apartment segment priced at about 2-3 billion VND continues to be absent. In that context, social housing emerged as a bright spot when recording more than 7,000 products eligible for sale, contributing to filling the gap that commercial housing has not been able to meet.

Cautious buyer sentiment

According to Mr. Le Dinh Chung - General Director of SGO Homes, Vice Chairman of the Research Council - assessing the Vietnamese real estate market, in the primary market, selling prices continue to be maintained at a high level and tend to increase slightly due to increased input costs.

Conversely, on the secondary market, prices are starting to adjust locally. Liquidity is no longer simply dependent on whether the price is high or low, but increasingly dependent on the actual usable value and the ability to exploit the product's cash flow.

After the Lunar New Year holiday and in the context of high lending interest rates, buyers' psychology became more cautious in the first 3 months of the year.

Notably, the high-end apartment segment has seen "loss-cutting" transactions but not many due to financial pressure not reaching the threshold and long-term growth expectations still remaining.

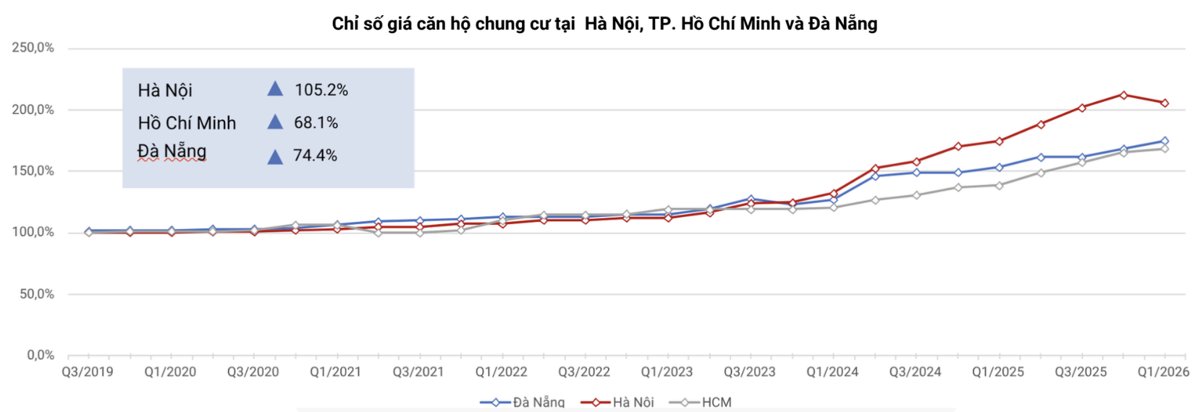

In Hanoi, secondary prices recorded a slight decrease in adjustment. While the offering price is still high, the actual transaction price tends to be more flexible and the transaction closing time is longer, reflecting that investors are adjusting price expectations in the context of not really strong liquidity.

Meanwhile, in Ho Chi Minh City and Da Nang, prices still maintain an upward trend, with increases of about 2% and 4% respectively quarterly, mainly thanks to positive expectations about planning, infrastructure and price increase room in the medium and long term.

Demand shifts to selective

Regarding liquidity, the whole market recorded about 24,000 transactions in the first quarter of 2026, equivalent to an absorption rate of 47% on primary supply. The absorption rate on new supply reached 58%, equivalent to more than 22,000 transactions.

Compared to the previous quarter, the absorption rate decreased slightly, partly due to coinciding with the Lunar New Year. However, the market still maintained positive results thanks to large real housing demand and flexible financial support policies from investors.

Under the impact of the general level of interest rates and cautious sentiment, the market did not fall into a "freeze" but switched to a selective disbursement phase.

Research by VARS IRE shows that buyer behavior has changed significantly. Buyers no longer chase after crowd psychology but prioritize products with transparent legal status, good exploitation capabilities and serving real housing needs.

Apartment buildings continue to be the segment leading in liquidity, accounting for 69% of total transaction volume. The absorption rate of new supply of this segment reached about 60%, equivalent to nearly 15,000 transactions.

Transactions are mainly concentrated before the Lunar New Year, with supply coming from projects with complete legal status implemented from 2025. In particular, projects with competitive prices recorded an absorption rate of nearly 100%.

Meanwhile, products lacking infrastructure and utilities - especially land plots in many areas - continue to fall into a state of sluggishness.