Households and individuals doing business under the contract tax method need to adjust revenue and the contract tax rate will be implemented according to Decision 3078/QD-BTC by the Ministry and Commune levels.

6 cases that need to be implemented

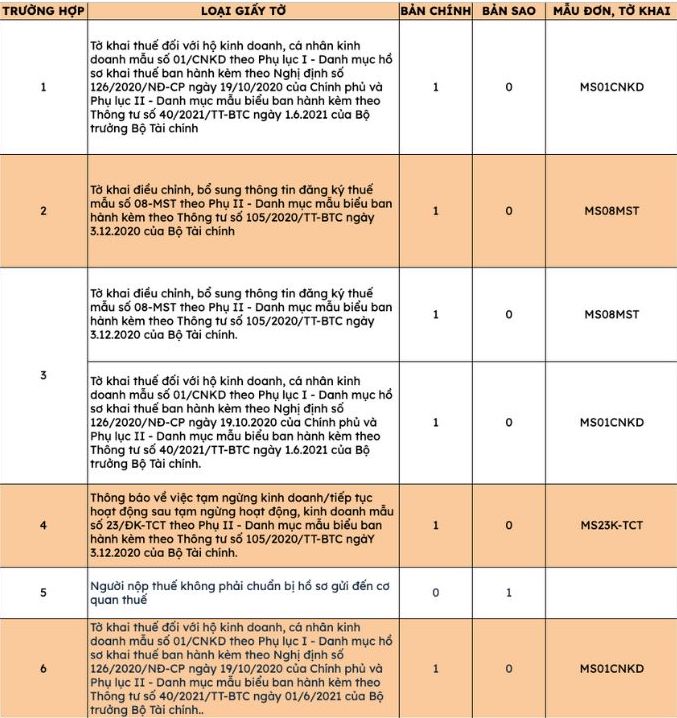

Case 1: The business contract changes the business scale (business area, employee capacity, revenue), then the Tax Declaration must be adjusted and supplemented according to form No. 01/CNKD.

Case 2: If the contracting household changes its business location, it is necessary to change the tax registration information according to regulations and carry out tax declaration procedures at the new location as for newly established business households.

Case 3: If the contract changes the business line and field (including the case of no change in the rate and rate of tax rate applied), the contract household must carry out the procedure for changing tax registration information according to regulations (if there is a change in the business line and field compared to tax registration), and at the same time declare an adjustment and supplement to the Tax Declaration according to form No. 01/CNKD.

Case 4: The contractor suspends or temporarily suspends business, the contractor shall make a notice when suspending or temporarily suspending business according to the provisions of Article 4 of Decree No. 126/2020/ND-CP dated October 19, 2020 of the Government.

Case 5: The contractor suspends or temporarily suspends business at the request of a competent state management agency.

Case 6: If the contractor switches to the declaration method, the contractor declares to adjust and supplement the Contract Tax Declaration according to form No. 01/CNKD.

Regarding the content of the dossier

Households and individuals determine cases where revenue and contract tax rates need to be adjusted to prepare the correct documents.

On how to do it

Households and individuals doing business can pay directly and no later than the 20th of the following month with changes in tax amount.

In addition, business households can conduct the tax payment online and no later than the 20th of the following month with a change in tax amount.

In addition, business households can use postal services. Notably, the payment date is no later than the 20th of the month following the month in which the tax payment changes occur.

For the 3 implementation forms, the tax authority issues a Notice of adjustment of revenue and contract tax rates of form No. 01/TB-CNKD or issues a Notice of not adjusting the contract tax rate of form No. 01/TBKDC-CNKD no later than the 20th of the month following the month with tax change.

In case taxpayers choose and send the application to the tax authority through electronic transactions, they must comply with the correct and complete regulations and conditions for conducting electronic transactions in the tax field in Circular No. 19/2021/TT-BTC dated March 18, 2021 of the Minister of Finance guiding electronic transactions in the tax field.