High US Treasury bond yields may put pressure on gold prices in the short term, but the reasons for rising yields make gold more attractive to both individual and institutional investors in the medium term.

Meanwhile, silver may face more obstacles as the Iran conflict overshadows economic growth prospects and weakens industrial demand, according to Ryan McIntyre - Senior Managing Partner at Sprott Inc.

In an interview with Kitco News earlier this week, Mr. McIntyre emphasized that the next wave of large investment demand for gold from institutions has not really taken place yet.

According to him, this trend started from central banks a few years ago, then spread to individual investors and partly institutions through ETFs in mid-2024. Signs of interest rate cuts appearing at Jackson Hole late last summer contributed to maintaining this momentum until a conflict with Iran occurred.

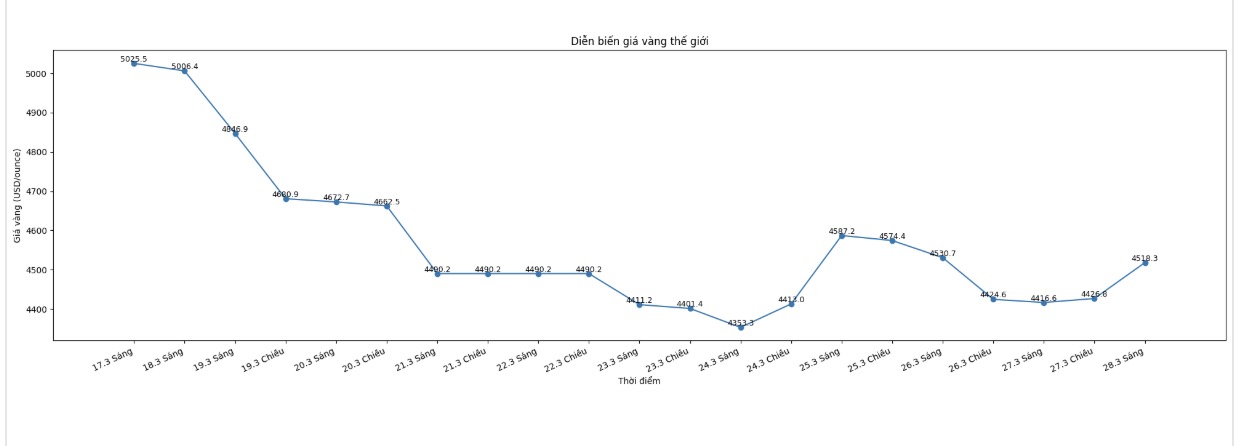

Although gold prices have fallen sharply since the end of January, especially in the early weeks of the Iranian conflict, he believes that long-term factors supporting this precious metal have not changed since 2022.

According to him, the most notable factor is the opportunity cost when compared to bond yields. Rising yields have led some investors to switch to holding the USD - an asset with higher liquidity. However, that does not change the role of gold in the investment portfolio.

He cited that if investors hold 10-year term bonds from January to now, an additional yield increase of about 30 - 40 basis points has caused the bond value to decrease by about 3 - 4%, a significant decrease for an asset that is considered stable.

At the same time, long-term financial prospects are worsening as the government may have to continue printing more money, which will be beneficial for gold but disadvantageous for bonds.

A question is why organizations have not yet strongly participated in the gold market even though prices have increased significantly in recent years. According to McIntyre, the main reason is the lack of internal expertise in commodities and gold after many organizations withdrew from this field after a period of strong adjustment before 2015.

In addition, the stock market has grown well for a long time, making them unmotivated to look for alternative investment channels. He believes that organizations will only really act when the stock market no longer maintains positive performance.

He also said that the Bitcoin boom may have attracted part of the investment resources of institutions, which may be for gold. He recounted the case of a large family fund in Europe that invested hundreds of millions of USD in Bitcoin but completely did not hold gold or commodities, showing the difference in asset approach.

Regarding silver, he said the prospects are even more complex due to much dependence on industrial demand. Although the silver market is forecast to continue to be short of supply this year - for the sixth consecutive year, economic concerns may reduce consumer demand and put pressure on prices in the short term.

At the same time, the increase in yields is also an unfavorable factor, although silver still plays a certain role as a diversified and monetary asset.

According to Mr. McIntyre, in the short term, negative factors are dominating silver. He believes that this metal is unlikely to attract investment flows again if gold has not entered a clear upward trend. Conclusion, gold will be the leading asset, while silver is likely to increase afterwards.