According to Mr. Tai Hui - Chief Market Strategist for the Asia-Pacific region of JP Morgan Asset Management, the strong sell-off of gold during the Iranian conflict has weakened the role of this precious metal as a defensive asset in the investment portfolio. Instead, investors should see gold as an investment asset, not a risk hedging tool.

Mr. Hui said: "Gold has not played a risk hedging role in the face of geopolitical fluctuations. We have argued for quite a long time that gold is not a truly effective risk hedging tool for any factor. Looking at the level of correlation between gold and stocks or risky assets, this relationship is not stable.

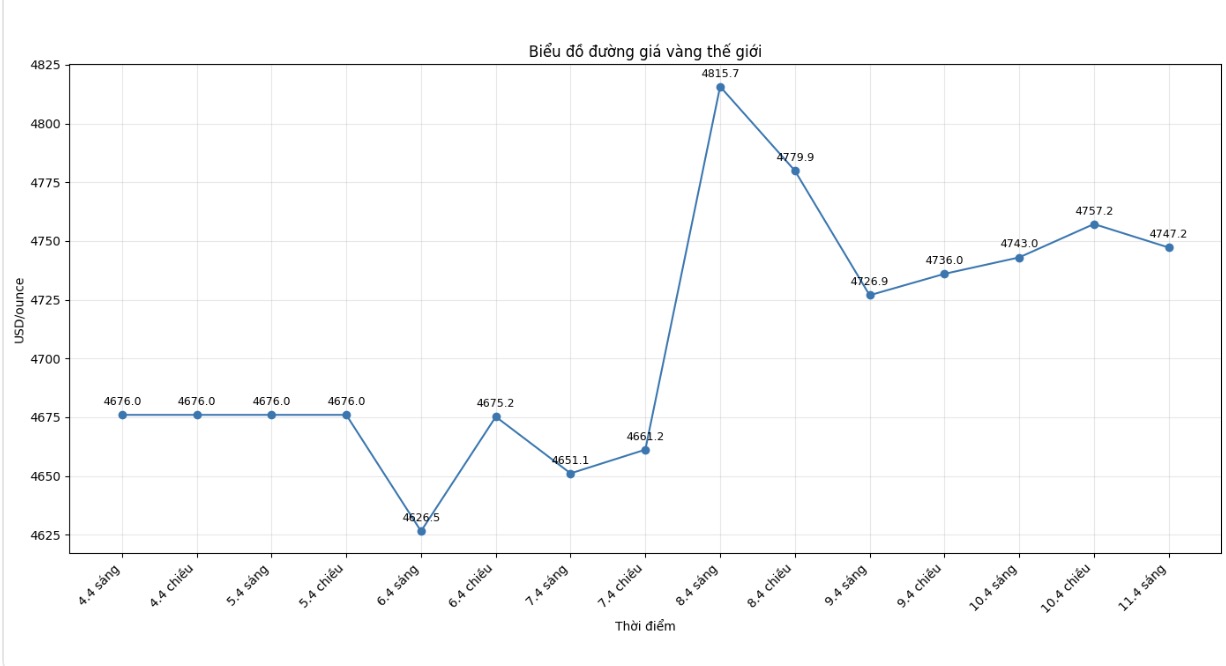

Although prices have somewhat recovered compared to the lowest level, gold prices still have difficulty regaining momentum as the conflict drags on.

Mr. Hui believes that many investors still see gold as a hedging tool against geopolitical events, although in fact the effectiveness of gold in such situations in the past 30 years has been quite weak.

We can't even say that 70% of geopolitical events help gold appreciate. The ratio is only 50/50, like throwing a coin," he said.

Not only affected by geopolitical shocks such as the Iran war, gold also faces many other disadvantages. According to Mr. Hui, gold volatility is equivalent to stocks in emerging markets. Besides, gold does not generate income flows.

However, JP Morgan representatives also emphasized that gold still has reason to be held in the investment portfolio. Long-term demand from central banks wanting to diversify reserves, reduce dependence on the USD, along with the risk hedging trend in the face of rapid increases in public debt and money supply, are still factors supporting gold.

“Because gold supply growth is limited, there is still an investment basis for gold. But we need to be very clear that gold is an investment asset, not a risk hedging asset,” Mr. Hui said.

Accordingly, gold is still a noteworthy asset in portfolio allocation, but its main role should be understood as increasing yields, rather than a risk management tool.

Meanwhile, JP Morgan still maintains a positive view of gold's upward trend in the long term and believes that price adjustments are only temporary. Previously, on February 17, experts at this bank said that there were still arguments refuting the continued upward momentum of gold, but those arguments were not convincing.

According to Ms. Kriti Gupta - CEO of J.P. Morgan Private Bank, and Mr. Justin Biemann, Global Investment Strategist, gold prices have increased by more than 170% in the past 5 years. One of the biggest drivers is the new phase of geopolitical instability and fragmentation, prompting investors to turn to this precious metal.

The two experts also said that concerns about currency devaluation, economic growth, inflation and lack of fiscal discipline continue to make gold an attractive asset in times of tension.

However, JP Morgan points out two major risks to gold price rise prospects. The first is the possibility of central banks ending the gold buying wave in recent years. According to experts, central bank net buying has doubled since the Russia-Ukraine conflict broke out in 2022, when many countries wanted to diversify reserves away from the USD after the US freezed Russian assets.

Second is the risk of individual investors turning their backs on gold. However, JP Morgan believes that individual investors still have reasons to continue holding or increasing gold, not only to cope with short-term geopolitical risks but also to diversify in the long term, prevent inflation, improve efficiency in periods of sharp market decline and reduce overall portfolio volatility thanks to a relatively low correlation with other assets.

JP Morgan believes that the weakening USD, falling US interest rates, along with economic and geopolitical instability, which are traditional factors supporting gold prices, and all are contributing to the current increase. The bank forecasts strong demand from investors, along with continued demand from central banks, will help gold buying power remain at an average of 585 tons per quarter in 2026.