In the latest report on precious metals, Mr. Mike McGlone - senior market strategist at Bloomberg Intelligence (BI), said that although he does not rule out the possibility that gold prices may increase to 6,000 USD/ounce, the scenario with a higher probability is that the price will return to testing the support zone around 4,000 USD/ounce.

This expert believes that the downward space for gold is still large, as record highs set last week may be a signal that the market is pegging. According to him, silver prices may also fall sharply, falling back to the 50 USD/ounce mark.

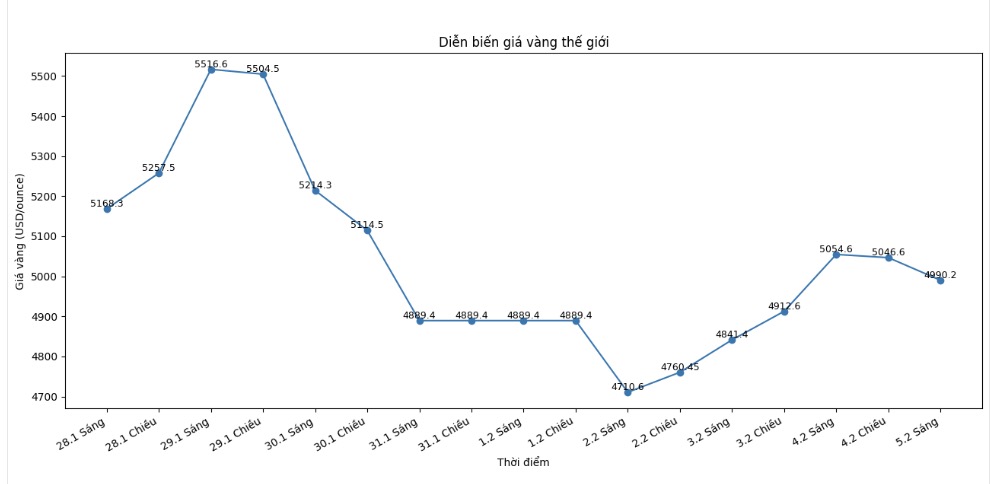

The "standstill" increase in gold and silver in January shows many signs that 2026 may be a year of correction, in the process of creating market peaks" - Mr. McGlone said. "The upward momentum may also push gold up to 6,000 USD/ounce, but according to the usual returning law, prices tend to return to the 4,000 USD/ounce zone.

According to Mr. McGlone, not only falling into a state of overbought, gold's upward momentum also far exceeded the general commodity index. He cited that at its peak, the ratio between the Bloomberg Commodity Index (BCOM) and gold prices once reached 68 points, compared to the baseline of 100 in 1960. Meanwhile, the level of 50 once marked important bottoms in 1980, 1987 and 2020. Currently, this ratio is only about 32.

“To keep gold maintaining such a large difference compared to the basic commodity group, a "model" change - or maybe BCOM is being overvalued? ” - he raised the issue. “When prices rise too fast and too strongly, the underlying factors can change very quickly. We believe that the risk of gold'overvaluation' is currently at an extreme level, making the risk/profit ratio less attractive.”

In addition, Mr. McGlone also believes that gold is being overvalued compared to inflation. He emphasized that since US President Richard Nixon ended the gold binary regime in 1971, there has never been a time when gold has increased sharply in the context of low inflation as it is now.

Will inflation follow the vertical upward momentum of this precious metal, or will the post-inflation deflation scenario return to normal in history? We lean towards the second scenario," he said.

However, the Bloomberg Intelligence strategist believes that gold still plays a certain role in the investment portfolio, especially as a diversification asset. He noted that even in high prices, the ratio between gold and the S&P 500 index is still at a noteworthy level.

When gold prices peaked about 15 years ago, the ratio of gold ounces to the S&P 500 index also peaked nearly 1.7 times. By February 3, this ratio was only 0.71 times, which is less than half of the 2011 level. This may play a supporting role, helping gold maintain its position as a defensive tool in the context of the stock market being in a high valuation zone" - he analyzed.

Regarding the outlook, Mr. McGlone believes that if the stock market continues to rise sharply, gold prices may face further downward pressure. However, in the event of a stock market correction, gold - even if at a lower price - may still outperform relatively.

For silver, Mr. McGlone said that the gold/silver ratio is unlikely to remain below the 50 threshold. The sharp drop in silver prices in the last and early sessions of this week has brought this ratio back to the historical average, currently around 56.6.

This year's peak of 121.65 USD may be retested, but the price returning to the 50 USD/ounce zone is a normal scenario for high volatility metals" - Mr. McGlone concluded.