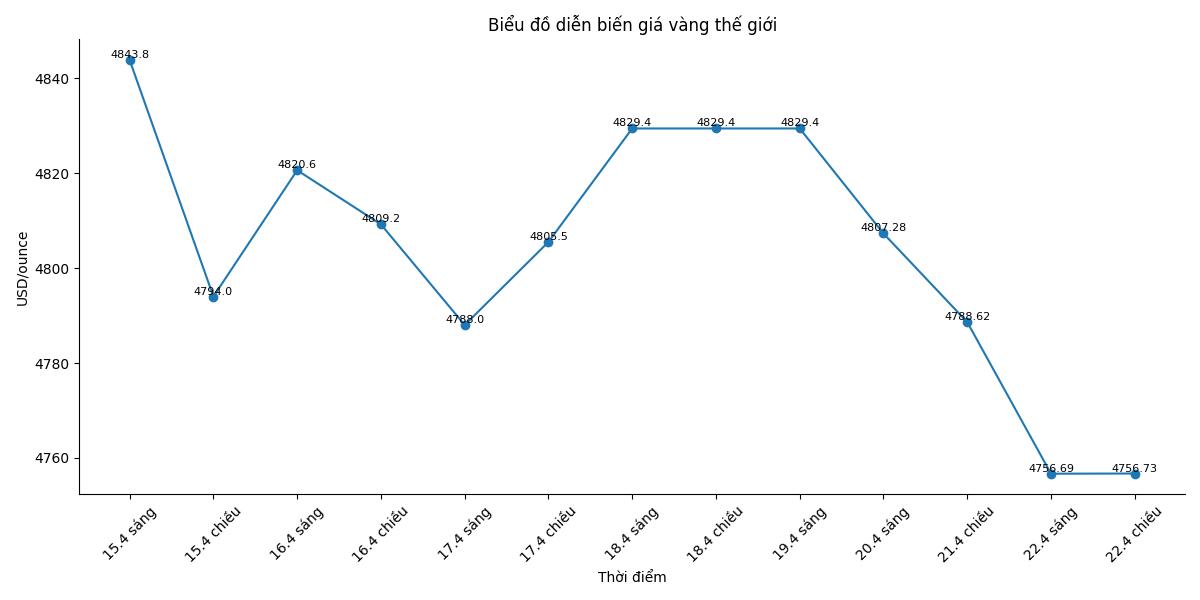

Gold prices recorded the deepest drop in more than two weeks when losing more than 100 USD in just one session, from an opening price of 4,842 USD/ounce to nearly 4,700 USD/ounce, before fluctuating around the range of 4,720–4,760 USD/ounce. The decline took place in the context of a sharp increase in the USD, rising US bond yields and concerns about continued inflation due to conflicts in the Middle East.

This development reflects an increasingly clear paradox in the market: geopolitical tensions – a factor that once fueled cash flow to gold – are triggering currency tightening risks, thereby reducing the attractiveness of precious metals.

The continued blockade of the Strait of Hormuz has caused a major energy supply shock, pushing oil prices to stay above the threshold of 90 USD/barrel. This increases global inflationary pressure, forcing central banks to consider maintaining high interest rates or even continuing to raise interest rates.

In that context, the rising USD becomes a factor that puts direct pressure on gold – an asset valued in greenbacks and not yields. As interest rates rise, the opportunity cost of holding gold also increases, causing cash flow to tend to shift to profitable assets.

Notably, the statement of Mr. Kevin Warsh – Chairman of the US Federal Reserve candidate further strengthens the expectation of prudent monetary policy. He believes that a new framework is needed to deal with persistent inflation and does not commit to sharp interest rate cuts in the near future, reducing market monetary easing expectations.

In the opposite direction, diplomatic signals caused gold prices to fluctuate sharply in each session. US President Donald Trump's extension of the ceasefire with Iran helped gold prices recover slightly, as concerns about an inflation shock eased.

However, the prospect of negotiations is still very fragile. Conflicting signals from both sides make the market maintain a state of high caution. Analysts believe that gold prices are currently "largely dependent on news related to the ceasefire and liquidity demand", while any breakdown in negotiations could quickly reverse the trend.

Since the conflict broke out at the end of February, gold prices have fallen by about 8–11%, mainly due to liquidity pressure in the early stages that forced investors to sell to compensate for losses in other assets.

However, considering the long-term picture, gold prices still maintained a significant increase, increasing by more than 25% from the beginning of 2025 and about 43% compared to the same period last year. This shows that the upward trend is still supported by fundamental factors such as prolonged inflation, economic instability and the need for central banks to stockpile.

Major organizations such as JPMorgan and Goldman Sachs continue to maintain a positive outlook, forecasting gold prices may fluctuate in the range of 4,000–6,300 USD/ounce until 2026. Central bank demand for gold, although slowing down, still plays an important "price base" role, limiting the risk of prolonged deep declines.

In the short term, the gold market is facing many major variables: US economic data, inflation outlook, US Federal Reserve policy and especially the results of negotiations between the US and Iran.

Whether the recent decline is an opportunity to buy or a starting signal for a deeper correction cycle will depend on geopolitical developments in the coming days. If the conflict escalates, gold may regain its shelter role; conversely, if risk cools down and interest rates remain high, downward pressure will continue.