Increased supply, positive liquidity

According to a summary from the One Mount Group Market Research and Customer Understanding Center, in the first quarter of 2026, the primary apartment market recorded simultaneous improvement in both supply and liquidity, showing that absorption capacity is still maintained positively despite the high interest rate level.

In Hanoi, the newly opened supply reached about 8,800 units, double compared to the same period in 2025. The recorded transaction volume was about 7,300 units, equivalent to an increase of 122% compared to the previous year, reflecting a high absorption rate and stable real housing demand. Similarly, in Ho Chi Minh City, the supply reached about 3,700 units, an increase of 86%, while the consumption volume reached about 4,800 units, an increase of about 70% compared to the same period.

In Ho Chi Minh City, the Binh Duong area continues to be the main driving force when supplying nearly 2,200 units, equivalent to about 60% of new open supply. Although the central area recorded an increase in supply, it is still local and dependent on the limited number of projects.

This development shows a structural shift in the market, in which satellite areas are increasingly playing a "regulating valve" role in supply and price levels, while effectively meeting real housing needs in the context of increasingly narrowing affordability in the central area.

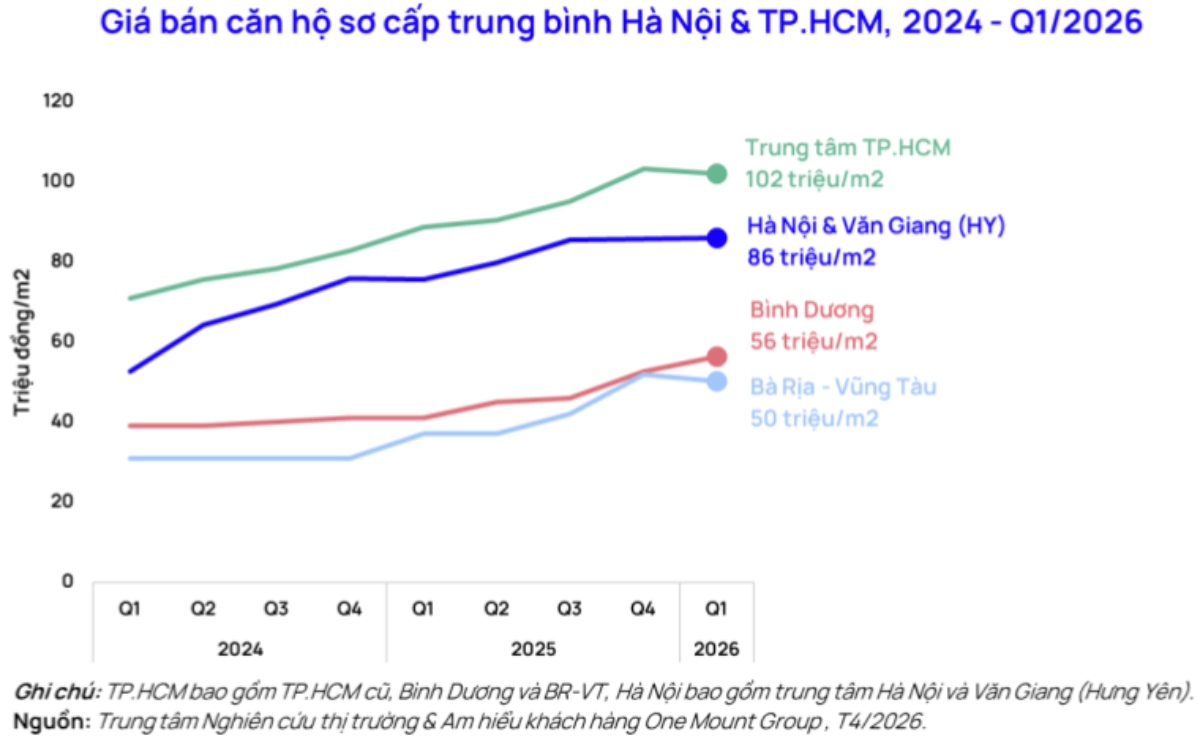

Stable price level, differentiated by region

In the first quarter of the year, primary selling prices in the two major markets generally remained stable compared to the end of 2025.

The average price in the center of Ho Chi Minh City is about 102 million VND/m2, while Hanoi is about 86 million VND/m2. However, inside the overall picture is a clear differentiation between regions.

In Hanoi, the price level in the inner city area continues to linger at a high level, averaging about 124 million VND/m2, an increase of 14% quarter-on-quarter. The main reason comes from new supply in the high-end segment with prices above 150 million VND/m2.

In Ho Chi Minh City, Binh Duong emerged with an average price of about 56 million VND/m2, up 7% quarter-on-quarter and 37% compared to the same period. Some new projects have set a price level of over 70 million VND/m2, reflecting growth expectations after mergers and infrastructure improvement.

Despite recording positive signals in the first quarter, the One Mount Group Market Research and Customer Understanding Center forecasts that supply in 2026 will have a downward adjustment compared to previous forecasts.

The main reason comes from high interest rates that increase capital costs, and at the same time, investors become more cautious in implementing new projects. It is forecast that the total newly opened supply in Ho Chi Minh City in 2026 will reach about 28,000 - 29,000 units, a decrease of about 2,000 units compared to previous expectations. However, Hanoi is still considered a bright spot with an expected supply of 35,000 - 40,000 units.

Commenting on the market, Mr. Tran Minh Tien - Director of One Mount Group Market Research & Customer Understanding Center said: "The market is being significantly affected by interest rate fluctuations, but still maintains stability in supply and liquidity. This is a positive sign in the current context. However, to fully assess the impact of macroeconomic factors, more monitoring time is needed.

Mr. Tien also recommended that buyers and investors should prioritize projects from reputable investors, and balance their finances appropriately to limit risks in the context of fluctuating interest rates.