Ole Hansen - Head of Commodity Strategy at Saxo Bank - said that in the past two weeks, "market sentiment has shifted from excitement to caution, as investors reassess the level to which the 2025 stories - interest rate cuts, fiscal pressures, geopolitical risks and central banks' demand for gold - have been reflected in prices".

He noted that the festive season in India often boosts demand for gold jewelry. The market has now entered a stagnant period after the holiday something that is common every year and will likely stabilize again when year-end demand appears, supported by the recent price adjustment Hansen commented.

He also highlighted a notable development in China: the government has ended a long-standing VAT exemption policy for jewelry retailers who buy gold through the Shanghai Gold Exchange and the Shanghai Commodity Exchange.

According to Hansen, this change will cause retail prices to increase slightly and may reduce jewelry sales, but the macro-economic impact is limited. Investment gold in the form of bars, coins and ETFs is still completely exempt from taxes, ensuring that major channels that drive Chinas record physical demand are not affected, he wrote.

Hansen also mentioned that a recent speech by Federal Reserve Chairman Jerome Powell said that the December rate cut not a certain thing had strengthened the US dollar and real yields increased, cooled down the excitement of the gold market. Meanwhile, the market's reaction to the progress in US-China tariff negotiations is still quite reserved.

Investors understand that deeper strategic tensions are still unresolved, especially in the technology, supply chain and industrial policies sectors. This announcement could help reduce extreme risks, but not change the long-term rational reasons for holding defensive assets such as gold," he said.

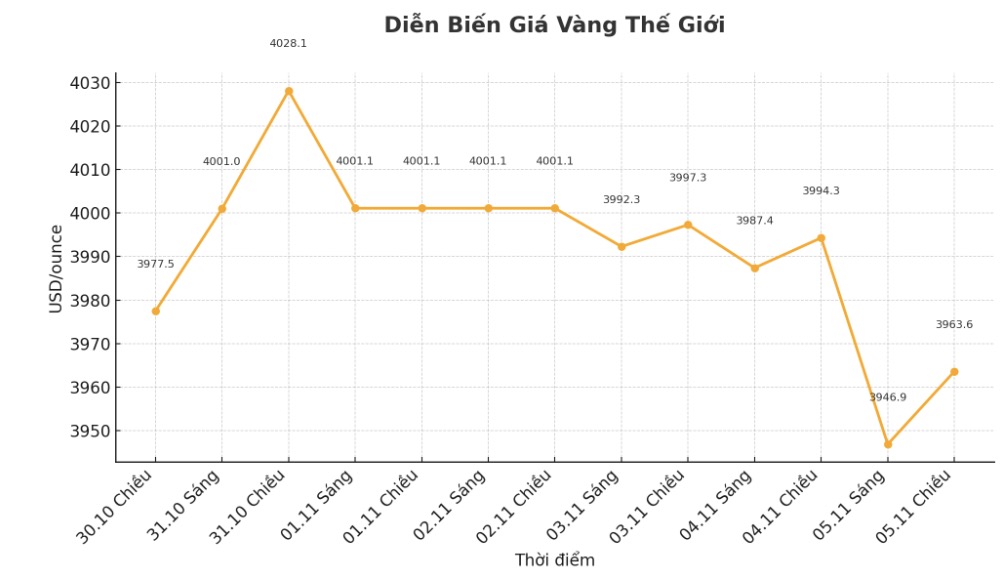

Technically, Hansen believes the recent price correction is a healthy development, showing that the market is relieving pressure rather than reversing trends.

The support zone is forming around $3,8353,878 a month, which corresponds to a 50% Fibonacci retracement in the rally since August and also overlaps with a 50-day moving average, he said, warning that a deeper decline could still happen if the risk appetite in the stock market remains strong and the US dollar continues to rise.

He also noted that ETF holdings rose sharply in the recent rally, and futures data chi showed a moderate decline in buying position, not a sell-off.

Meanwhile, central banks continue to be the main source of support, with the World Gold Council reporting official purchases in the third quarter reached 220 tons, bringing the total since the beginning of the year to 634 tons nearly the same as last years record. This stable official demand helps limit downward volatility," he said.

Despite gold's weakening in the short term, Hansen said factors such as high public debt, currency depreciation risks, central bank reserve demand and the Fed's policies still strengthen the prospect of price increases in the medium term.

Regarding the short-term outlook, he said that although the peak this year may have formed, the current decline looks more like a consolidation phase than a decline.

The previous major adjustment, after a May peak of nearly $3,500/oz, lasted about four months before prices broke out in August, up 27% in nine weeks. If history repeats itself, gold may continue to move sideways for a few more months before regaining momentum in early 2026. During this time, high fluctuations and constantly changing psychology will test the confidence of both buyers and sellers" - Hansen reiterated.

When this adjustment period ends, the drivers that have fueled this years rally public debt, inflation and asset diversification are likely to return, turning the next rally into a story for 2026.