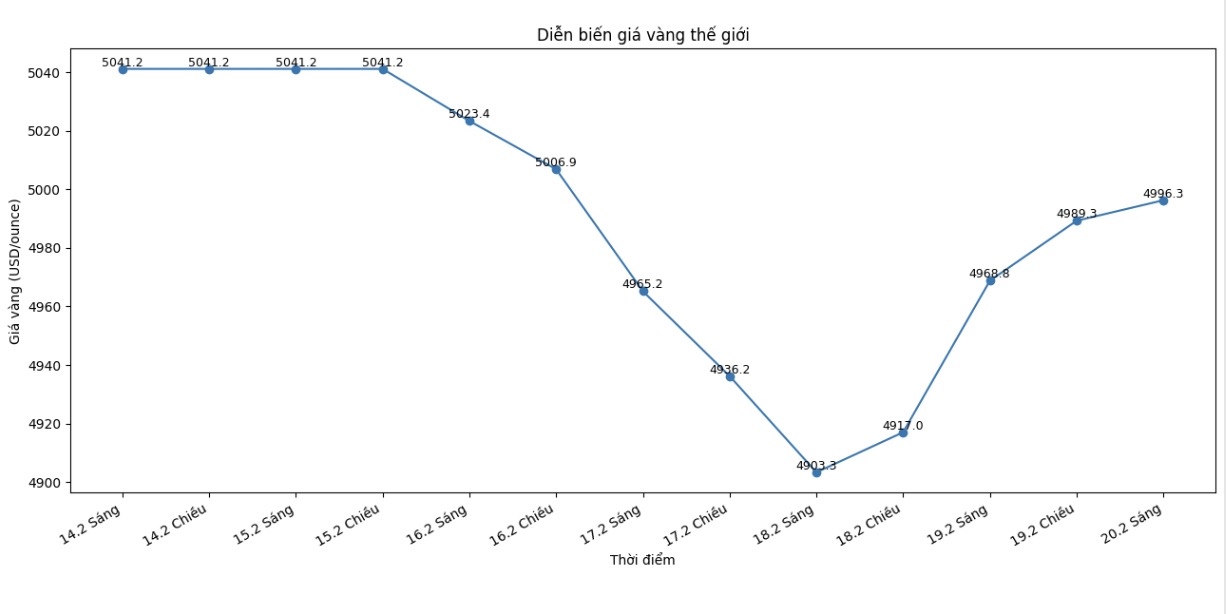

The strong correction of gold last month, after US President Donald Trump nominated Kevin Warsh as the next Fed Chairman, mainly reflects technical factors and market position rather than fundamental changes, said Kevin Flanagan - Head of Investment Strategy at WisdomTree in a recent interview.

After a period of "standstill" increase, bringing gold prices to a record level of nearly 5,600 USD/ounce at the end of January, this precious metal became vulnerable to profit-taking activities.

According to Mr. Flanagan, information about Warsh only serves as an excuse, not the real reason for the correction. "After a parabolic increase, profit-taking, accumulation or correction are all healthy developments for the market," he said.

Initially, the market saw Mr. Warsh's nomination as a factor to help stabilize the direction of monetary policy. Mr. Flanagan said that Warsh is considered an experienced policy maker, understanding the value of the Fed's independence.

He meets many positive criteria and fully understands the principle of independence of the Fed" - Flanagan commented.

Kevin Warsh used to work in the Fed's periods of operating under traditional monetary policy, and also went through the 2008 financial crisis - which brought a familiar feeling to investors in the context of increasing political pressure. However, although this nomination may ease concerns about the possibility of direct political intervention in the Fed, Flanagan warned that it does not mean that instability disappears, nor does it reduce the strategic role of gold.

He believes that real challenges could arise right at the first meeting chaired by Warsh. "If the labor market continues to be strong and inflation remains higher than target, it is very likely that Warsh will not cut interest rates" - Flanagan said.

If this scenario occurs, tensions between the White House and the Fed may quickly return. Warsh may bring institutional credibility, but cannot completely eliminate political conflict. And according to Flanagan, such prolonged clashes are often beneficial for gold.

On the contrary, he rejected the view that the Fed's independence is being threatened. Flanagan said that concerns that the Fed is dominated by politics are exaggerated, because the organizational structure of this agency inherently has protection mechanisms.

The Federal Open Market Committee (FOMC) consisting of 12 members with voting rights, including rotating regional Fed chairmen, plays a "barrier" role in preventing unilateral influence.

The Fed's own structure helps protect the independence of this agency," he emphasized.

Even when new governors are appointed, the Senate approval process and the balance between regional governors and Fed presidents also limit the possibility of policy changes in an extreme direction. This brings peace of mind to US investors.

If the Fed implements one or two more cuts, those are just minor adjustments, not a return to hyper-loose policy. A sharp cut in interest rates will require a recession scenario – which is not within WisdomTree's baseline forecast.

According to Flanagan, as the story of interest rate cuts is no longer the central factor, gold will increasingly be shaped by broader and more sustainable drivers.

In addition to monetary policy, the main factors supporting gold remain, including geopolitical tensions, trade conflicts, uncertainty about tariffs and the gold buying trend of central banks.

Geopolitics, trade wars, tariffs, central bank purchases - all are still present. They don't disappear at all," he said.

The most important message in Flanagan's assessment is that gold no longer simply responds to individual news headlines. This precious metal is reflecting a multi-layered and prolonged unstable environment.

According to him, factors such as trade disputes, fiscal expansion, increased global public debt and tensions between the government and the Fed are not temporary phenomena but structural.

These instability will continue for the next few years," Flanagan said, adding that gold is increasingly seen as a neutral asset in the context of policy turmoil.

Gold is no longer considered a tactical allocation, but is increasingly a strategic choice in the investment portfolio," he concluded.

For Flanagan, the recent adjustment did not mark the end of gold's upward momentum, but was just a necessary break in the context that regulatory risks are becoming a driving force.